One of the most popular questions I’m getting from clients right now is how to position portfolios in the face of rising rates.

It’s not surprising given that long-term rates have spiked since the Fed’s now-famous tapering comments – 10-year Treasury rates have jumped almost 1.0% from a low of roughly 1.6% in early May to roughly 2.6% this week. Investors — suddenly faced with the potential of negative fixed income returns after a long bull bond market — are showing a renewed interest in equities as a potential rising rate hedge. But investors should look before they leap, since it’s not necessarily the case that equity and bond excess returns[1] can be expected to reliably move in opposite directions.

The statement above may be surprising to investors who have followed US markets in the past few years because recent data on the relationship between equity and bond excess returns seems to support the idea of equities acting as a hedge for bonds. Indeed, since the bottom of the crisis (i.e. the period March 2009 to April 2012) the correlation[2] between equity and bond excess returns was a negative 50% (which means equity and bond excess returns were moving in opposite directions, while there was a positive correlation between bond rate changes and equity returns). So, what gives?

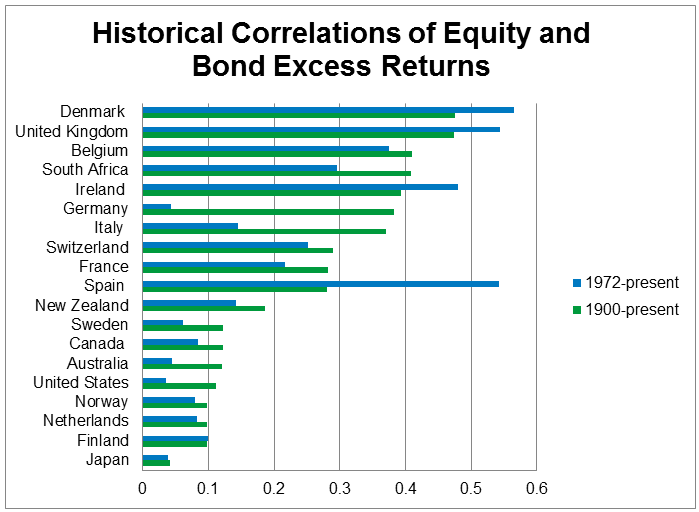

The answer is that this most recent period data isn’t the norm either historically for the United States or across other developed markets. To see this, I look at data collected by Dimson, Marsh and Staunton (generally referred to as the “DMS data”)[3], which contains annual returns for key assets across 20 countries from 1900-present. The breadth of this data provides a very broad view of what the “normal” behavior of returns looks like over the long run in large (mostly developed) markets.

Using this data the correlation of equity and bond excess returns across the entire sample is a positive 25%. If we look at a more recent period (since the breakup of the gold standard[4]), the correlation is still a positive 23%. And perhaps more importantly, there is no single country (see the chart below) where the correlation for equity and bond excess returns is negative either for the full period since 1900 or since the 1970s. In short, equities and bonds can diversify each other in the short term, but over the long run their excess returns do not reliably move in opposite directions.

{kind=link}