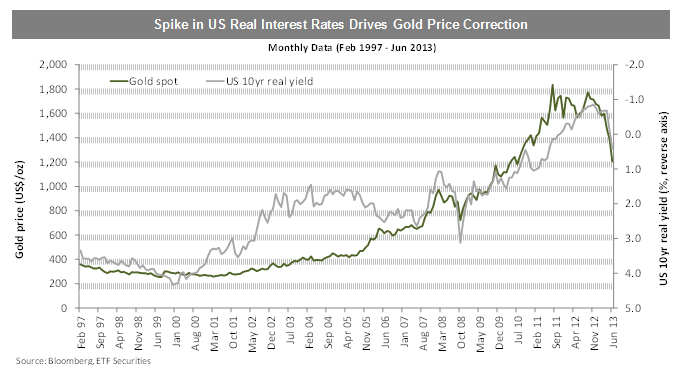

Precious metals, particularly gold and silver, were hit hard last week as investors continued to re-assess the outlook for US monetary policy. The sharp rise in US real interest rates has been the main trigger for the correction in gold and silver prices.

In our view the reaction of bond markets to Fed comments has been overdone, and ultimately real interest rates will fall back from current levels. It appears that the Fed agrees that bond markets have over-reacted and key FOMC members appear to be trying to talk rates back down now. With gold speculative shorts at all-time highs and market sentiment almost unanimously negative, we believe there is scope for a price reversal in the coming weeks and months. Silver should benefit from a gold price rebound.

Platinum and palladium have been affected more by the recent liquidity squeeze and resultant growth fears in China. Again, we believe the sell-off is overdone. We expect China liquidity conditions will ease and growth fears will dissipate over the course of the year, removing this hindrance to platinum and palladium price performance. An added source of longer-term price support for all four of the precious metals is that they are all now trading well below estimated marginal costs of production.

Gold price falls below US$1,200oz for the first time since August 2010. Positive data from the US weighed on the gold price last week, accelerating its slide below US$1,300oz from the week before. With key resistance levels at US$1,150-1,155oz, gold risks to retrace even further to US$1,030oz. On the physical demand side, the increase in import duties in India, coupled with a weak Rupee, have weighed on Indian demand. However, China demand appears to be robust with a number refiners having trouble keeping up with China demand. With the gold price trading below estimated average marginal production costs, gold miners are starting to slash costs with negative implications for future supply.

South Africa mining unions ask for a 15% to 60% pay rise. With wage contracts coming to an end on June 30 and unions asking for double-digit increases in wages, negotiations between executives and workers’ representatives risk becoming extremely heated. Despite the recent price correction, palladium’s fundamentals remain the strongest across the precious metals sector in our view. South African production, which accounts for 35% of global palladium production, continues to become more costly. Meanwhile both US and China demand remains strong.

Key events to watch this week. US non-farm payrolls on Friday will likely be the main market focus as investors look to see whether employment is moving to levels the Fed will be comfortable removing QE. The US ISM will also be looked at for similar reasons. Watch also for more potential guidance from Fed members trying to talk bond markets down. In Europe, PMIs will be watched for indications that the ECB may have to become more aggressive in easing. In the UK, Mr Carney (formerly of the Bank of Canada) will be taking over Governor King’s seat at Bank of England and investors will be watching closely for any hints of change.

{kind=link}