The Japanese markets have been largely a one-way path higher in the last six months, as market participants focus on the bold actions of the Bank of Japan (BOJ) targeting 2% inflation through unprecedented monetary stimulus. One outcome of these bold policies has been a substantially weakening yen, which provides support to Japan’s exporters.

The steep sell-off was triggered by a worse than expected Chinese economic report. Will this be a psychology changing report that changes the tone of the market? I doubt it.

Just recently the yen breached a critical 100 yen per U.S. dollar level that was a key psychological barrier for continued yen weakness. When one focuses on the fundamentals of Japanese companies, the earnings outlook has improved meaningfully as a result of this currency weakness (discussed below).

With the equity market rising in conjunction with earnings expectations, I believe the case for Japan’s equity markets is intact. A key variable to watch, of course, is the exchange rate, as much of the moves higher in equities are tied to weakness in the yen. From a historical perspective, I believe there is more room for weakness.

Longer-Term Perspective

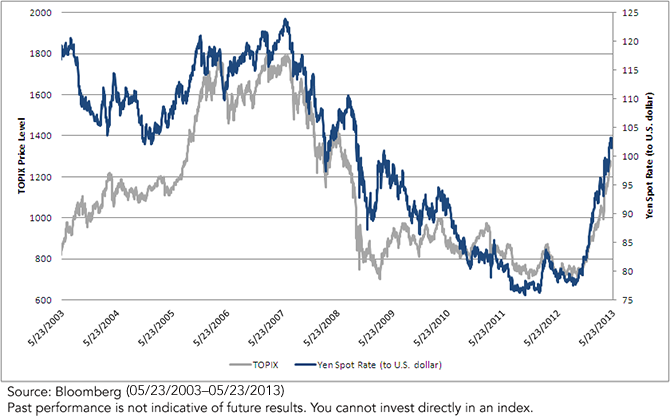

Although the yen has weakened recently, both the yen and the TOPIX (Tokyo Stock Price Index) are still below their pre-financial crisis levels of mid-2007. The BOJ recently argued that the yen hadn’t weakened against other currencies but rather begun to moderate from its excessive highs toward a more balanced level. Let’s look at the 10-year history of both the TOPIX and the yen–to-dollar exchange rate in the chart below.

{kind=link}

• Recently Strong Trend –The yen has weakened by more than 14.0% against the U.S. dollar, and the TOPIX has returned over 38% year-to-date. The yen has weakened over 25% since its 2011 highs against the dollar, and the TOPIX has gained over 70% since its 2012 lows.

• Still Below Recent Highs – Although the yen has weakened substantially against the U.S. dollar and the TOPIX has surged, both are below their pre-crisis levels. The yen would need to depreciate another 22%, and the TOPIX would have to appreciate over 52% for them to return to the highs set in 2007. To put this in perspective, the S&P 500 Index is currently around 4% above its 2007 high.

• Current Levels – Many experts expect the yen to weaken further against the dollar as a result of the Bank of Japan’s monetary actions and 2% inflation target. Considering the price action over the past 10 years, I also think there is more room for the yen to weaken if the Bank of Japan continues to stimulate the economy through monetary policy.