Even with Rate Cuts, Carry Still Attractive

Although the central bank has recently cut interest rates by 0.25% to 7.25%,5 we still believe India provides attractive opportunities for carry. In fact, India still has some of the highest short-term interest rates across all emerging markets. As of March 31, 2013, the “implied yield” of 3-month forward contracts was 7.68%.6 The notion of implied yield means that, should the value of the rupee not change against the U.S. dollar, the return embedded in the forward currency contract would be 7.68% on an annualized basis. For currency investors, this interest rate provides a “cushion” of returns that could potentially mitigate or offset losses, should the rupee depreciate against the U.S. dollar.

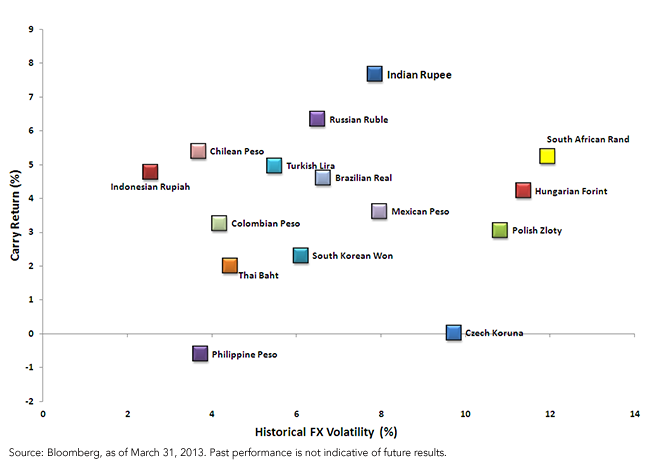

Additionally, many currency investors look to a concept known as carry per unit of foreign exchange (fx) volatility. Essentially, this measure attempts to provide a standardized means of comparing risk and reward in currency markets.

{kind=link}

As the chart above shows, the Indian rupee has provided some of the highest implied interest rates of any emerging market country over the past year. However, it has also seen its volatility climb compared to other Asian and Latin American currencies over the past year. Yet when compared to many European or African currencies, the rupee has been comparatively attractive given its higher carry and lower levels of volatility.

Outlook for the Remainder of 2013

If rate cuts and inflows are supplemented by further political reforms, we believe the Indian rupee has the ability to deliver sizable appreciation against the U.S. dollar by the end of the year. Combined with higher local interest rates, investments in the Indian rupee could potentially provide an attractive entry point for investors near current levels.

Rick Harper is head of fixed income and currency for WisdomTree Asset Management. This post was republished with permission from the WisdomTree blog.

1Source: International Monetary Fund (IMF), 2013.

2Source: Bloomberg, 4/30/2013.

3IMF, 2013.

4IMF, 3/31/2013.

5Source: Bloomberg, May 3, 2013

6Source: Bloomberg, 2013