I would argue that analysts are drawing a misguided conclusion about dividend stock valuations by just looking at these particular higher-dividend sectors. When one looks at diversified baskets of dividend stocks across all market sectors, shown through the WisdomTree Indexes above, the valuation picture changes.

It is also important to remember that not all dividend strategies offer exposure to the same types of dividend-paying stocks. Some dividend indexes are designed to represent a broad basket of dividend payers, while others select stocks based on high dividend yields or dividend stocks with growth characteristics. Below, we review WisdomTree Indexes for each category along with their current valuation picture.

Similar P/E Ratios: Whether one looks at high-yielding dividend payers, large-cap dividend payers or potential dividend growers, we find the P/E ratios to be in a very narrow band and all below 15 times earnings. We find these to be very reasonable valuations, especially given where U.S. equities are by the same metric.

Primary Difference Is Dividend Payout Ratio: Because the price-to-earnings ratios and, conversely, the earnings yields (earnings-to-price ratios) are broadly similar for these indexes above dividend strategies, one of the key elements leading to the differences in dividend yields would be the payout ratio. The potential dividend growers had the lowest dividend payout ratio (dividend yield / earnings yield)—33%—and thus a lower dividend yield than the high-yielding dividend payers, which had a dividend payout ratio of 56.6%. But that is not to say that one set of stocks is dramatically more expensive than the other—the P/E ratios are similar. The story being told by the numbers is that the high-yielding dividend payers are returning more of their earnings to shareholders, whereas the potential dividend growers—similarly priced on a P/E ratio basis—are reinvesting a greater share of their earnings or returning cash to shareholders through the use of stock buybacks.

Long-Term Earnings Growth Expectations: Given the lower dividend payout ratios (and higher reinvestment in the company or use of cash to fund stock buybacks), it should not come as a surprise that high-yielding dividend payers had lower growth expectations than the potential dividend growers. Given similar price-to-earnings ratios, many might view the potential dividend growers as being more attractively priced, given their higher growth expectations.

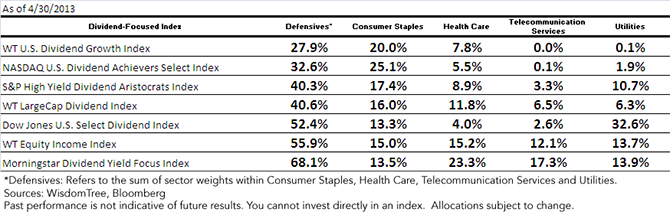

Exposure to Expensive-Defensives

For those who believe that the defensive sectors are relatively expensive, we discuss how various dividend-focused indexes are exposed to these sectors. We believe that many investors would think all dividend indexes were always heavily exposed and that they’d be surprised to learn that the exposure actually ranged from below 30% to nearly 70% as of April 30, 2013.

{kind=link}

• The WisdomTree U.S. Dividend Growth and NASDAQ US Dividend Achievers Select indexes focus on dividend growth, albeit in different ways. Their exposure to the defensive sectors was on the low end of the range.

• The Dow Jones U.S. Select Dividend, WisdomTree Equity Income and Morningstar Dividend Yield Focus indexes each incorporate dividend yield into their selection methodologies, leading them to having the highest exposure to defensive sectors of all the dividend-focused indexes shown.

• The WisdomTree LargeCap Dividend Index does not focus on yield or growth as part of its selection methodology and ends up in the middle position on this chart. The S&P High Yield Dividend Aristocrats Index does in fact weight its constituents by dividend yield, but the fact that it requires 20 consecutive years of dividend growth for its constituents lowers its exposure to the defensive sectors compared to the other yield-focused approaches.

Conclusion

While one can argue that the Consumer Staples, Health Care, Telecommunication Services and Utilities sectors are becoming expensive, since they’ve led the recent rally, we believe it is a mistake to make the generalization that all dividend payers are becoming expensive based on that fact alone. Additionally, there are dividend-focused indexes that do not have majority exposure to these sectors, so avenues exist through which one can apply a dividend focus without having to seek exposure to defensive sectors.

Jeremy Schwartz is director of research at WisdomTree Investments (NasdaqGM: WETF). This post was republished with permission from the WisdomTree blog.