Through the first quarter of 2013, eight out of ten G10 currencies depreciated against the U.S. dollar. With the Japanese yen leading the downward charge, investors in most developed markets sought the perceived safety of the U.S. dollar.

Two notable exceptions to the broad-based depreciation were the Australian and the New Zealand dollar. We believe investors will continue to be attracted to Australian debt, as it currently offers the highest yields of any AAA-rated sovereign in the world.1

o Increased Sponsorship: Official reserve currency status

o Highest Yields among Highly Rated Developed Market Sovereigns2

• Semi-government and supranational debt provide additional opportunities to enhance yield relative to sovereign debt

o Deepening of Trade Relations with China

• Reduced transaction costs/slippage

o Regional Economies Projected to Grow at Faster Rates

• Policy flexibility, should the Australian economy moderate

Reserve Currency Status Confirmed

In an update to a story we mentioned in February, the International Monetary Fund (IMF) has confirmed that the Australian dollar (along with the Canadian dollar) will be reported as a separate holding in the quarterly Currency Composition of Official Foreign Exchange Reserves (COFER) beginning in June 2013.3 While Australian officials have dismissed this as a “classification change,” we believe the Australian dollar joining other reserve currencies (among them U.S. dollar, British pound, Swiss franc and euro) could highlight Australian-denominated assets such as government bonds to individual investors.

{kind=link}

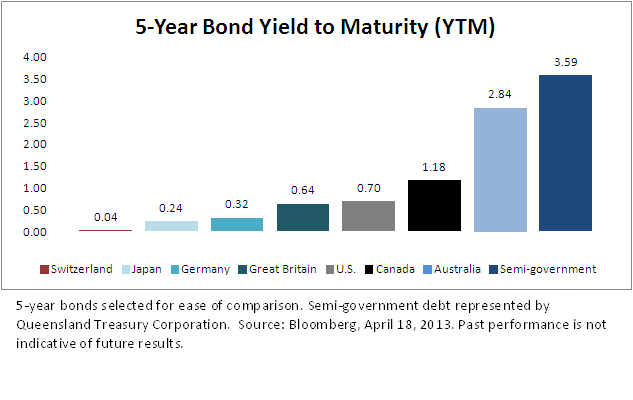

Australian Yields Compare Favorably to Other Reserve Currencies

As shown by the chart above, Australian government debt continues to offer a significant yield premium compared to other reserve currencies. Despite the rally in yields last year, Australian markets still provide attractive levels of income compared to most developed market peers. Among reserve currencies, Australian yields are significantly higher than those of Germany, Switzerland or Canada (the only countries rated AAA or equivalent by all three major ratings agencies). In addition to Australian government debt, a deep and liquid market of high-credit quality semi-government debt can offer additional opportunities for yield enhancement. Last year, we touched on the possibility of Chinese sovereign wealth funds increasing allocations to semi-government debt to take advantage of these higher yields. As of March 31, 2013, 89% of the US$648 billion in Australian debt outstanding was rated AA+ or better by S&P, Moody’s and Fitch.4

Direct Currency Trading with China