In my last post, we introduced you to the who of the ETF ecosystem. We defined the various types of market makers (MMs) and other market participants, and explained what role each plays in the everyday trading of ETFs.

Today we are going to discuss why these players are in the ETF ecosystem – how their business models differ and what motivation they each have for trading ETFs.

Why is this important? Simply put, the interaction between these different market players can lead to liquidity for the investing public. Furthermore, any of the recent discussions around regulatory changes for market makers – for example, their obligations within the marketplace – must start with the strategies these firms employ. This understanding may also help dispel fears around a potential breakdown in trading leading to illiquid markets in ETF securities.

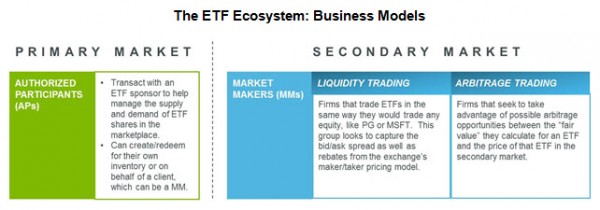

Of the many market participants, there are 2 main categories which facilitate ETF trading on a daily basis: Authorized Participants and Market Makers. The visual below explains how each interacts with ETFs on a regular basis.

{kind=link}

Authorized Participants (APs)

On the primary market side, Authorized Participants provide a service by transacting with an ETF sponsor to manage the supply and demand of ETF shares in the marketplace. Some APs will create and redeem new shares to manage their own inventory, while those who do not engage in market making simply facilitate creations and redemptions on behalf of their clients (which could include market makers). Even the concept of ‘create to lend’ – creating new shares in order to lend them to a short seller– is simply another example of client facilitation.

Market Makers (MMs)