The average yield on the 10-year note over the past five decades was 6%, or closer to 7% if the spike in the early 1980s to nearly 16% is included.

Dehn thinks yields in heavily indebted developed countries like the U.S. are “vulnerable” with central banks pushing rates to all-time lows in the aftermath of the 2008 financial crisis.

Consumers are deleveraging while central banks are becoming more reluctant to support the market with additional stimulus. “There is no precedent for reversing QE of the magnitude currently in place,” Ashmore said.

Clearly, record-low bond yields in traditional safe havens such as the U.S. Germany show that investors are indeed more concerned with return of capital than return on capital.

There are several scenarios in which Treasury yields could move higher and punish bond investors. They could rise for “unhealthy” reasons such as concerns over the massive debt load in the U.S.

Or they could rise for “healthy” reasons as markets anticipate an improving economy or a resolution of the debt crisis in Europe.

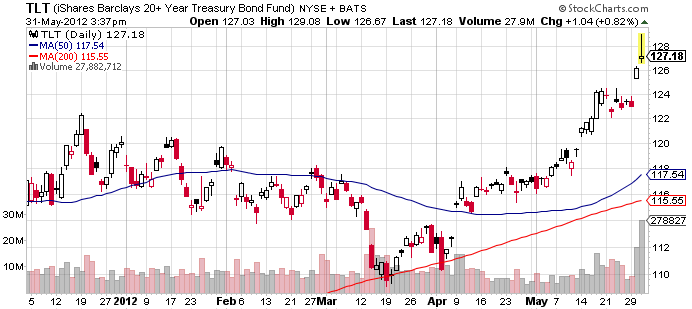

The strength of Treasury ETFs this month is a victory for diversification and asset allocation because bonds have provided shelter from the sell-off in equity and commodity markets.

However, investors who have piled into Treasury ETFs should at least have an exit strategy in place.

iShares Barclays 20+ Year Treasury Bond Fund

{kind=link}