Not all that glitters is gold, but reader interest is high for ETFs that invest in the precious metal. Since the start of the year, gold ETFs have been one of the top ten research themes on the VettaFi platform. This week, the VettaFi Voices came together to talk about the diverse offering of gold-related ETFs available for investors right now.

Todd Rosenbluth, director of ETF research: Gold remains a hot topic for advisors, and they certainly are doing research on these ETFs on VettaFi. But year to date, its ETFs have seen approximately $640 million of net outflows, while in the past year, gold ETFs have seen $11 billion of net outflows. The SPDR Gold Shares ETF (GLD) and the iShares Gold Trust (IAU), the two largest ETFs of the bunch, are bleeding assets in 2023, only continuing the trend.

The lone bright spot has been the SPDR Gold Minishares Trust (GLDM), which is a less expensive version of GLD that has seen inflows this year ($595 million). Over the past year, it has taken in $1.1 billion in flows. But the abrdn Physical Gold Shares ETF (SGOL) and iShares Gold Trust Micro ETF of Beneficial Interest (IAUM), both also cheap, are incurring redemptions.

I’m all for advisors to pay less for the same exposure. But in general investors concerned about taking on risk are turning more to short term Treasuries ETFs over the metal. ETFs like the iShares Short Treasury Bond ETF (SHV), the SPDR Bloomberg 1-3 Month T-Bill ETF (BIL), and the WisdomTree Floating Rate Treasury Fund (USFR) are much, much more popular in part because they sport 4% yields. Gold ETFs provide no income.

Lara Crigger, editor-in-chief: You’re not wrong, but we have to define what we mean by “cheap.” Which gives me an excuse to talk about one of my favorite overlooked stories in investing — the importance of a reasonably sized handle!

Yes, GLD has an expense ratio of 40 basis points, while GLDM has an expense ratio of 10 basis points. But that’s not the full story as to why for years, GLD, the oldest and largest physical gold ETF, has been losing market share to other funds, like IAU.

It’s also because GLD has a huge share price. As of mid-day on Thursday, GLD’s share price was about $170 per share. IAU, meanwhile, has a share price of $35 per share.

That difference in price isn’t arbitrary — it’s because each share of GLD represents 1/10th of an ounce of gold, while each share of IAU represents 1/100th of an ounce. Less metal per share brings down the size of IAU’s handle, making it more accessible for retail investors and smaller advisors, who still want to allocate to gold but tend to trade in smaller, cheaper lot sizes. Hence why IAU has for years been seeing steady inflows, while GLD tends to sees much more vibrant trading activity — it remains the preferred vehicle for institutions.

It’s also why the World Gold Council launched GLDM. GLDM is basically the same product as GLD, and by the same issuer, except it also has a smaller gold-per-share ratio (1/100th of an ounce, same as IAU). And if that wasn’t enough, its expense ratio is only ten basis points, making GLDM the gold ETF with the lowest price tag as well.

Rosenbluth: Good point, Lara, on the share price. The old school ETFs like GLD are harder to allocate a small slice of a portfolio and make rebalancing moves on a regular basis, compared to GLDM. That helps explain its growing asset base.

Dave Nadig, financial futurist: I tend to think of gold very differently than any other asset. It’s the only publicly acceptable form of psychological commodity, by which I mean that at any given point in time, its price is determined nearly completely by the willingness of someone else to buy it from you, right now.

While it’s true that the price of anything is essentially what you can sell it for, with every other kind of asset, we have other reasons to own it. We own a stock because we get a claim on a business: its profits, its growth, its assets, its potential value in a sale. We own a bond for the coupon stream. And so on. Even other types of commodities offer additional motivations for ownership. If you buy an oil ETF, like the United States Oil Fund LP (USO), then you do so because you believe this critical economic input will face scarcity; meaning, you believe that in the future, it will be more valuable than the cost of your cash. But gold is different.

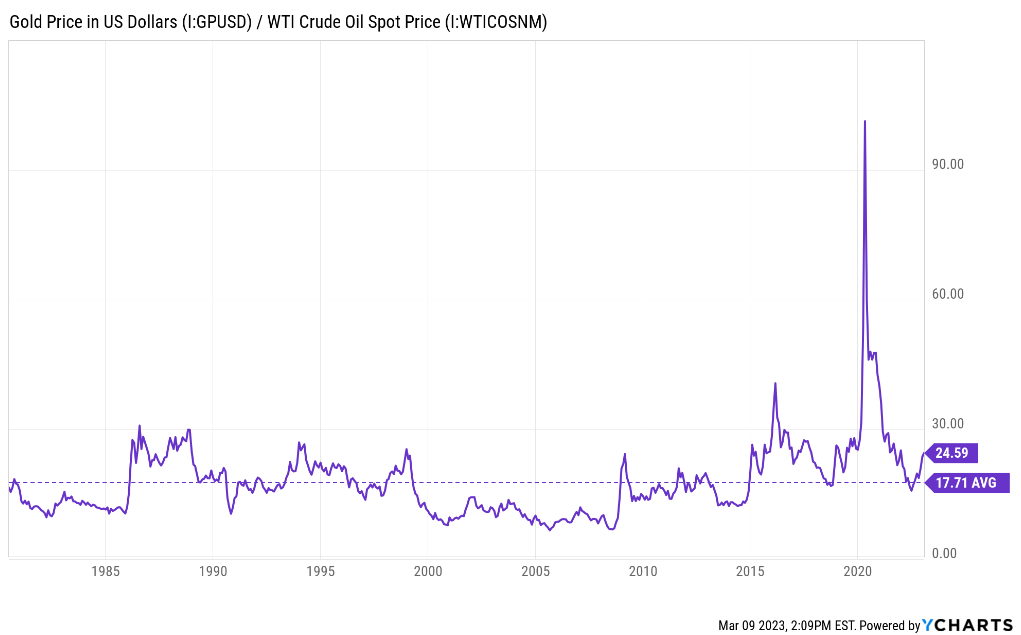

When you think about its value, the most important question to ask is, “Gold versus what?” For example, this is how many barrels of WTI crude you get for an ounce of gold (the long term average is about 17.71):

In other words, it is well above its long term average price, in terms of energy buying power.

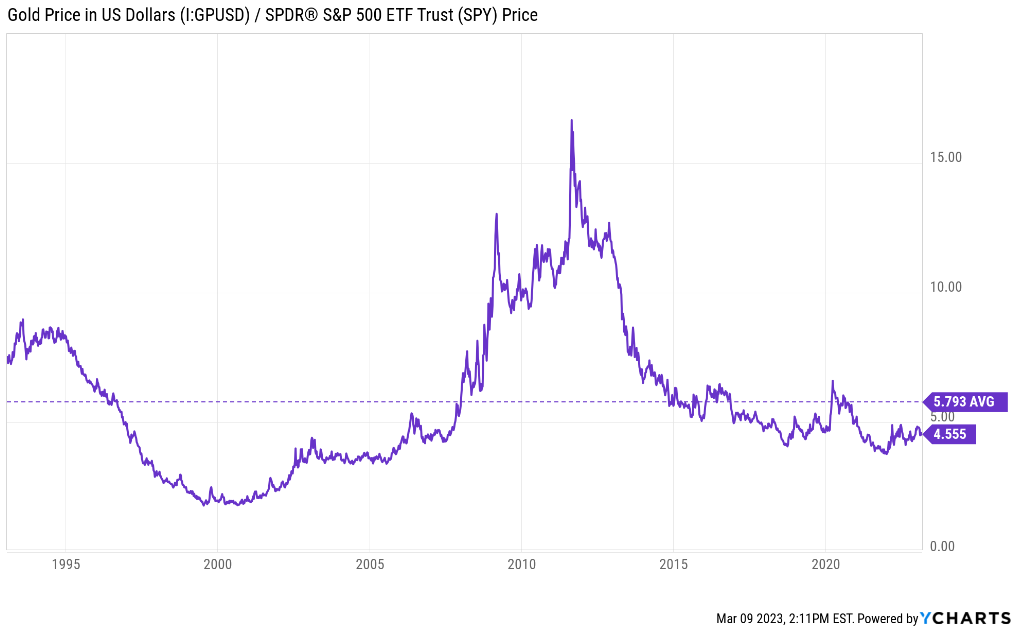

But what if you’re comparing it to the overall price of the S&P 500 Index?

In that case, gold’s value is a little below the long term average.

Since it has no intrinsic value as a producing financial asset, you always have to ask why someone will pay you more for this same allotment of gold at a later date. Historically, the answer was that it would hold value in terms of inflation, but with real yields still positive despite inflation, you now have to look at what cash does for you.

That’s the sort of mainstream, green-eyeshade asset allocation perspective. Of course, a LOT of people buy for much less mathematical reasons: they see it as a completely independent store of value to protect against major collapses, be at the economic, country, or system level. I don’t have much to say to folks who are doing that; I’m not personally much of an apocalyptic, so I don’t personally see the value of sticking gold in a safe. And putting gold in your ETF and holding it in your brokerage account would make it lose its “out of system” qualities anyway.

Roxanna Islam, associate director of research: But because it is a type of psychological commodity, as you said Dave, I think that mainstream narrative is extremely important when analyzing what’s happening to gold in terms of price and demand.

When Powell made hawkish comments on Tuesday about rates staying higher for longer, we saw gold prices drop. A lot of the divergence has been because of this scenario we’re in, where rates might stay higher and keep the dollar stronger but at the same time people are fearing a recession and trying to flee to “safety.” So it’s been really difficult to say what happens next, because so much of it is based on sentiment, and currently that sentiment is mixed.

Rosenbluth: I agree that the monetary policy uncertainty is playing a role. While earlier I talked about fund flows, I think advisors using gold in their client portfolios should focus on the lower cost products like GLDM or the Franklin Responsibly Sourced Gold ETF (FGLD) because they provide the same exposure as the larger funds but with less of a cost drag on the portfolio.

Nadig: There’s certainly no reason to over pay for “gold beta,” Todd, absolutely. And Roxanna you’re totally right — it’s essentially all sentiment. So you should expect its price to react to headlines along its traditional narratives (crisis, inflation, safety, etc.), as everyone tries to reposition for a new trend with each new news bite.

Crigger: I want to circle back to Todd’s point about ESG in gold, because although the precious metals industry often gets dinged for its ESG violations, truth is there’s actually a fair bit of work being done by the big gold miners in improving, say, labor violations, environmental mitigation, and general responsibility in supply chain sourcing. Sure, it’s not butterflies and rainbows, but it’s also a lot better than many other commodity supply chains, that’s for sure. (Just look up how cocoa and coffee are produced. Or the cobalt in your smart phones.)

The World Gold Council has been leading the charge here with its Responsible Gold Mining Principles. Skeptics are gonna skeptic, to be sure, but as somebody who refuses to buy or be bought diamonds and other conflict gems, it’s encouraging to see an industry actively attempting to move away from conflict gold. In fact there are even now two ETFs that focus on conflict-free gold, FGLD and the Sprott ESG Gold ETF (SESG).

Rosenbluth: What about gold miner ETFs? They’re seeing lots of inflows. Van Eck’s Gold Miners ETF (GDX) has seen $230M, while its small cap version the VanEck Junior Gold Miners ETF (GDXJ) has seen more modest flows despite declining in value.

Islam: Gold miner ETFs are an area that’s not as well-known with investors, but which has some interesting aspects to it. In short, any sort of commodity miner is typically a leveraged play on that commodity and tends to do much better when the commodity price rises and or much worse when the price falls. It makes sense if you think about it — if gold prices go up, then gold mining companies should have higher margins and likely higher free cash flow to either reduce balance sheet debt, pay back to shareholders, or invest into operations. And if they manage these profits well, then they might even be able to survive better through times when gold prices are weak. So it’s an intriguing area for investors that are bullish on gold and/or interested in investing in equities rather than commodities.

Crigger: That said, gold miner ETFs are just getting creamed, both in the short-term (YTD) and long-term (1-3 years). You have to look out to a 5 year basis to see anything other than the inverse-leveraged products seeing positive returns. Maybe that’s a buy-the-dip opportunity for the optimistic investor, though, I don’t know.

Islam: There have been some periods of relatively recent outperformance, but there’s certainly different risks vs. investing in gold. I would say that there is probably a niche group of investors interested in gold mining ETFs vs. gold ETFs which have a wider appeal. One of the cool aspects of ETFs though — there’s something out there for every type of investor.

For more news, information, and analysis, visit the Gold/Silver/Critical Minerals Channel.