![]() By Gary Stringer, Kim Escue and Chad Keller, Stringer Asset Management

By Gary Stringer, Kim Escue and Chad Keller, Stringer Asset Management

A Goldilocks economy may be defined as an economy that is neither too hot nor cold, sustains moderate economic growth, low inflation, and allows for a market-friendly monetary policy. We think the U.S. economy falls within the Goldilocks definition at this time.

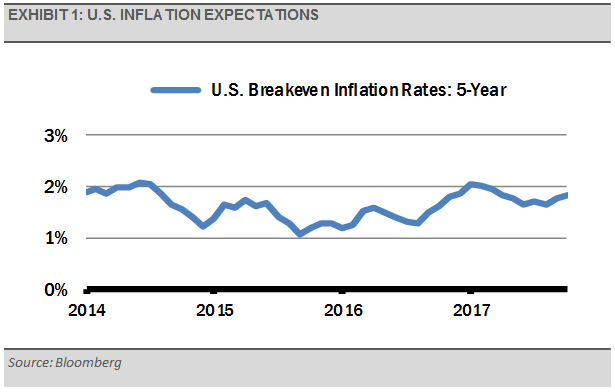

Domestically, market-based inflation expectations are showing a lack of inflationary pressure (exhibit 1), so we do not see a need for the U.S. Federal Reserve (Fed) to alter their current course. A slow reduction of the U.S. balance sheet and gradual rate hikes should be fine as long as the yield curve does not flatten significantly.

Additionally, Jerome Powell will likely take over for Janet Yellen as Chairman of the U.S. Federal Reserve in February, assuming the Senate confirms him, and is expected to keep the Fed on the same course. We think the change in leadership will cause little disruption.

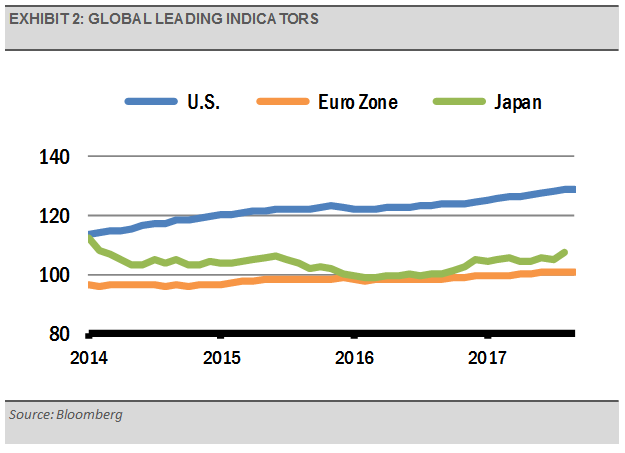

Globally, leading economic indicators are advancing nicely, which suggests continued economic momentum for the world’s major economies (exhibit 2).

For example, October manufacturing surveys, a component of the leading economic indicators, demonstrate that developed economies, such as the U.S., euro zone, and Japan, continue to perform well. As a result, the global manufacturing surveys rose to their highest level since early 2011. In fact, the U.S. economy looks to have been particularly resilient in the face of Hurricanes Harvey and Irma.

For instance, consumer spending is up, as is business investment, which offsets the lack of business lending growth. Even productivity, which is a key input to economic growth, came in at a strong 3% last month. Meanwhile, the recent depreciation of the U.S. dollar should add a tailwind to the already strong global demand for U.S. exports.

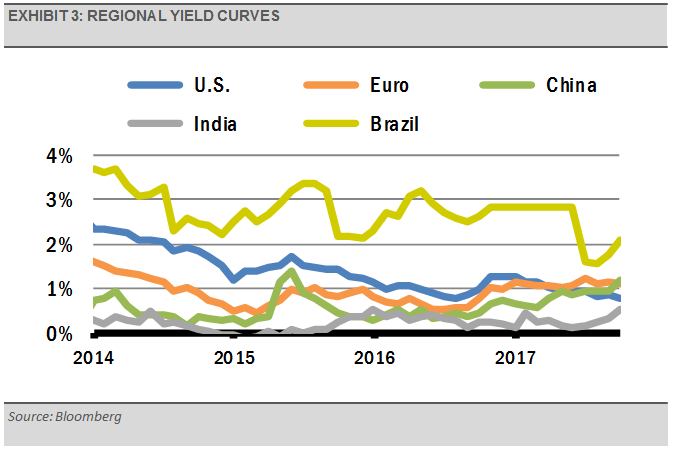

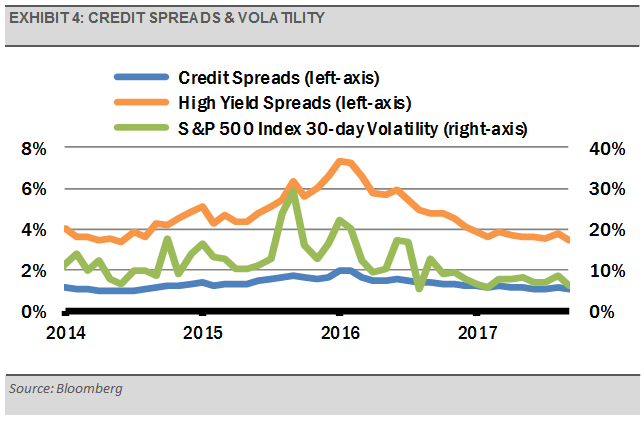

The fixed income markets also support the Goldilocks economic scenario. The U.S. yield curve, which is a sign of economic growth and inflation expectations, has flatten as a result of the Fed’s policy tightening. However, yield curve measures in Europe and the emerging markets look good (exhibit 3). Additionally, credit spreads, which tend to lead equity market volatility, project market stability for the months ahead (exhibit 4). While we expect an increase in equity volatility, we expect it to be limited.

Overall, it looks like smooth waters ahead as we steam into 2018. We think investors should take advantage of these positive trends through equity market exposure.

THE CASH INDICATOR

The Cash Indicator (CI) has declined to the low end of its historic range. While we expect market volatility to increase, the current level of the CI suggests that the environment for raising significant cash is a long way off. Market dips are likely buying opportunities.

This article was written by Gary Stringer, CIO, Kim Escue, Senior Portfolio Manager, and Chad Keller, COO and CCO at Stringer Asset Management, a participant in the ETF Strategist Channel.

DISCLOSURES

Any forecasts, figures, opinions or investment techniques and strategies explained are Stringer Asset Management, LLC’s as of the date of publication. They are considered to be accurate at the time of writing, but no warranty of accuracy is given and no liability in respect to error or omission is accepted. They are subject to change without reference or notification. The views contained herein are not be taken as an advice or a recommendation to buy or sell any investment and the material should not be relied upon as containing sufficient information to support an investment decision. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested.

Past performance and yield may not be a reliable guide to future performance. Current performance may be higher or lower than the performance quoted.

The securities identified and described may not represent all of the securities purchased, sold or recommended for client accounts. The reader should not assume that an investment in the securities identified was or will be profitable.

Data is provided by various sources and prepared by Stringer Asset Management, LLC and has not been verified or audited by an independent accountant.

Index Definitions:

S&P 500 Index – This Index is a capitalization-weighted index of 500 stocks. The Index is designed to measure performance of a broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.