Options-based strategies appear here to stay, as broad adoption remains ongoing for institutional and retail investors alike. One firm, NEOS Investments, continues to carve out market share within the space.

NEOS recently celebrated the two-year anniversary of the launch of its flagship funds. These include the NEOS S&P 500 High Income ETF (SPYI), the NEOS Enhanced Income 1-3 Month T-Bill ETF (CSHI), and the NEOS Enhanced Income Aggregate Bond ETF (BNDI). I sat down with Troy Cates, co-founder and co-PM at NEOS Investments, to discuss the journey of the last two years and what’s on the horizon for the firm.

NEOS Brings Seasoned Options Investing Experience to ETFs

Karrie Gordon, staff writer, VettaFi: Troy, thank you so much for taking the time to sit down with me. First of all, congratulations on the two-year anniversary of SPYI, CSHI, and BNDI. Let’s start this off by talking about the firm and the experience NEOS brings to options investing.

Troy Cates, co-founder, co-PM at NEOS Investments: At NEOS, we’re a global asset manager. NEOS, as you know, stands for Next Evolution Option Strategies — it’s what we focus on, and it’s all that we do. We use quantitative approaches to deliver yield enhancement strategies through an ETF structure. Our team is made up of seasoned professionals that have been together for a number of years. We also manage our own products — we’re the ones who research and spend time building these products, and then managing them.

My co-founding partner, Garrett Paolella, and I have been working together for over 15 years, and this is our second venture together in the options-based ETF space. We’ve both been involved in the ETF space for well over a decade and we’ve launched a number of ETFs over those years, including some of the early options-based ETFs that were some of the first to pay monthly income. The space has grown tremendously over that time frame.

We launched NEOS a little over two years ago, and our goal was to offer a suite of ETFs that bring institutionalized option strategies to the investing public. Our ETFs are all active in nature, but rooted in a data-driven and systematic approach. What’s especially cool about the ETF structure is how accessible it is. Anybody that can buy one share of our ETFs can be invested in our strategies. Traditionally, these types of options strategies came with higher fees and minimum investment requirements.

We really pride ourselves at NEOS on being available. Whether it’s somebody writing into the website or it’s an advisor calling one of our sales professionals saying – “I want to dive into your options strategies to better understand them and help my clients get comfortable with it as well.” – Garrett and I, as the two portfolio managers, are available.

A Look at the Fundamental NEOS Strategy

Gordon: The strategy itself is one that focuses on high income and tax efficiency across a number of asset classes. Can you step through how the strategy works, because I know it’s using different kinds of options in different funds — calls in some, and puts in others?

Cates: In our equity suite, we have three ETFs; SPYI, QQQI [NEOS Nasdaq 100 High Income ETF], and most recently, IWMI [NEOS Russell 2000 High Income ETF]. Those ETFs all use the call side of the option chain. We’re using index options in all the ETFs for added tax efficiency.

Index options are treated as Section 1256 Contracts, where they get 60% long-term cap gains, 40% short-term cap gains, no matter the holding period. Let’s look at the portfolio of SPYI as an example. You’re long a basket of 500+ stocks that represent the S&P 500, and you have an SPX index option short call overlay on top of it that aims to generate income, which helps fund the monthly distribution payments to shareholders. . Investors can pursue both high monthly income and tax efficiency from our equity products.

Now, on the other side, you have the fixed income products. We have two: CSHI and BNDI. In those two products, we’re using the put side of the option chain, using SPX index options. So, you’re still getting that tax-efficient use of the index options, but using puts. And we’re doing put spreads — those are a little different.

We roll those on a weekly basis, because we want to make sure we don’t get too close to where [the]spot [price]is for the S&P 500. We want to make sure we’re staying out-of-the-money on those, but slowly bringing in additional income.

CSHI is more of a lower volatility, ultra-short duration portfolio with 1-3 month T-bills and the put spread overlay. The goal is to give you an extra 1.0%-1.5% a year over what T-bills yield. For BNDI, a similar strategy, rolling weekly with SPX index put spreads, trying to bring in an additional 2.0%-2.5% and matching up the risk of the underlying portfolio.

These funds aren’t so much targeting a yield as matching the risk with the option portfolio to the underlying. We’re trying to maintain a similar volatility profile while generating that added income.

SPYI, CSHI & BNDI 2 Years Later

Gordon: You took this options overlay strategy and you launched SPYI, CSHI, and BNDI two years ago. Would you tell me about your decision to bring this kind of strategy to market and what the reception has been?

Cates: So, when we launched in August of 2022, we really wanted to start with these three ETFs to cover a core asset allocation of equities, fixed income and cash/ultrashort duration. SPYI with its broad equity exposure for our first equity, high income ETF utilizing the S&P 500. Then on the fixed income side, we really wanted to have that ultra-short duration product with the enhanced 1-3 month T-bill ETF, and that’s CSHI. Then we also wanted something more in the core bond space, so we built out BNDI as well.

We thought that if you look at your asset allocation pie, it really slices it up nicely. There’s probably something there for everyone. And as we’ve grown from there, we’ve slowly started to slice up more of the equity pie.

We will continue to cut up that pie to offer more ETFs to income-focused investors looking for this type of exposure. But the three initial ETFs have done really well since inception. Performance has been in line with what we had expected for these products in this market environment, the AUM raise has been amazing, and we’re really excited to continue to watch these products grow.

Enthusiastic Investor Uptake of NEOS ETFs

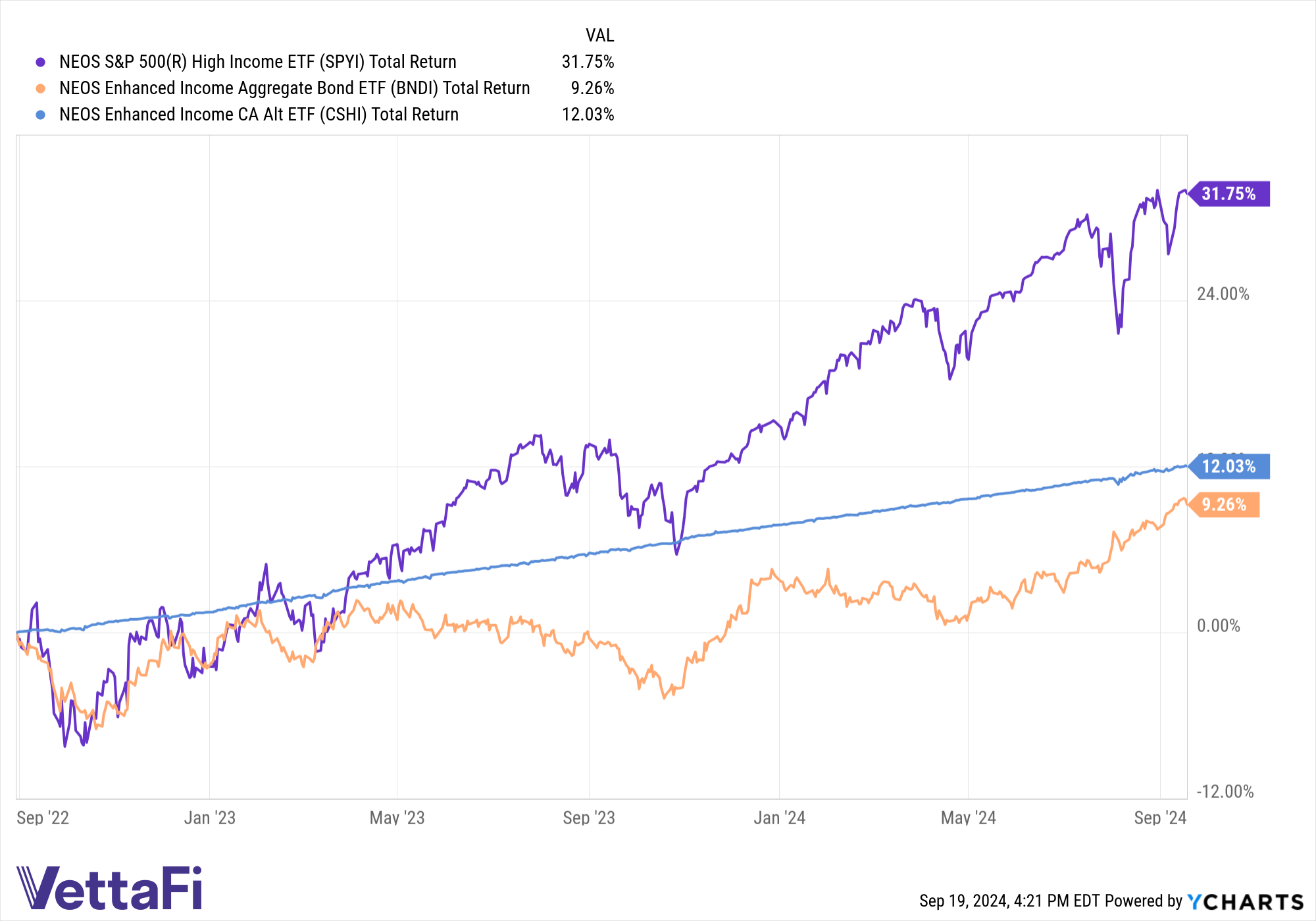

Gordon: Touching on the AUM, SPYI continues to prove enormously popular, with over $1.9 billion in assets currently. CSHI has over $500 million, and QQQI, launched a little over six months ago, is nearing $500 million in AUM. And that’s largely been retail and individual advisors, correct?

Cates: There’s a large advisor community that can buy into these funds early on. Whether it’s some of the independents or RIAs, they can really dive into these strategies with us. As the option-based ETF space has grown, more and more advisors have been using these products. They also understand these products at a much deeper level than ever before. We’re thankful to have built a strong following in the advisory community and are excited to continue that.

There’s also been a very large retail following. I think it goes along with how much this space is growing. Some of the biggest active ETFs in the marketplace are option-based ETFs. People, whether they’re in their 20s or 60s, are talking about bringing in income on a monthly basis.

Ten years ago, many people later in their investing life cycle were looking at these kinds of products as a bond replacement. Now we’ve also seen younger people wanting to build out income allocations earlier in their investing lifecycle. They have the freedom to reinvest the dividends, letting it build it until they need the actual payments down the road. They can also take the distributions to supplement other income streams they may have. This space has grown so much recently and as a result, so have the potential portfolio applications of these products.

data as of 08/31/24

Image source: NEOS

Expanding the Strategy’s Coverage in New Offerings

Gordon: You started with the core suite two years ago, and now you’ve expanded to include small-caps and the Nasdaq-100. How do you decide what asset class you believe is best for this strategy?

Cates: For us, it’s where we are seeing demand. We’re not an ETF issuer that’s just going to throw out tons of ETFs and see what sticks. We are thoughtfully bringing out institutional quality, option-based ETFs where there’s a demand. It’s where advisors currently invested in our products ask if we’re bringing out anything in this space.

We spend a lot of time researching and thinking about the option portfolios that will go along with the underlying equity or fixed income portfolios. We currently have five ETFs out and have two that we are in the middle of proxies and trying to bring over. One is an ETF where we were subadvisors for Nationwide. The other one is a high yield bond mutual fund that’s been out for years, which we’ll aim to enhance with an option overlay after converting it to an ETF.

We also have another fund in registration, and we have some more that we’re going to file for soon. We’re not trying to bring out a ton of funds at once because we want to be really thoughtful about the ETFs. This way we can support them with client service efforts, the portfolio management side, and on the broader distribution side.

How to Think About Portfolio Allocation

Gordon: With so many more people looking at and investing in these types of funds, what kind of portfolio allocation do you suggest? How do they fit into an income portfolio? Are they replacements or complements?

Cates: This space has grown so much. The last time I looked, there’s well over 400 options-based products, whether ETFs or mutual funds. A lot of them may be expiration-date-type products, like buffered strategies. But there’s also a lot of income-focused options-based ETFs that continue to come to market across all types of asset classes with differing option overlays. I think anybody investing in the space needs to do their homework. And there’s so many good ways to do that now. We say education is key.

For example, whether it’s our ETF or another options-based ETF, you have to look at the total return. Distributions are different across all these different options ETFs, but is the total return enough to support the distribution? We always try to build products where the underlying distribution that’s going out on a monthly basis can be supported by the total return. It’s also crucial to understand what’s in the portfolio. Is it tax efficient? That’s an important aspect, especially for advisors that we talk to.

It’s not so much a one-to-one replacement conversation anymore with advisors. Income portfolios are becoming more sophisticated. We’ve talked to advisors that might say, “I’m taking this ETF out to put in a NEOS ETF,” or “I’m leaving my current allocations and complementing it with a NEOS product because of the added tax-efficiency and high income potential.”

Gordon: Troy, as always, I appreciate your time and insight into this space and the NEOS funds. I look forward to seeing what’s next for the firm, and congratulations again on two years for your flagship ETFs.

For more news, information, and analysis, visit the Tax-Efficient Income Channel.