By Natalia Gurushina, Chief Economist, Emerging Markets Fixed Income Strategy, VanEck

Turkish assets are under pressure – in part due to thin pre-holiday liquidity, but also due to skepticism about the reform agenda. South Africa’s double rating downgrade – not surprising but not welcome either.

Turkish assets got “roasted” early during the Thanksgiving week, with the lira weakening by as much as 4% at some point in the morning trade. Thin liquidity and some profit-taking might be to blame, but we suspect that there is also some “buyers’ remorse” as authorities are yet to prove that the policy U-turn is genuine. The last week’s rate hike was a good start, but the central bank did not over-deliver, and President Tayyip Erdogan’s dislike of high interest rates remains an issue. The market is also waiting for more information about the new Minister of Finance’s policy agenda.

South Africa’s double rating downgrade by Moody’s and Fitch (with negative outlooks) had a limited market impact. First, it was not completely unexpected – the country’s fiscal metric is among the weakest in emerging markets, the debt-to-GDP ratio is rising fast, and there are major structural impediments to growth. Second, the sovereign had already been rated “non-investment grade” by all three agencies. That said, further rating downgrades to single-B can affect bond investors with mandate restrictions – which is why we keep a very close eye on South Africa’s structural developments and reform plans.

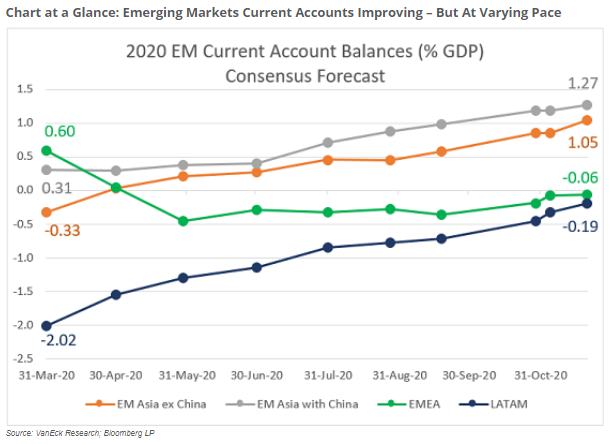

The current account outlook for emerging markets continues to improve, with the 2020 expected surplus gradually approaching 1% of GDP (compared to 0% of GDP back in April-May). However, there are regional differences. The largest surpluses are expected in Asia, but the biggest adjustment (nearly 2% of GDP) is seen in LATAM (see chart below).

Originally published by VanEck, 11/23/20

IMPORTANT DEFINITIONS & DISCLOSURES

PMI – Purchasing Managers’ Index: economic indicators derived from monthly surveys of private sector companies; ISM – Institute for Supply Management PMI: ISM releases an index based on more than 400 purchasing and supply managers surveys; both in the manufacturing and non-manufacturing industries; CPI – Consumer Price Index: an index of the variation in prices paid by typical consumers for retail goods and other items; PPI – Producer Price Index: a family of indexes that measures the average change in selling prices received by domestic producers of goods and services over time; PCE inflation – Personal Consumption Expenditures Price Index: one measure of U.S. inflation, tracking the change in prices of goods and services purchased by consumers throughout the economy; MSCI – Morgan Stanley Capital International: an American provider of equity, fixed income, hedge fund stock market indexes, and equity portfolio analysis tools; VIX – CBOE Volatility Index: an index created by the Chicago Board Options Exchange (CBOE), which shows the market’s expectation of 30-day volatility. It is constructed using the implied volatilities on S&P 500 index options.; GBI-EM – JP Morgan’s Government Bond Index – Emerging Markets: comprehensive emerging market debt benchmarks that track local currency bonds issued by Emerging market governments.; EMBI – JP Morgan’s Emerging Market Bond Index: JP Morgan’s index of dollar-denominated sovereign bonds issued by a selection of emerging market countries; EMBIG – JP Morgan’s Emerging Market Bond Index Global: tracks total returns for traded external debt instruments in emerging markets.

The information presented does not involve the rendering of personalized investment, financial, legal, or tax advice. This is not an offer to buy or sell, or a solicitation of any offer to buy or sell any of the securities mentioned herein. Certain statements contained herein may constitute projections, forecasts and other forward looking statements, which do not reflect actual results. Certain information may be provided by third-party sources and, although believed to be reliable, it has not been independently verified and its accuracy or completeness cannot be guaranteed. Any opinions, projections, forecasts, and forward-looking statements presented herein are valid as the date of this communication and are subject to change.

Investing in international markets carries risks such as currency fluctuation, regulatory risks, economic and political instability. Emerging markets involve heightened risks related to the same factors as well as increased volatility, lower trading volume, and less liquidity. Emerging markets can have greater custodial and operational risks, and less developed legal and accounting systems than developed markets.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future performance.