Summary

Ukraine bonds collapsed following Russia’s invasion. At this time, we are accumulating bonds, as we believe a Ukraine that can finance itself easily is likely to emerge.

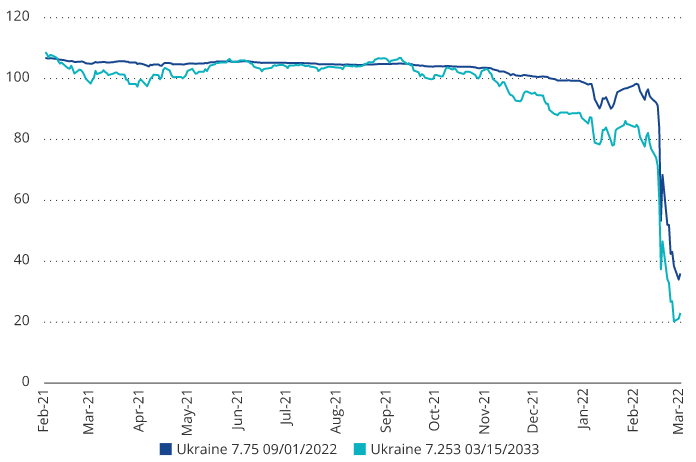

Ukrainian bonds just got very cheap relative to history. Ukraine bonds collapsed following Russia’s invasion. Exhibit 1 shows Ukraine ‘22s and ‘33s. The shorter-dated bonds are now trading at around 36 cents on the dollar, while the longer-dated bonds are trading around 23. The market is pricing in the certainty of default, clearly. If Ukraine muddles through to September, the upside is obviously dramatic. If Ukraine’s payment capacity is viewed as more permanently intact, then the upside for both the front- and long-ends is also obviously dramatic.

Exhibit 1 – Ukraine ‘22s and ‘33s

Ukraine International Bond Prices

Source: Bloomberg. Data as of March 8, 2022.

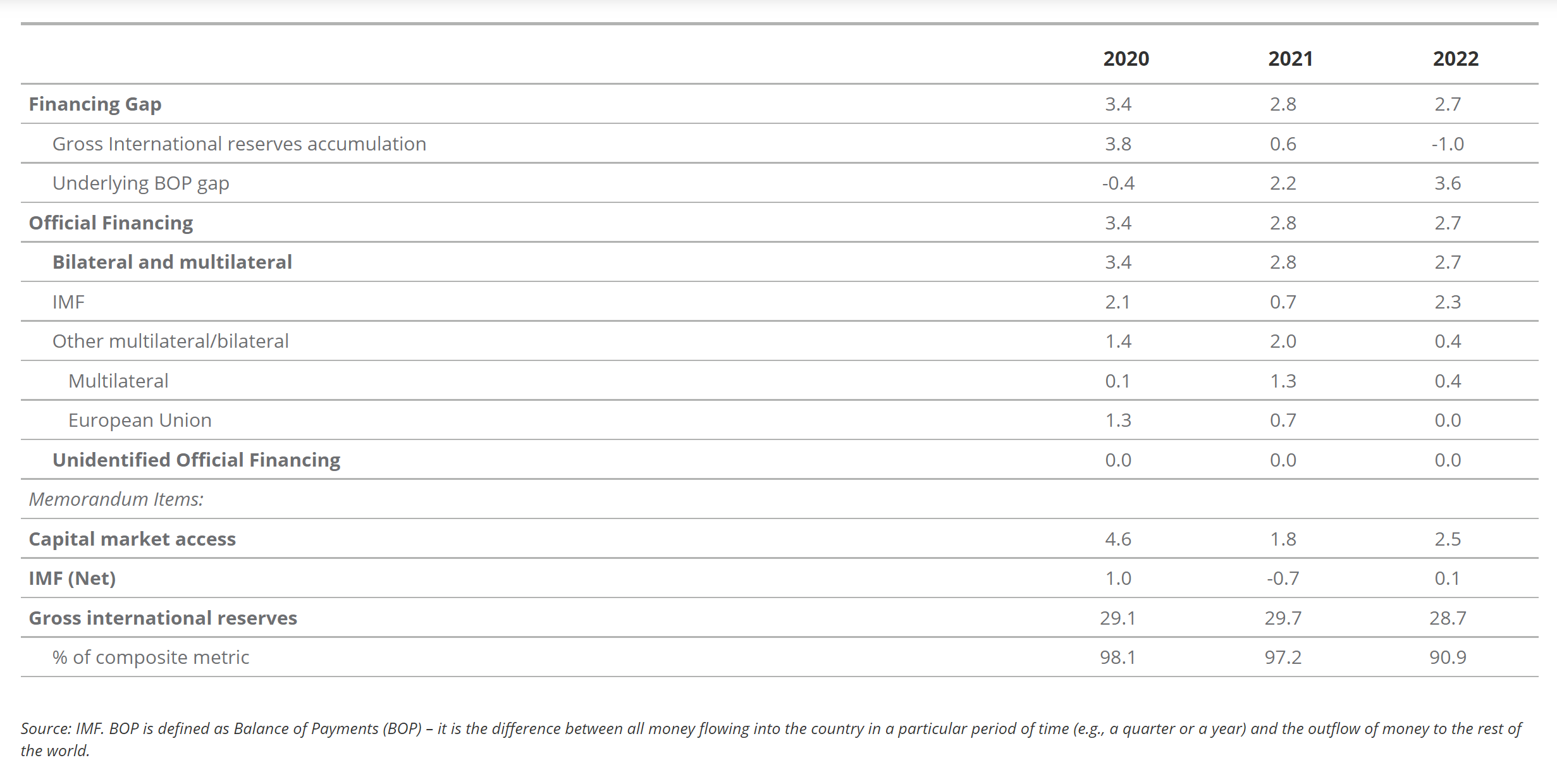

Ukraine is likely to finance itself. Exhibit 2 below shows Ukraine’s external financing requirement, and its financing, for 2020, 2021 and the forecast for 2022. The key thing to note is that 2022’s $2.7B was fully funded by the official sector, before additional support that is being announced for Ukraine.

Exhibit 2 – Ukraine’s External Financing in 2022

Ukraine: Program Financing (US$ billion)

Ukraine is looking better on what had been a key constraint to our owning it—its Policy/Politics Test score is improving, we believe. Now, the above simply says we believe Ukraine is cheap relative to history and can finance itself, which is pretty important. But, of course, Ukraine faces the ultimate political challenge—an invasion. Luckily, our process incorporates such non-systematic risks. This is the point of Step 2 of our investment process. After Step 1, in which we generate a list of what we view as the cheapest bonds in emerging markets (“EM”) based on a purely systematic and quantitative framework, we have Step 2. Step 2 incorporates non-systematic risks, but on a consistent basis. We apply the Tests of Step 2 to all EM bonds and, luckily, important non-systematic risks such as invasion are fairly rare. We won’t bore you with all three Tests that make up Step 2, but the key one in the Ukraine situation is the Policy/Politics Test. Why are we assigning a less pessimistic/more optimistic score here?

There has been an outpouring of international support for Ukraine that dwarfs its external financing requirements. Not only is Ukraine already financed by official creditors, but the amount of financing that looks to be in the pipeline as a reaction to Ukraine’s invasion dwarfs current financing.

- First, the EU has just now welcomed Ukraine’s application to join the EU. EU accession and membership anchors policy (membership is conditioned on policy). But EU membership also comes with significant funding. In countries like Poland, for example, it provides around 10% of budget financing. EU membership has transformed policy and led to a convergence of credit spreads in virtually all Eastern European countries.

- The United States Congress is now considering legislation to provide Ukraine with $6-$10B in aid.

- The IMF has announced $1.4B in additional financing, through a Rapid Financing Instrument line (“RFI”).

- The IMF is likely to show great forbearance, reflecting the international community’s attitude. This is normal in situations like this, but the amount of international sympathy seems extremely high in this instance, based on our decades of looking at such programs. Practically speaking, what this means is that if “market financing” (in Ukraine’s case, assumed to be $2.5B of issuance) does not happen due to the invasion, the IMF is very likely to compensate.

- The Ministry of Finance of Ukraine informed us and other investors recently that all regions are continuing to provide revenues to the central government. Remember that Crimea, Donetsk, and Luhansk (the latter two just seceded from Ukraine) are already excluded from Ukraine’s financing assumptions, so this risk is already reflected.

- The Ministry of Finance pledged to continue paying its obligations and paid the coupon due on February 28, 2022.

- Military spending could increase, but recent pledges by Germany and the EU make that likely to be foreign-funded going forward.

- There will be large reconstruction costs, but we see these as likely to be funded by international bilateral and multilateral agencies. EU accession will be part-and-parcel of this. Also, all capex in Ukraine is obviously frozen, currently, so many of those resources could be redeployed after hostilities are ended.

Our bottom line is that Ukraine bonds reflect the fact of the invasion, but not the likelihood of new international support. As a result, we are accumulating bonds. We don’t discount that as Russia takes Kyiv, Ukraine bonds could suffer more. But, when the dust settles, we believe a Ukraine that can finance itself easily is likely to emerge. We obviously can’t wait until that scenario becomes obvious, as the bonds will have gapped upward. As a result, we’re accumulating.

To receive more Emerging Markets Bonds insights, sign up in our subscription center.

IMPORTANT DISCLOSURES

Not intended as a recommendation to buy or to sell any of the securities mentioned herein. Holdings will vary for the Funds and their corresponding Indices.

Please note that the information herein represents the opinion of the portfolio manager and these opinions may change at any time and from time to time and portfolio managers of other investment strategies may take an opposite opinion than those stated herein. Not intended to be a forecast of future events, a guarantee of future results or investment advice. Current market conditions may not continue. Non-VanEck proprietary information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of Van Eck Securities Corporation © 2022 VanEck.

Investments in emerging markets bonds may be substantially more volatile, and substantially less liquid, than the bonds of governments, government agencies, and government-owned corporations located in more developed foreign markets. Emerging markets bonds can have greater custodial and operational risks, and less developed legal and accounting systems than developed markets.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future results.

Originally published by VanEck on March 11th, 2022