By Joe Foster, Portfolio Manager, Gold Strategy, VanEck

Gold Correction

U.S. dollar strength kept pressure on gold throughout September. The dollar, as measured by the U.S. Dollar Index (DXY),1 trended higher as the stock market trended lower from its all-time highs. The pandemic stimulus-driven bull market looks to be in jeopardy as the S&P 5002 fell sharply at the beginning of the month and the dollar responded to the risk-off sentiment. Gold may have seen additional pressure as a source of cash from equity-related margin selling. Gold had been consolidating above $1,900 per ounce since its $2,075 high on August 7. The consolidation now looks more like a correction as gold fell to a near-term low of $1,848 on September 28. For the month, the gold price declined $81.98 (4.2%), ending at $1,885.82 per ounce. The bottom of the current gold bull market trend is around $1,800. We expect this correction to remain above this level.

Gold miners retreated with gold, as the NYSE Arca Gold Miners Index (GDMNTR)3 fell 7.4% and the MVIS Global Junior Gold Miners Index (MVGDXJTR)4 declined 7.6%.

Miners Remain On Point, Operationally

We attended the virtual versions of the Precious Metals Summit and Gold Forum Americas (a/k/a The Denver Gold Forum). The Precious Metals Summit features Junior companies,5 most of which are cashed up from recent equity raises. As a result there was an abundance of drilling results, project updates and plans for more drilling. In our view, with new money comes new discoveries. Several of our companies have recently announced discoveries that we believe will help advance their projects toward production. For example, De Grey Mining looks to have a multi-million ounce discovery in the Pilbara region of Western Australia. Corvus Gold has made additional discoveries at its Southern Nevada project that may turn it into a district-scale play. Galway Metals’ drilling has turned some isolated gold occurrences into a trend that may host over a million ounces in New Brunswick, Canada.

The Gold Forum Americas conference reiterated and enhanced the industry trends that we have been talking about for several years. Large gold producers tripped over each other to inform investors of their cash-generating ability and commitment to return money to shareholders through increasing dividends and/or share buybacks. Balance sheets are pristine, as those who aren’t already in a net-cash position should get there by early 2021. While there isn’t much growth amongst the large companies, many emphasized sustainable production bases for ten years. Newmont (6.8% of net assets) even went beyond, indicating it can sustain current annual production levels of around 6 million ounces into the 2040s. In the past we were lucky to get five years of guidance. Most companies continue to use conservative pricing in the $1,200 to $1,300 per ounce range to calculate reserves and project economics. Companies also expressed a commitment to increasing Environmental, Social and Governance (ESG) initiatives. All of this bodes well for gold equity investors and demonstrates the sustainable financial and operating strength of the industry.

Still, Room For Improvement

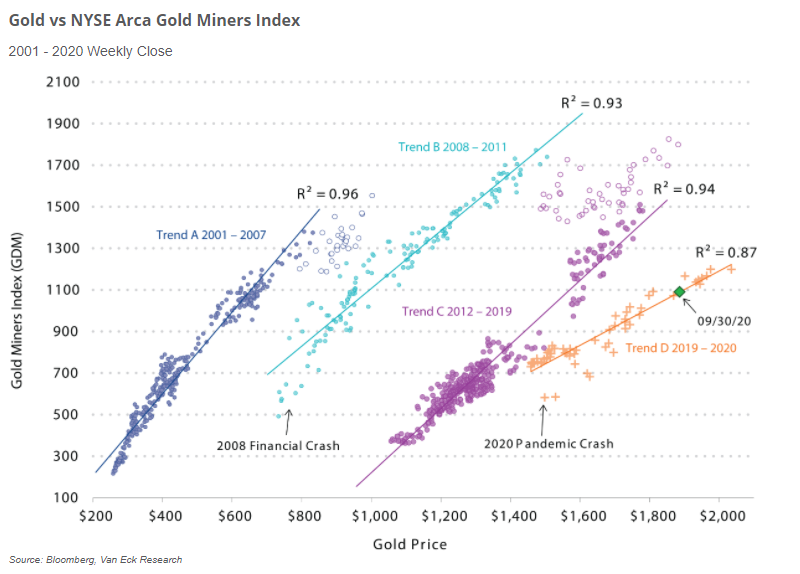

In August, gold reached its all-time high of $2,075 per ounce. At the same time the GDMNTR topped out at 1,271, far below its all-time high of 1,855 in September 2011 when gold reached its former high of $1,921. Since the current bull market began in December 2015, gold advanced 98% to its August 2020 high, while GDMNTR gained 266% over the same period. If the GDMNTR had returned to its old 2011 high of 1,855 in August of this year, it would have advanced 435% since the current bull market began. Here we explore the reasons that gold miners have not reclaimed their all-time highs with gold.

This chart below plots gold versus gold miners (as measured by GDMNTR). Notice that gold and gold miners trade along four discreet trends that have shifted to the right over time. Within each trend, the extent to which gold miners’ price movements can be explained by gold price movements (as measured here by the coefficient of determination, or “R-squared”6) is very high—near 1.0, or nearly 100% of the time in some cases. Alternatively, trend shifts to the right indicate that a given gold price movement corresponds to a lower gold miner price movement than in a preceding trend. In other words, gold miners have been de-rated relative to gold. Also, flatter trend lines indicates lower gold miners’ price beta7 to gold (beta being the performance leverage gold miners naturally carry to gold).

The chart shows that gold miners have suffered three de-ratings8 since 2007, with their beta to gold declining as well. The first two de-ratings occurred in late 2007/early 2008 and late 2011/early 2012 (trends A-B-C). These were caused by poor operating and financial performance on many fronts. Cost inflation eroded the operating leverage that investors expected. Rising costs also caused capital projects to fall short of expected returns. Companies made a habit of missing their production and cost guidance. When rates fell after the financial crisis, the Seniors loaded up on debt and many companies overpaid for acquisitions that didn’t perform as promised. As a result, top managements of all the large gold producers lost their jobs. New managements have learned the hard lessons of the past and the industry has completely turned itself around by instilling the right incentive structure from the board to the mines. This is shown by recent financial and operating results and the strategies we have highlighted from the Gold Forum Americas.

Unfortunately, despite all of the improvements, the sector still suffered another de-rating in 2019 (trends C-D). We believe there are two reasons for this:

- Many generalist investors abandoned gold equities in the last cycle due to poor management. We have yet to see many of these investors return. So far in this cycle, most investors are using bullion ETFs for exposure to the gold market. Bullion ETF inflows have shattered records in 2020. Meanwhile net inflows to both active and passive equity funds have been anemic.

- There is a lack of growth amongst the large gold companies. Historically, a rising gold price brought exploration excitement, high quality discoveries and expanding production. While this excitement is still driving Junior gold miners, it is missing amongst the large companies. Multi-million ounce gold deposits have become very difficult to find and global production is probably past its peak. The large companies are now focused on maintaining current production levels in the long term.

So far in 2020 gold has advanced 24%, while the GDMNTR is up 34%. If Trend D remains in place through the current cycle, the GDMNTR may reach its historic 2011 high if/when gold reaches $2,755 per ounce. Generally speaking, from current levels, this would translate to a 46% increase for gold and a 70% increase for gold miners. We believe gold miners can do better.

Building Mass Appeal Over Building Mines

We believe, the key to achieving a positive re-rating, better performance and higher valuations is attracting generalists back to the sector. Scotia Capital Markets estimates that the average dividend yield of the large gold producers will rise to the average of the S&P 500 sometime in 2021 at 1.5%. Scotia also reckons that if gold prices become sustainable around the $2,000 per ounce level, cash flows should enable yields in the 3% to 4% range. Managements are focused on the task and doing everything in their power to make the gold industry appeal to a broader investor base with their ability to generate returns and mitigate risks.

GDMNTR and MVGDXJTR are dominated by Senior and Mid-Tier gold companies respectively, many of which we hold in our active gold funds. While the large companies are doing a great job, the fact remains that the best way to create value is to make a discovery and turn a barren piece of real estate into a gold mine. This is the type of value creation we find in the Juniors and some of the Mid-Tiers in our active portfolio. This is also how we expect to deliver the leverage to gold seen in past cycles.

Download Commentary PDF with Fund specific information and performance.

Originally published by VanEck, 10/9/20

IMPORTANT DISCLOSURES

*All company, sector, and sub-industry weightings as of September 30, 2020 unless otherwise noted. Source: VanEck, FactSet.

Nothing in this content should be considered a solicitation to buy or an offer to sell shares of any investment in any jurisdiction where the offer or solicitation would be unlawful under the securities laws of such jurisdiction, nor is it intended as investment, tax, financial, or legal advice. Investors should seek such professional advice for their particular situation and jurisdiction.

1U.S. Dollar Index (DXY) indicates the general international value of the U.S. dollar by averaging the exchange rates between the U.S. dollar and six major world currencies. 2S&P 500® is a capitalization-weighted index of 500 U.S. stocks from a broad range of industries. 3NYSE Arca Gold Miners Index (GDMNTR) is a modified market capitalization-weighted index comprised of publicly traded companies involved primarily in the mining for gold. 4MVIS Global Junior Gold Miners Index (MVGDXJTR) is a rules-based, modified market capitalization-weighted, float-adjusted index comprised of a global universe of publicly traded small- and medium-capitalization companies that generate at least 50% of their revenues from gold and/or silver mining, hold real property that has the potential to produce at least 50% of the company’s revenue from gold or silver mining when developed, or primarily invest in gold or silver. 5“Juniors” are gold mining companies that typically produce less than 0.3 million ounces of gold per year while Seniors” and “Mid-Tiers” are gold mining companies that produce, approximately,1.5-6.0 and 0.3-1.5 million ounces of gold per year, respectively. 6R-squared is a statistical measure generally interpreted as the extent to which the variance of one factor can explain the variance of a second factor (for example, the percentage of a fund or security’s movements that can be explained by movements in a benchmark index). 7Beta is a measure of sensitivity to market movements. 8A change in rating often occurs when the market’s view of a company or industry changes significantly enough—either positively or negatively—to where a company’s or industry’s valuation is impacted as a result.

Any indices listed are unmanaged indices and include the reinvestment of all dividends, but do not reflect the payment of transaction costs, advisory fees or expenses that are associated with an investment in a Fund. Certain indices may take into account withholding taxes. An index’s performance is not illustrative of a Fund’s performance. Indices are not securities in which investments can be made.

NYSE Arca Gold Miners Index is a service mark of ICE Data Indices, LLC or its affiliates (“ICE Data”) and has been licensed for use by VanEck Vectors ETF Trust (the “Trust”) in connection with VanEck Vectors Gold Miners ETF (the “Fund”). Neither the Trust nor the Fund is sponsored, endorsed, sold or promoted by ICE Data. ICE Data makes no representations or warranties regarding the Trust or the Fund or the ability of the NYSE Arca Gold Miners Index to track general stock market performance.

ICE DATA MAKES NO EXPRESS OR IMPLIED WARRANTIES, AND HEREBY EXPRESSLY DISCLAIMS ALL WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE WITH RESPECT TO THE NYSE ARCA GOLD MINERS INDEX OR ANY DATA INCLUDED THEREIN. IN NO EVENT SHALL ICE DATA HAVE ANY LIABILITY FOR ANY SPECIAL, PUNITIVE, INDIRECT, OR CONSEQUENTIAL DAMAGES (INCLUDING LOST PROFITS), EVEN IF NOTIFIED OF THE POSSIBILITY OF SUCH DAMAGES.

MVIS Global Junior Gold Miners Index (the “Index”) is the exclusive property of MV Index Solutions GmbH (a wholly owned subsidiary of Van Eck Associates Corporation), which has contracted with Solactive AG to maintain and calculate the Index. Solactive AG uses its best efforts to ensure that the Index is calculated correctly. Irrespective of its obligations towards MV Index Solutions GmbH, Solactive AG has no obligation to point out errors in the Index to third parties. The VanEck Vectors Junior Gold Miners ETF (the “Fund”) is not sponsored, endorsed, sold or promoted by MV Index Solutions GmbH and MV Index Solutions GmbH makes no representation regarding the advisability of investing in the Fund.

The S&P 500® Index is a product of S&P Dow Jones Indices LLC and/or its affiliates and has been licensed for use by Van Eck Associates Corporation. Copyright © 2018 S&P Dow Jones Indices LLC, a division of S&P Global, Inc., and/or its affiliates. All rights reserved. Redistribution or reproduction in whole or in part are prohibited without written permission of S&P Dow Jones Indices LLC. For more information on any of S&P Dow Jones Indices LLC’s indices please visit www.spdji.com. S&P® is a registered trademark of S&P Global and Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC. Neither S&P Dow Jones Indices LLC, Dow Jones Trademark Holdings LLC, their affiliates nor their third party licensors make any representation or warranty, express or implied, as to the ability of any index to accurately represent the asset class or market sector that it purports to represent and neither S&P Dow Jones Indices LLC, Dow Jones Trademark Holdings LLC, their affiliates nor their third party licensors shall have any liability for any errors, omissions, or interruptions of any index or the data included therein.

Please note that the information herein represents the opinion of the author, but not necessarily those of VanEck, and this opinion may change at any time and from time to time. Non-VanEck proprietary information contained herein has been obtained from sources believed to be reliable, but not guaranteed. Not intended to be a forecast of future events, a guarantee of future results or investment advice. Historical performance is not indicative of future results. Current data may differ from data quoted. Any graphs shown herein are for illustrative purposes only. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of VanEck.

About VanEck International Investors Gold Fund: You can lose money by investing in the Fund. Any investment in the Fund should be part of an overall investment program, not a complete program. The Fund is subject to the risks associated with concentrating its assets in the gold industry, which can be significantly affected by international economic, monetary and political developments. The Fund’s overall portfolio may decline in value due to developments specific to the gold industry. The Fund’s investments in foreign securities involve risks related to adverse political and economic developments unique to a country or a region, currency fluctuations or controls, and the possibility of arbitrary action by foreign governments, or political, economic or social instability. The Fund is subject to risks associated with investments in Canadian issuers, commodities and commodity-linked derivatives, commodities and commodity-linked derivatives tax, gold-mining industry, derivatives, emerging market securities, foreign currency transactions, foreign securities, other investment companies, management, market, non-diversification, operational, regulatory, small- and medium-capitalization companies and subsidiary risks.

About VanEck Vectors® Gold Miners ETF (GDX®) and VanEck Vectors® Junior Gold Miners ETF (GDXJ®): An investment in the Funds may be subject to risks which include, among others, investing in gold and silver mining companies, Canadian issuers, foreign securities, foreign currency, depositary receipts, small- and medium-capitalization companies, equity securities, market, operational, index tracking, authorized participant concentration, no guarantee of active trading market, trading issues, passive management risk, fund shares trading, premium/discount risk and liquidity of fund shares, non-diversified and concentration risks, all of which may adversely affect the Funds. Foreign investments are subject to risks, which include changes in economic and political conditions, foreign currency fluctuations, changes in foreign regulations, and changes in currency exchange rates which may negatively impact the Funds’ return. Small- and medium-capitalization companies may be subject to elevated risks. The Funds’ assets may be concentrated in a particular sector and may be subject to more risk than investments in a diverse group of sectors.

Diversification does not assure a profit or protect against loss.

Please call 800.826.2333 or visit vaneck.com for performance information current to the most recent month end and for a free prospectus and summary prospectus. An investor should consider a Fund’s investment objective, risks, charges and expenses carefully before investing. The prospectus and summary prospectus contain this as well as other information. Please read them carefully before investing.

© 2020 VanEck