By Natalia Gurushina, Chief Economist, Emerging Markets Fixed Income Strategy, VanEck Global

Resilient exports, manufacturing drive China’s recovery. Argentina’s debt restructuring deadline might be extended yet again.

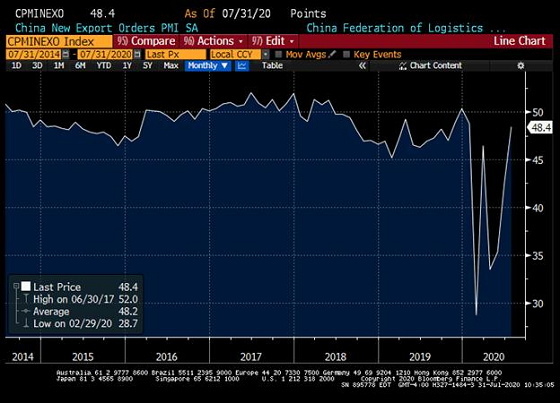

China’s official activity gauges (Purchasing Managers Indices, or PMIs) confirmed that the recovery gained pace in July. A notable development was a big jump in new export orders (see chart below), which suggests that global headwinds are subsiding. Supply-side factors (manufacturing, infrastructure) remained strong, and a combination of pent-up demand and further re-openings kept the services PMI well in expansion zone. The dichotomy between large companies PMI (firmly in expansion zone) and small firms PMI (slipped further to 48.6) persists, as the transmission mechanism is imperfect (=high financing costs for privately-owned firms) and authorities are wary of creating new bubbles (=“drip” stimulus only). Finally, even though July’s PMIs pointed to the improving external conditions, uncertainties—short-term and especially longer-term—are abound. So, the Politburo’s emphasis on domestic demand—both in terms of consumption and general self-sufficiency—should not come as a surprise.

According to local reports in Argentina, the debt restructuring deadline might be moved yet again from July 31 to August 27. Minister of Economy Martín Guzman confirmed yesterday that the government will still go through various restructuring options (and that it would seek a new agreement with the IMF irrespective of the restructuring deal). At this stage, the difference between the government and international creditors is not that big. There were strongly-worded statements in the past few days, but such brinksmanship is not uncommon. The extended deadline gives all sides time to reach a comprehensive deal, and move on.

South Africa’s trade surplus went into the stratosphere in June, beating expectations and giving yet another example of textbook external adjustment (Turkey might want to take notice). The improvement was driven to a large extent by weaker imports, as domestic demand remains constricted by COVID and the central bank refuses to intervene to support the currency. Exports contributed as well, getting an extra boost from precious metals. South Africa’s external adjustment is a welcome development, but the market is understandably concerned about the widening fiscal gap—and the next important milestone is October’s medium-term budget review.

Chart at a Glance: China New Export Orders – Finally On The Way Up?

Source: Bloomberg LP

IMPORTANT DEFINITIONS & DISCLOSURES

PMI – Purchasing Managers’ Index: economic indicators derived from monthly surveys of private sector companies; ISM – Institute for Supply Management PMI: ISM releases an index based on more than 400 purchasing and supply managers surveys; both in the manufacturing and non-manufacturing industries; CPI – Consumer Price Index: an index of the variation in prices paid by typical consumers for retail goods and other items; PPI – Producer Price Index: a family of indexes that measures the average change in selling prices received by domestic producers of goods and services over time; PCE inflation – Personal Consumption Expenditures Price Index: one measure of U.S. inflation, tracking the change in prices of goods and services purchased by consumers throughout the economy; MSCI – Morgan Stanley Capital International: an American provider of equity, fixed income, hedge fund stock market indexes, and equity portfolio analysis tools; VIX – CBOE Volatility Index: an index created by the Chicago Board Options Exchange (CBOE), which shows the market’s expectation of 30-day volatility. It is constructed using the implied volatilities on S&P 500 index options.; GBI-EM – JP Morgan’s Government Bond Index – Emerging Markets: comprehensive emerging market debt benchmarks that track local currency bonds issued by Emerging market governments.; EMBI – JP Morgan’s Emerging Market Bond Index: JP Morgan’s index of dollar-denominated sovereign bonds issued by a selection of emerging market countries; EMBIG – JP Morgan’s Emerging Market Bond Index Global: tracks total returns for traded external debt instruments in emerging markets.

The information presented does not involve the rendering of personalized investment, financial, legal, or tax advice. This is not an offer to buy or sell, or a solicitation of any offer to buy or sell any of the securities mentioned herein. Certain statements contained herein may constitute projections, forecasts and other forward looking statements, which do not reflect actual results. Certain information may be provided by third-party sources and, although believed to be reliable, it has not been independently verified and its accuracy or completeness cannot be guaranteed. Any opinions, projections, forecasts, and forward-looking statements presented herein are valid as the date of this communication and are subject to change.

Investing in international markets carries risks such as currency fluctuation, regulatory risks, economic and political instability. Emerging markets involve heightened risks related to the same factors as well as increased volatility, lower trading volume, and less liquidity. Emerging markets can have greater custodial and operational risks, and less developed legal and accounting systems than developed markets.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future performance.