By Natalia Gurushina

Chief Economist, Emerging Markets Fixed Income

China announced another supply-side stimulus package, as the consensus continues to cut the 2022 growth forecast.

China Growth Slowdown, Policy Response

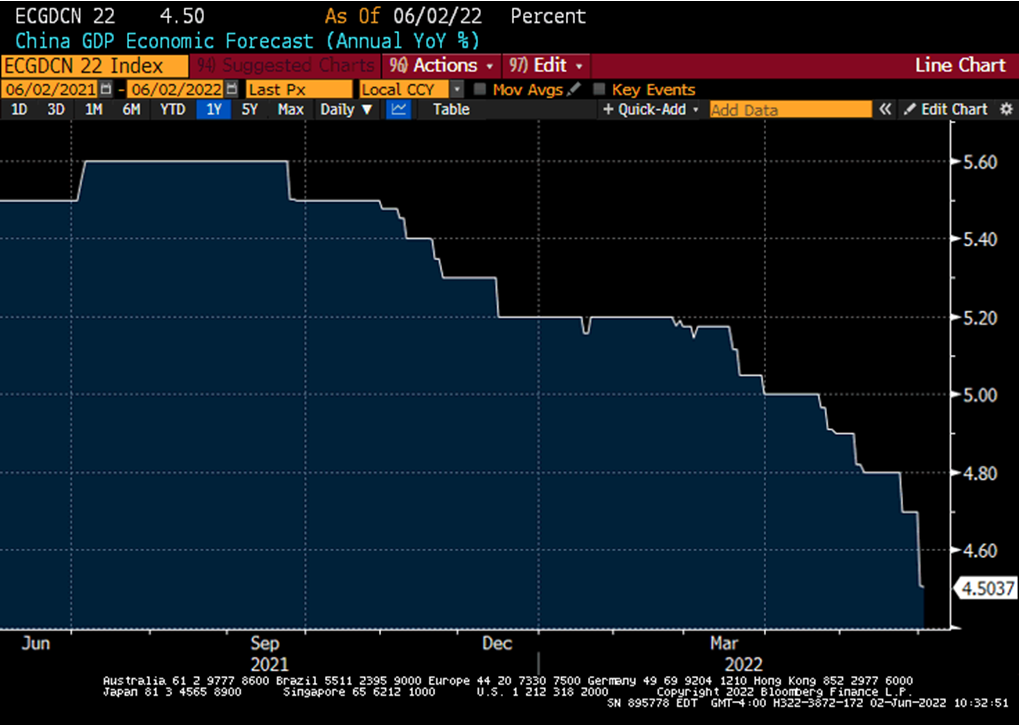

China’s policy stimulus is a newswire fixture these days – and the chart below shows why. China’s 2022 GDP forecast keeps moving farther and farther away from the official growth target, and the speed of downward growth revisions is accelerating despite some encouraging developments on the COVID front. So, is China’s USD120B increase in the credit quota for policy banks – announced yesterday – a game-changer or not? First of all, the package aims to support infrastructure investment – so it sounds like more of the same (= the demand side is still an “orphan”). Second, it is not huge size-wise – well below, for example, the loss of local government’s revenue from land sales estimated by sell-side analysts. So, what we have here is another supply-side “drip stimulus” measure. It will definitely help at the margin, but it remains to be seen whether its impact on GDP growth will not be offset by weak consumption.

New Eurozone Members

China is not the only independent global growth driver, which keeps investors on their toes. The Eurozone is often referred to as the world’s “weak link” due to the worsening growth outlook and a lack of political (and policy) cohesion. But, apparently, some “aspirants” still want to join the club. Croatia is now expected to enter the monetary union in January 2023, and the focus now shifts to the Croatian kuna/EUR conversion rate and potential rating upgrades. The accession also means that Croatia will be leaving the J.P. Morgan’s EM sovereign bond index (EMBIG), albeit its small weight (0.52%) means that the relative weights of other constituents will not change much.

Ukraine War And Policy Challenges

The final big policy move of the day is Ukraine’s humongous rate hike, which brought the policy rate from 10% to 25%. The size was definitely surprising, with the central bank pointing to rising inflation and larger FX interventions (the currency is currently fixed against the U.S. Dollar) as the main reasons for reactivating the policy tool in such a dramatic fashion. This is a strong signal for sure – but the problem is that international aid covers only a portion of Ukraine’s budget deficit, and the country continues to rely on monetary financing as Plan B (which boosts inflation). Stay tuned!

Chart at a Glance: China 2022 Growth Forecast Keeps Moving Away from the Target

Source: Bloomberg LP

Originally published by VanEck on June 2, 2022.

For more news, information, and strategy, visit the Beyond Basic Beta Channel.

PMI – Purchasing Managers’ Index: economic indicators derived from monthly surveys of private sector companies. A reading above 50 indicates expansion, and a reading below 50 indicates contraction; ISM – Institute for Supply Management PMI: ISM releases an index based on more than 400 purchasing and supply managers surveys; both in the manufacturing and non-manufacturing industries; CPI – Consumer Price Index: an index of the variation in prices paid by typical consumers for retail goods and other items; PPI – Producer Price Index: a family of indexes that measures the average change in selling prices received by domestic producers of goods and services over time; PCE inflation – Personal Consumption Expenditures Price Index: one measure of U.S. inflation, tracking the change in prices of goods and services purchased by consumers throughout the economy; MSCI – Morgan Stanley Capital International: an American provider of equity, fixed income, hedge fund stock market indexes, and equity portfolio analysis tools; VIX – CBOE Volatility Index: an index created by the Chicago Board Options Exchange (CBOE), which shows the market’s expectation of 30-day volatility. It is constructed using the implied volatilities on S&P 500 index options.; GBI-EM – JP Morgan’s Government Bond Index – Emerging Markets: comprehensive emerging market debt benchmarks that track local currency bonds issued by Emerging market governments; EMBI – JP Morgan’s Emerging Market Bond Index: JP Morgan’s index of dollar-denominated sovereign bonds issued by a selection of emerging market countries; EMBIG – JP Morgan’s Emerging Market Bond Index Global: tracks total returns for traded external debt instruments in emerging markets.

The information presented does not involve the rendering of personalized investment, financial, legal, or tax advice. This is not an offer to buy or sell, or a solicitation of any offer to buy or sell any of the securities mentioned herein. Certain statements contained herein may constitute projections, forecasts and other forward looking statements, which do not reflect actual results. Certain information may be provided by third-party sources and, although believed to be reliable, it has not been independently verified and its accuracy or completeness cannot be guaranteed. Any opinions, projections, forecasts, and forward-looking statements presented herein are valid as the date of this communication and are subject to change. The information herein represents the opinion of the author(s), but not necessarily those of VanEck.

Investing in international markets carries risks such as currency fluctuation, regulatory risks, economic and political instability. Emerging markets involve heightened risks related to the same factors as well as increased volatility, lower trading volume, and less liquidity. Emerging markets can have greater custodial and operational risks, and less developed legal and accounting systems than developed markets.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future performance.