By James Kim, VanEck Director, ETFs

For some time now, we have been studying different trading opportunities associated directly, or indirectly, with VanEck Vectors® ETFs. We have identified a number that we think may be of interest to our clients. Consequently, we have decided to launch a series of occasional pieces that offer investors what we believe may be interesting trading ideas around our ETFs.

With each new trade idea, we will also provide monthly updates on either how a previously executed trade (which is still “open”) is faring, or how previous trades (which have been executed and “closed”) have done. This will, we hope, provide investors some useful continuity around the trades we have described.

Trade Idea: A long position in VanEck Vectors® Fallen Angel High Yield Bond ETF (ANGL).

Rationale

At the end of July, the U.S. Federal Reserve (Fed) cut its overnight lending rate 25 bps from 2.25% to 2.00%. Despite some wild fluctuations, in the end, credit markets did not react that much to the Federal Open Market Committee’s (FOMC’s) cut. Investors in high yield bonds will, however, be congratulating themselves.

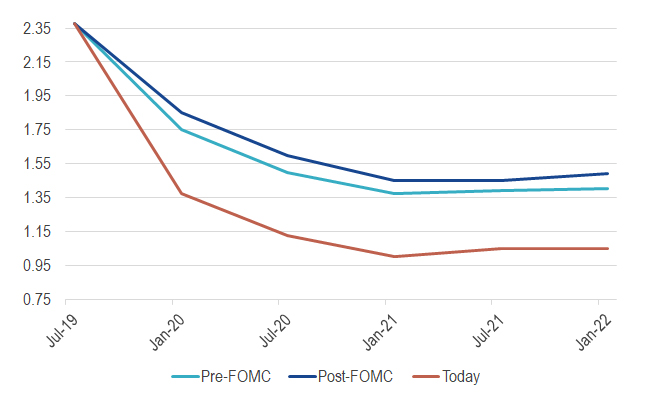

Based on the tone of the FOMC’s most recent statement, fed fund futures are pricing in 114 bps of additional cuts by the end of 2020—up from the 70 bps before the July FOMC meeting.

Federal Funds Rate Implied by Futures

Source: Source: Bloomberg and Goldman Sachs

We believe this is most likely only going to increase as trade tensions and the threat of a global slowdown persist. With President Donald Trump threatening to lift tariff rates “well beyond 25%” (if necessary), the U.S. Department of the Treasury designating China as a currency manipulator, China suspending purchases of U.S. agricultural goods and elsewhere the threat of a “no-deal” Brexit, the scene appears to be well set for a potential “mid-cycle adjustment” to “adjust policy to a somewhat more accommodative stance:” as per Fed Chairman Jerome Powell.

It does not look as if the Fed is interested in popping any asset bubbles in the riskier end of the market, in our opinion, rather, yields look to be heading back down to the lows reached in July. Even if they remain at these levels, 10-year U.S. Treasuries are yielding approximately 1.47% (as of August 28, 2019). We believe this may mean better returns from higher-yielding U.S. debt for the rest of the year.

Why specifically ANGL? As William Sokol alludes to in his recent post, “Fallen Angel High Yield Bonds in the Late Cycle,” two primary factors that have led to the outperformance of fallen angels over its broad market competitors.

- Longer Duration: As a general rule of thumb, for every 1% increase/decrease in interest rates, there should be a 1% decrease/increase in price (remember bond prices and interest rates are inversely related) for every one year in duration. In a falling interest rate environment, ANGL’s higher duration (6.215 based on aggregate cash flow (ACF) methodology[1]) should lead it to outperform relative to its broad high-yield peers. Fallen angel bonds generally have an average higher duration because of their previous status as an investment-grade issuer; because of their fundamentals, investment-grade issuers can generally obtain longer-term funding.

- Credit Selection: From the universe of high yield bonds, the higher quality names (i.e. BB) have outperformed the lower quality names (i.e. B, CCC and lower). ANGL’s tilt towards BB exposure (~75%) has helped outperform its peers in the broad high yield space since mid-May of this year.

Given this, there seem to be few reasons, in our opinion, why the performance of high yield bonds should not surpass that of either leveraged loans or, indeed, investment-grade debt in the second half of the year. While high yield bonds may have lost out to equities in the first half of the year, weak earnings could now be a drag on equity returns. We believe that, with few signs of rising defaults, the returns from high yield should remain solid for some time yet.

The VanEck Vectors®Fallen Angel High Yield Bond ETF (ANGL) seeks to replicate as closely as possible, before fees and expenses, the price and yield performance of the ICE BofAML US Fallen Angel High Yield Index (H0FA), which is comprised of below investment grade corporate bonds denominated in U.S. dollars, issued in the U.S. domestic market and that were rated investment grade at the time of issuance.

For more market trends, visit ETF Trends.

IMPORTANT DISCLOSURES