By Doug Sandler, CFA, RiverFront Investment Group

SUMMARY

- Significant supply shortages are beginning to appear.

- Some of these shortages can be addressed quickly and some will take time.

- We are equity ‘bulls’ but will not be surprised if markets are choppy over the summer.

It Could be a Choppy Summer for Markets

As the economy reopens the economic tailwinds are picking up. After nearly 16 months of an economic shut-down, the combination of high savings and government stimulus has created pent-up demand to consume.

Undoubtedly, we believe better economic times are coming.

Buying into the stock market in anticipation of the economy re-opening seems like a ‘no-brainer’ to us. RiverFront’s investment team recognizes the extent to which stocks have anticipated this recovery. We understand that things rarely happen as smoothly and quickly as people think. High levels of investor optimism suggest that the stock market may be vulnerable to disappointment in the short-term. This explains our recent risk reduction trade that brought our balanced portfolios closer to benchmarks.

There is no perfect recovery and bumps along the road should be expected. So, what could go wrong? For the first time in a while, the biggest threat to future growth may not be a lack of demand but rather constraints on supply.

Supply constraints are beginning to appear in multiple areas and we believe their impact may be underestimated. Below, we focus on constraints around labor supply and manufacturing and services capacity:

- Labor supply starting to be addressed: We see April’s non-farm payroll miss, the biggest since 1998, as a high-profile example of pending supply shortages. It would appear that more generous enhanced unemployment benefits have ‘crowded out’ low-wage private sector jobs. Employers are countering with higher wages and signing bonuses, but ‘Help Wanted’ signs are becoming more prevalent. A reduction in unemployment benefits appears to be the next step to alleviating labor constraints. Whether these reductions come soon enough, and whether there will be long-term consequences of nearly 12 months of generous unemployment benefits, remain in question. Solutions to the labor shortage are now being addressed. For example, President Joe Biden on May 10th, stated: “We’re going to make it clear that anyone collecting unemployment, who was offered a suitable job, must take the job or lose their unemployment benefits”. Additionally, at least 22 states have gone one step further by choosing to end their participation in the federal enhanced unemployment benefit program in June, roughly three months early.

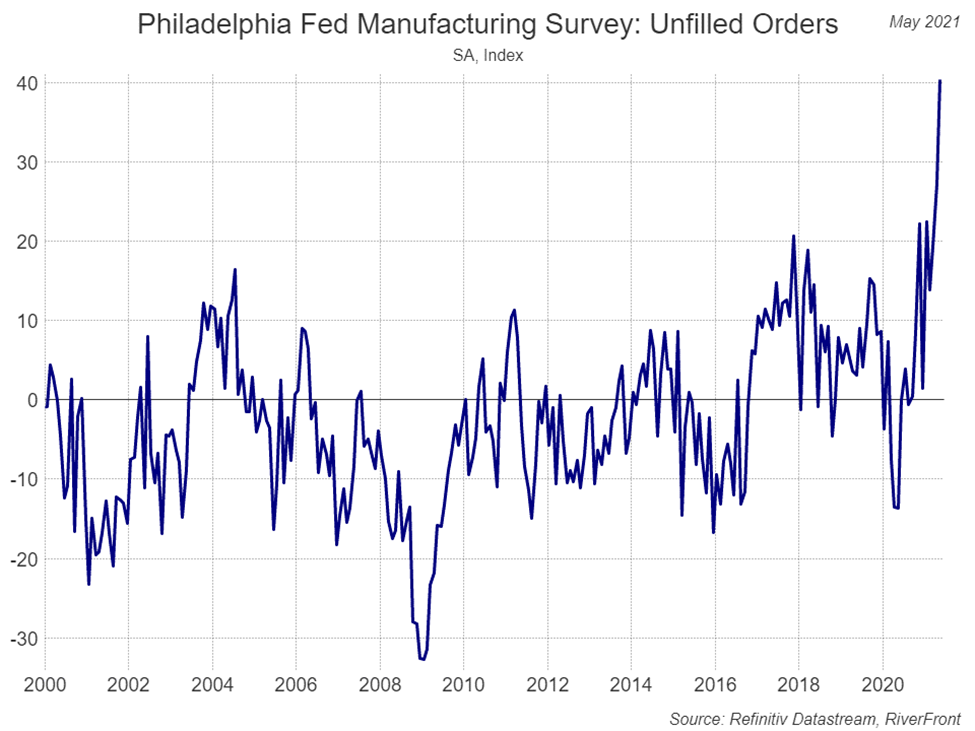

- Increasing manufacturing capacity faces short-term roadblocks: It has been a while since the US economy has experienced a demand surge the likes of which we are seeing today. Not surprisingly, suppliers, many of whom utilize ‘just-in-time’ inventory systems, have been caught flat-footed. This fact is apparent in the spike in ‘unfilled orders’ in April’s Philadelphia Fed Manufacturing report (Chart below). ‘Ginning up’ production is not simple and can require significant lead-times. Consider how long it took manufacturers to meet the spike in demand for toilet paper, masks, and cleaning supplies over the last twelve months, and these were relatively simple products to produce. Inventory shortages in automobiles (the worst in at least a decade), homes (lowest in history), semiconductors, and raw materials like lumber and copper will not be simple or quick to eradicate. The building of large sawmills, copper mines, semiconductor fabrication facilities, and auto plants can take years and that is before considering the added complexities of environmental permitting and grass-roots activism from the NIMBY (not in my backyard) crowd. Shortage issues are also being compounded by port congestion (Record volumes at the 3 biggest ports in the US: Los Angeles, Long Beach, and New York/New Jersey), outstanding trade restrictions, lingering COVID-19 shutdowns and a sideways ship that closed the Suez Canal for six days.

Disclosures: Past performance is no guarantee of future results. Shown for illustrative purposes. Not indicative of RiverFront portfolio performance.

- Increasing service capacity may take longer: Service-sector workers – like waitstaff, entertainers, and janitors – have been the most impacted by COVID-19. Luring them back to work is proving more difficult than their former employers believed. These workers seem destined to be going from the most underappreciated employees in the workplace to some of the most valuable. Higher wages, signing bonuses, paid time off, and other benefits are just a few of the examples of the shifting attitudes towards our service sector workers. Unfortunately, we find it unlikely that all the hotels, restaurants, bars, spas, and theme parks will be able to staff up quickly enough to meet the coming demand surge.

Short-Term Implications:

- Supply likely to remain tight: Unfortunately, we believe ‘out of stock’ signs and bidding wars will likely remain over the next few quarters, placing a real constraint on economic growth and the potential for disappointing optimistic expectations. The impact of supply shortages is real. The Gross Domestic Product (GDP) report for the first quarter noted that the US economy grew by 6.4%, the second fastest quarterly rate since 2003. However, inventory drawdowns held this number back by nearly 3 percentage points! If you have tried to buy a bicycle, washing machine, or a house in the last 6-months you have likely experienced the impact of supply shortages personally.

- FOMO may compound tight supply: When supply tightens, the ‘FOMO’ (fear of missing out) gene kicks in and consumers stockpile, further compounding the problem. The empty shelves in many grocery stores a year ago are reminders of this. Outages are not limited to goods alone; services may be less available as companies are forced to align capacity with worker availability.

- Higher prices: Economics 101 tells us that prices should ultimately bring supply and demand into balance. Too little supply = higher prices. April’s consumer price index and producer price index reports, both of which were widely expected to be higher than last year’s pandemic low, also rose month-on-month surprising forecasters.

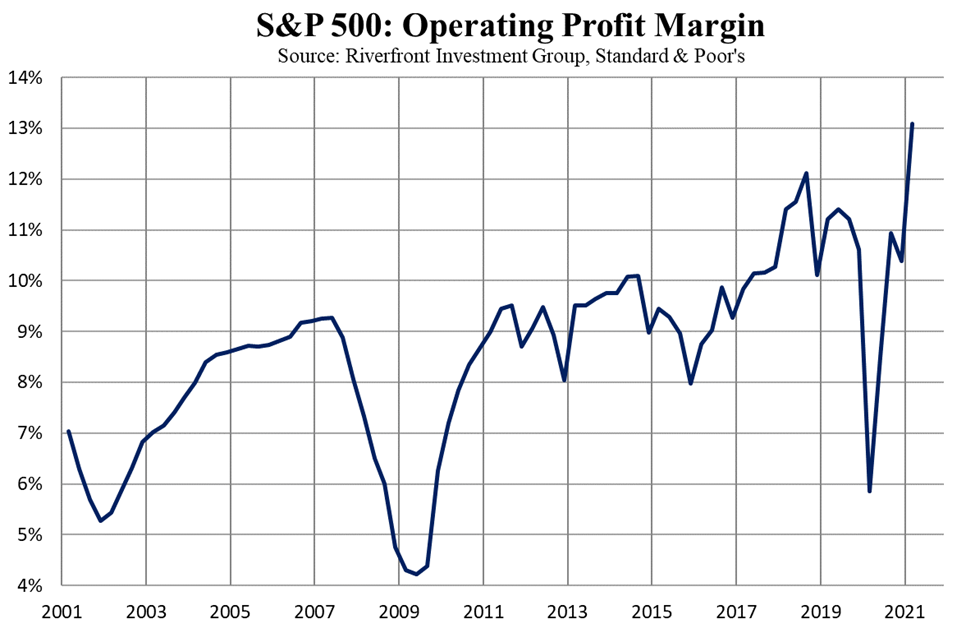

- Challenges for companies: You can’t sell what you don’t have, and rosy revenue expectations may need to be dialed back to reflect lower volumes. Emergency measures taken to meet demand, such as ‘paying up’ for raw materials, switching vendors or using faster but more expensive transportation methods will also eat into corporate profits. Companies will face the choice between passing on their higher input costs to their customers or accepting lower profit margins. If they chose the latter, analysts’ expectations for all-time record profit margins (see chart below) may need to be tempered.

Disclosures: Past performance is no guarantee of future results. Shown for illustrative purposes. Not indicative of RiverFront portfolio performance. Index definitions are available in the disclosures.

Conclusion: We believe that a combination of American ingenuity and a lowering of investor expectations will prevail, and the bull market will remain intact. To get there it may take a quarter or two of lower-than-average equity returns. Our portfolios remain slightly overweight stocks relative to bonds, consistent with our positive long-term outlook.

Important Disclosure Information

The comments above refer generally to financial markets and not RiverFront portfolios or any related performance. Opinions expressed are current as of the date shown and are subject to change. Past performance is not indicative of future results and diversification does not ensure a profit or protect against loss. All investments carry some level of risk, including loss of principal. An investment cannot be made directly in an index.

Chartered Financial Analyst is a professional designation given by the CFA Institute (formerly AIMR) that measures the competence and integrity of financial analysts. Candidates are required to pass three levels of exams covering areas such as accounting, economics, ethics, money management and security analysis. Four years of investment/financial career experience are required before one can become a CFA charterholder. Enrollees in the program must hold a bachelor’s degree.

Information or data shown or used in this material was received from sources believed to be reliable, but accuracy is not guaranteed.

This report does not provide recipients with information or advice that is sufficient on which to base an investment decision. This report does not take into account the specific investment objectives, financial situation or need of any particular client and may not be suitable for all types of investors. Recipients should consider the contents of this report as a single factor in making an investment decision. Additional fundamental and other analyses would be required to make an investment decision about any individual security identified in this report.

In a rising interest rate environment, the value of fixed-income securities generally declines.

When referring to being “overweight” or “underweight” relative to a market or asset class, RiverFront is referring to our current portfolios’ weightings compared to the composite benchmarks for each portfolio. Asset class weighting discussion refers to our Advantage portfolios. For more information on our other portfolios, please visit www.riverfrontig.com or contact your Financial Advisor.

Stocks represent partial ownership of a corporation. If the corporation does well, its value increases, and investors share in the appreciation. However, if it goes bankrupt, or performs poorly, investors can lose their entire initial investment (i.e., the stock price can go to zero). Bonds represent a loan made by an investor to a corporation or government. As such, the investor gets a guaranteed interest rate for a specific period of time and expects to get their original investment back at the end of that time period, along with the interest earned. Investment risk is repayment of the principal (amount invested). In the event of a bankruptcy or other corporate disruption, bonds are senior to stocks. Investors should be aware of these differences prior to investing.

Index Definitions:

Standard & Poor’s (S&P) 500 Index TR USD (Large Cap) measures the performance of 500 large cap stocks, which together represent about 80% of the total US equities market.

RiverFront Investment Group, LLC (“RiverFront”), is a registered investment adviser with the Securities and Exchange Commission. Registration as an investment adviser does not imply any level of skill or expertise. Any discussion of specific securities is provided for informational purposes only and should not be deemed as investment advice or a recommendation to buy or sell any individual security mentioned. RiverFront is affiliated with Robert W. Baird & Co. Incorporated (“Baird”), member FINRA/SIPC, from its minority ownership interest in RiverFront. RiverFront is owned primarily by its employees through RiverFront Investment Holding Group, LLC, the holding company for RiverFront. Baird Financial Corporation (BFC) is a minority owner of RiverFront Investment Holding Group, LLC and therefore an indirect owner of RiverFront. BFC is the parent company of Robert W. Baird & Co. Incorporated, a registered broker/dealer and investment adviser.

To review other risks and more information about RiverFront, please visit the website at www.riverfrontig.com and the Form ADV, Part 2A. Copyright ©2021 RiverFront Investment Group. All Rights Reserved. ID 1660502