By Frank Holmes, CEO and Chief Investments Officer for U.S. Global Investors

Bernard Looney, BP’s new chief executive, wants to cut his company’s greenhouse gas emissions down to zero by 2050. To do that, the world’s sixth-largest energy company is committing itself to massive investment in renewable energy, including wind, solar and biofuels.

“We aim to invest more and more in low-carbon businesses over time, and less and less in oil and gas,” commented Looney. BP’s decision to shift gears, he added, was driven not just by government policies that favor lower emissions but also demand from customers, investors and members of his own staff.

The U.K.-based energy provider may be more aggressive than its peers when it comes to plotting a carbon-free future, but it’s certainly not alone. Royal Dutch Shell, Total, Equinor and other traditional fossil fuel producers have also recently been diverting significant amounts of capital to renewable energy.

And it’s not just energy companies. Teck Resources, the giant Vancouver-based miner of copper, coal and zinc, announced in early February that it too has plans to be carbon-neutral by 2050.

“Providing the world with clean, reliable, affordable energy,” Looney said, “will require nothing less than reimagining energy.”

Adjusting Our Investment Strategy for a Changing World

Similarly, it may also require reimagining what it means to invest in energy and natural resources. And that’s precisely what we’ve been doing at U.S. Global Investors, particularly when it comes to our Global Resources Fund (PSPFX).

Although we’re not ready to toss out fossil fuel and carbon emitting companies altogether, we have been increasing the fund’s exposure to clean renewable energy. About 18 percent of the fund is now devoted to companies that are involved in either manufacturing wind turbines or solar panels (Vestas Wind Systems, for example, the world’s number one supplier of wind turbines) or generating and retailing electricity that’s been sourced through renewable means (Australia’s AGL Energy, whose energy mix includes not just wind and solar but also thermal and hydroelectric).

Copper will continue to play an important role in the gradual shift to renewables. In some cases, wind turbines and solar facilities can use as much as 12 times more of the red metal than traditional energy systems, according to the Copper Development Association (CDA). As such, we have maintained positions in key copper producers, including Ivanhoe Mines, Anglo American and BHP, whose stock may benefit from higher copper prices.

Facing Facts

You might think that the only reason we’re seeing a surge in renewables is because of government policy. While there’s some truth to this, it’s not entirely accurate. More and more, people are demanding cleaner, more sustainable energy. A November survey conducted by the Pew Research Center found that a whopping 77 percent of Americans believe that developing “alternative energy” is a more important priority right now than producing more fossil fuels.

Even if you’re not personally sold on the idea of sustainability and “green energy,” you must acknowledge that this is the direction the world is headed in. Rather than fight it, we’ve made the decision to follow the money.

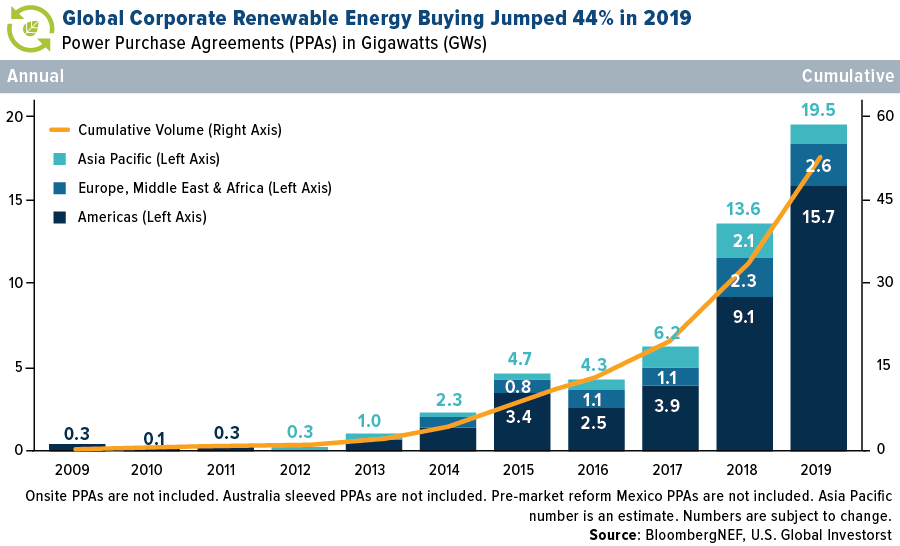

Just look at the facts. Last year, corporations around the world bought a record amount of clean energy through power purchase agreements (PPAs). According to BloombergNEF, as many as 100 companies in 23 different countries signed clean energy contracts amounting to 19.5 gigawatts (GW) of power, a 44 percent increase from 2018. Since 2009, a cumulative 52.9 GW have been purchased.

Among the biggest buyers in 2019 were American tech firms, including Google, Facebook and Amazon. A number of traditional oil and gas companies also signed contracts. Houston-based Occidental Petroleum, for instance, now powers its oil operations in the Permian Basin using solar energy.

In Europe, which is undergoing a rapid transition to clean energy, renewables accounted for an incredible 34.6 percent of total electricity generation in 2019. Today a greater share of European households and businesses get their power from wind and solar than they do coal.

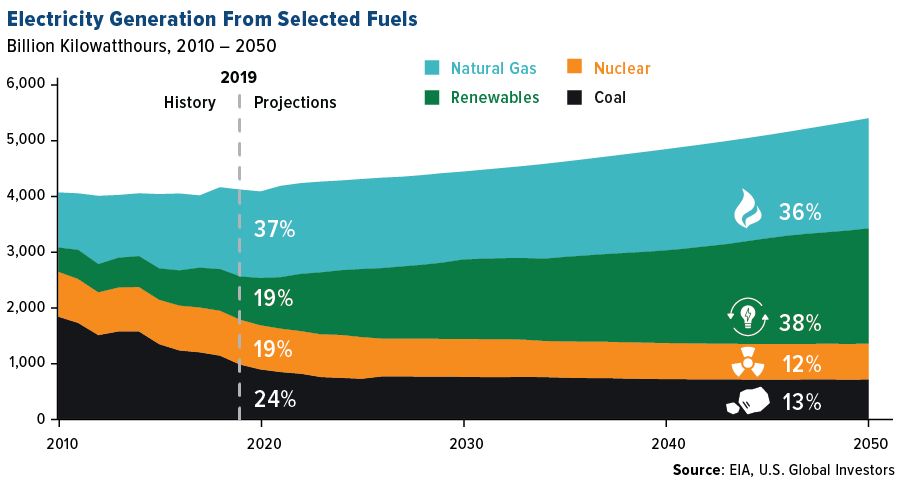

The U.S. isn’t too far behind. In its latest long-term projection, the U.S. Energy Information Administration (EIA) expects electricity generation from renewable sources to surpass nuclear and coal by as early as next year. By 2045, it may even surpass natural gas.

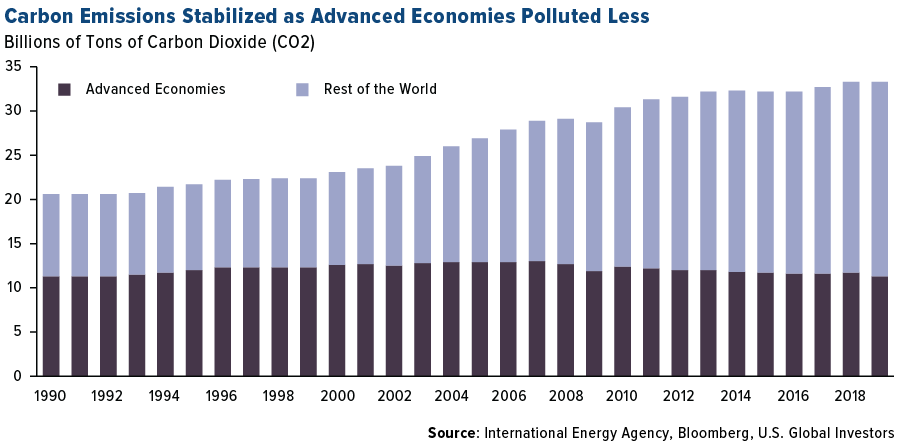

Thanks to these efforts, energy-related carbon emissions in advanced economies have remarkably dropped to levels last seen in 1993, according to the International Energy Agency (IEA). This helped total world emissions stabilize in 2019 for the first time in three years, even as developing economies, led by China and India, have been polluting more.

The Last Straw

China isn’t resting on its laurels, however. Not only has the Asian giant been a leader in clean energy investment, but it’s also recently joined a number of other countries in announcing a ban on single-use plastic items, starting with bags. The world’s largest producer and consumer of plastic, China will ban non-degradable plastic bags in major cities by the end of this year and everywhere else by 2022.

By 2025, non-degradable, single-use plastic packaging of all kinds will be forbidden in the country.

Other countries—as many as 60, in fact—have passed similar legislation. Among the most aggressive is the law approved by the European Parliament in October 2018 that bans 10 common types of plastics, including straws, plates, cutlery and cotton-swab sticks. Canada plans to ban all single-use plastic items by the end of 2021.

The reason I bring this up is because it represents a major headwind for oil and gas companies that manufacture the petrochemicals needed to make plastic products. Those that cannot adapt to changing policy and consumer habits will likely continue to face significant divestiture in favor of paper packaging companies and suppliers such as International Paper, Canfor Pulp Products and more.

If You Can’t Beat Them…

Speaking of divestiture, every day, it seems, you hear of another institutional investor that’s getting out of fossil fuels. Norway’s Government Pension Fund—the world’s largest sovereign wealth fund at over $1 trillion in assets—made headlines last year when it announced it would divest from oil and gas companies. What made this particularly notable is that the Fund was set up in 1990 specifically to invest in Norway’s prolific oilfields.

College endowments have followed suit, with Georgetown University and the University of California among the biggest to divest. Harvard and the Massachusetts Institute of Technology (MIT) are under considerable pressure from students, faculty and alumni to sell all shares of fossil fuel companies.

In January, BlackRock, the world’s largest fund manager, said it would begin shifting out of fossil fuels, and I wouldn’t be surprised if similar announcements from Vanguard and State Street Global Advisors were forthcoming.

To be clear, we’re not at the moment considering such drastic moves. It must be said, though, that with so much capital being transferred out of traditional oil and gas companies and into renewables, there may come a day when it no longer makes sense to fight the mob.

And the mob is clearly telling us which way the wind is blowing. Take a look at the chart above. Clean energy stocks have completely decoupled from natural resources, returning more than 66 percent for the three-year period through February 18. Natural resources stocks, meanwhile, returned only 11 percent over the same time.

If you can’t beat them, sometimes it may be better to join them.

Please consider carefully a fund’s investment objectives, risks, charges and expenses. For this and other important information, obtain a fund prospectus by visiting www.usfunds.com or by calling 1-800-US-FUNDS (1-800-873-8637). Read it carefully before investing. Foreside Fund Services, LLC, Distributor. U.S. Global Investors is the investment adviser.

Foreign and emerging market investing involves special risks such as currency fluctuation and less public disclosure, as well as economic and political risk. Because the Global Resources Fund concentrates its investments in specific industries, the fund may be subject to greater risks and fluctuations than a portfolio representing a broader range of industries.

The S&P Global Clean Energy Index provides liquid and tradable exposure to 30 companies from around the world that are involved in clean energy related businesses. The index comprises a diversified mix of clean energy production and clean energy equipment & technology companies. The S&P Global Natural Resources Index includes 90 of the largest publicly-traded companies in natural resources and commodities businesses that meet specific investability requirements, offering investors diversified and investable equity exposure across 3 primary commodity-related sectors: agribusiness, energy, and metals & mining.

Fund portfolios are actively managed, and holdings may change daily. Holdings are reported as of the most recent quarter-end. Holdings in the Global Resources Fund as a percentage of net assets as of 12/31/2019: BP plc 0.00%, Royal Dutch Shell PLC 1.06%, Total S.A. 0.00%, Equinor ASA 0.89%, Teck Resources Ltd 0.78%, Vestas Wind Systems A/S 1.81%, AGL Energy Ltd 1.03%, Ivanhoe Mines Ltd 3.23%, Anglo American PLC 1.29%, BHP Group Ltd 0.98%, Alphabet Inc. 0.00%, Facebook Inc. 0.00%, Amazon.com Inc. 0.00%, Occidental Petroleum Corp. 0.44%, International Paper Co. 0.54%, Canfor Pulp Products Inc. 0.52%.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.