Based on the latest report on exchange-traded fund (ETF) flow data from State Street Global Advisors, smart beta ETF inflows maintained their $4 billion in inflows during the month of June as the capital markets recovered from a volatility-laden May.

“Smart beta flows continued their 2019 trend of averaging $4 billion of inflows a month,” wrote Matthew Bartolini, CFA Head of SPDR Americas Research State Street Global Advisors, in the report. “Like previous periods, the majority of the flows have gone to defensive-oriented factor exposures, such as Dividend Yield and Minimum Volatility. ESG strategies have taken in the most flows out of a percent of assets within this category, largely from two specific funds that received strategic cornerstone investments at launch.Outside of those flows,there has been little interest relative to Smart Beta and Active mandates.”

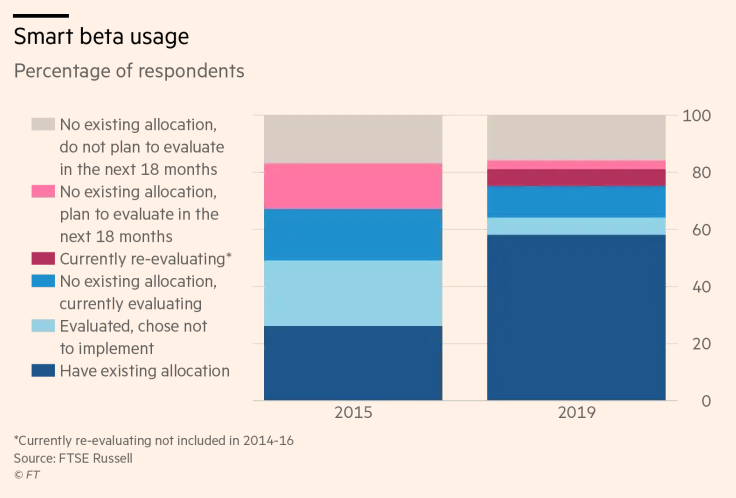

The previous reminded investors that they need to be strategic when it comes to investing in 2019 as volatility took hold of the capital markets as the U.S.-China trade deal that was supposed to happen morphed into an impasse. That said, more investors are beginning to realize the importance of incorporating smart beta strategies into their portfolios according to a survey conducted by index and analytics provider FTSE Russell.

58 percent of investors have an allocation to smart beta, based on the survey of 178 asset owners. It’s more than double the amount in 2015 when the same survey yielded only a 26 percent usage by investors.

With smart beta usage on the rise, one of the challenging aspects advisors face with this more cautious investor is the plethora of options available, especially in the exchange-traded fund (ETF) space. Where are the opportunities in ETFs given the current market landscape and how can smart beta-factor strategies work in a portfolio?

A market-capitalization-weighted index provides clients with exposure to a particular market based on security prices, without considering any true company fundamental to judge its value. However, the Great Recession of 2008 roiled investors with deep declines that they were not anticipating, as a result of overexposure to potentially overpriced stocks relative to their true value.

As such, things began to change, with many financial advisors shifting to smart beta strategies in the past 10 years. The first aspect to touch upon was the limitations of a market cap weighted index, which would then warrant the need for smart beta and factor strategies.

Given certain market conditions, investors need more than just a passive index that goes beyond a one-size-fits-all template that uses market cap weighting. While these indexes provided simple, low-cost solutions, the need for even greater scrutiny is necessary in the quest for more alpha —a case for smart beta.

Through smart beta, investors get adaptable exposure with the rules-based approach in conjunction with reaping the rewards of diversification via access to a broad market index. In addition, the simplicity of buying a broad-based market index has a concentration of risk, and should a market correction ensue comparable to that witnessed in the fourth quarter, investors are left vulnerable.

As such, smart beta strategies can be segmented into alternatively weighted, single factor and multi factor strategies–the latter to diversify concentration in a specific factor–low or minimum volatility, momentum, size, quality, yield, and value.

Smart beta ETFs to consider:

- Natixis Seeyond International Minimum Volatility ETF (NYSEArca: MVIN)

- VictoryShares US 500 Volatility Wtd ETF (NASDAQ: CFA)

- Oppenheimer Russell 1000 Dynamic Multifactor ETF (Cboe: OMFL)

For more market trends, visit ETF Trends.