Myth 1: ETFs are detrimental to markets – What impact has the precipitous rise in ETF AUM, and trading, had on underlying markets?

To address this question we consider liquidity, volatility and correlations that we can observe in the market. The meteoric rise in ETF AUM has led many investors to fear that ETF asset flows and trading activity may interfere with the liquidity of their underlying market, especially during periods of market stress. To address this concern, and to provide an instructive example, we took a look at the U.S. high yield bond market and broke down trading activity into three categories: underlying market activity, primary market activity and secondary market activity. In the context of ETFs, underlying market activity refers to direct trading of single name bonds, primary market activity refers to creation and redemption activity of high yield ETFs, and secondary market activity refers to the trading of outstanding ETF shares between market participants. The data illustrates the scope of high yield bond ETF trading relative to the broader market.

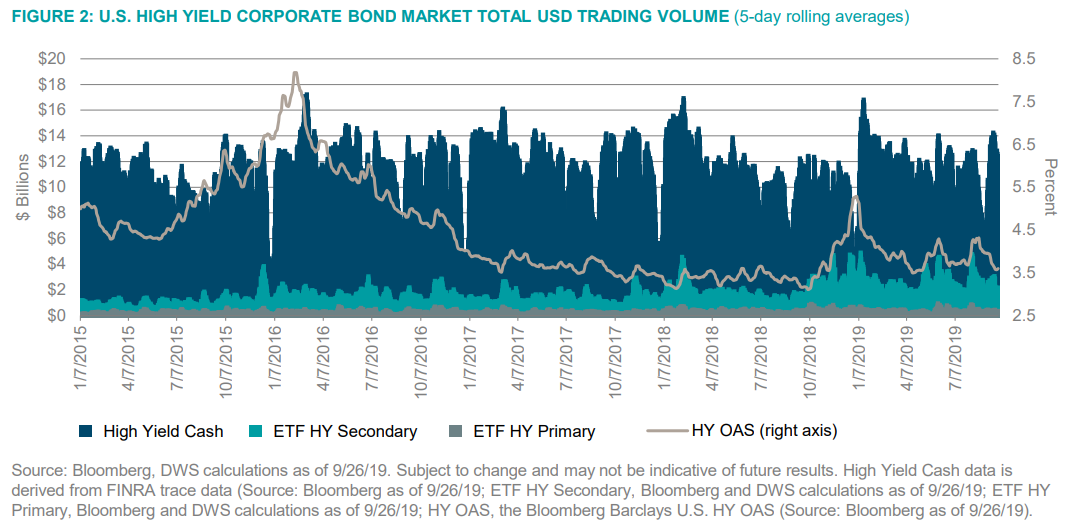

As shown in Figure 2, the portion of trading activity by U.S. high yield bond ETFs in the primary market (i.e. the creation and redemption orders of ETFs that impact individual bonds, represented by the gray area on the chart) is very small relative to the total dollar amount of cash high yield trading (i.e. the total dollar amount of bonds that change hands in a given day) that occurs. In fact, over the period shown, daily primary ETF trading activity, on average, represented less than 3% of daily high yield cash trading— a low percentage that speaks to the limited impact that ETFs have on underlying securities.

In addition, the turquoise shaded area indicates the total dollar amount of ETF shares that traded hands, and this highlights the additional level of liquidity that ETFs have introduced to the market. Importantly, such liquidity can be viewed as additive to the liquidity found in the high yield market. This is so, because trading in ETFs enables cash investors to turn on or turn off high yield bond exposure without buying or selling underlying bonds directly in the underlying cash market. This is an extraordinary feature of ETFs: They trade on the secondary market without impacting individual underlying securities, thus enhancing the overall liquidity profile of the market. This point is key.

Turning to volatility, ETF skeptics may argue that ETFs create a mechanism by which huge swathes of assets can be traded at the push of a button, which could have the unintended side effect of increasing market volatility.

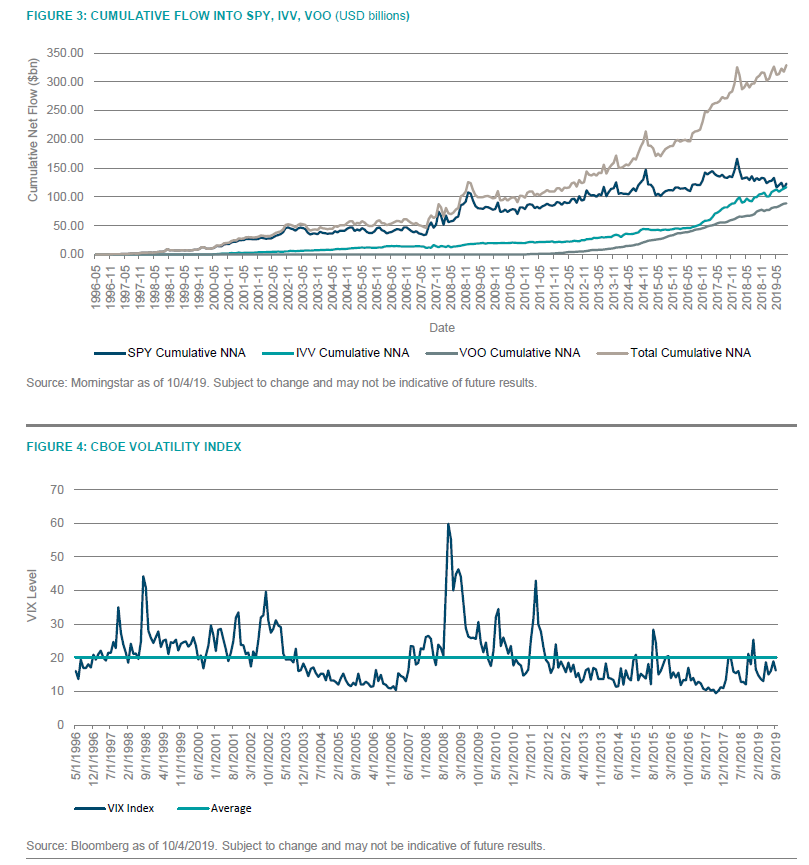

However, when discussing volatility in the context of ETFs, it is important to point out that definitively knowing what the volatility of markets that currently have ETF exposure would have been without the presence of ETFs is impossible, since one cannot directly observe how markets would have behaved otherwise, without the presence of ETFs. Take the S&P 500 index for example. In the following exercise we aim to get a sense for how the S&P 500 behaved alongside large inflows over time into ETFs that track this popular benchmark. Consider three of the largest and most popular S&P 500 ETFs in the U.S. market: SPY, IVV, VOO.

Figures 3 and 4 show the cumulative net dollar inflow into these ETFs, and the VIX Index, a gauge of S&P 500 volatility, over the same time period.

As you can see, there appears to be no immediately noticeable trend in S&P 500 volatility that coincides with the massive growth in assets of S&P 500 Index ETFs. Although the total AUM of these ETFs is still small relative to the market cap of the S&P 500 (i.e. comparing around $0.4 Trillion in these S&P 500 ETFs to close to $30 trillion for the S&P 500 Index market cap) they still represent a sizeable portion of the S&P 500 at current levels. Ultimately, while this is not definitive proof, it provides evidence in support of the fact that as ETF AUM rises, it does not necessarily change the volatility profile of the market that underlies those particular ETFs.

In terms of correlation, market participants may worry that as ETFs increase in market representation, correlations between underlying securities within the respective indices could increase and therefore elevate risk within the market.

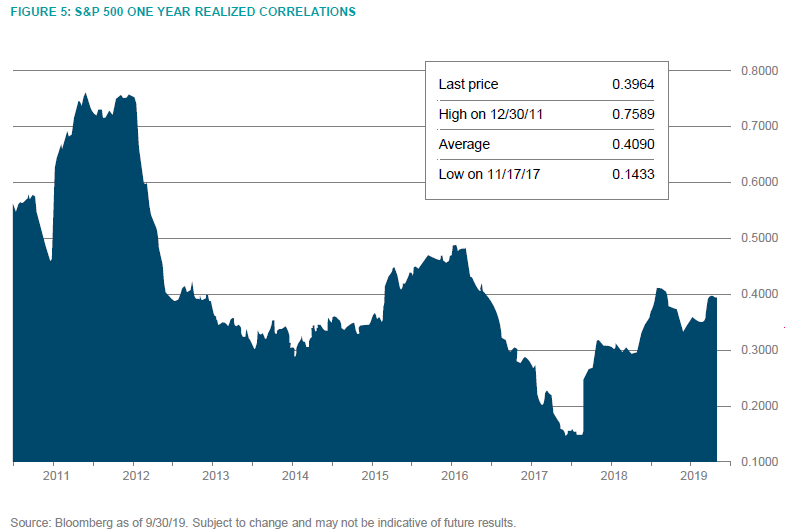

Proponents of this argument propose that when passive funds buy or sell baskets of stocks all at once, it could cause stock prices to move simultaneously more so than they otherwise would have, thus increasing inter-stock correlations. However, the graph below shows the average realized one-year correlation of S&P 500 stocks over the last nine years, a time period over which US ETFs assets nearly quadrupled from around $1 trillion USD to around $4 trillion USD. It seems that there is no noticeable trend that indicates that correlations have been rising over this time period coinciding with a massive rise in ETF AUM. In fact, inter-stock correlations between S&P 500 members seemed to have trended downward over the period. Had the opposite been true, in other words, if average correlations between individual S&P 500 stocks had been on the rise over the period, this would still only potentially indicate that ETFs could have been the culprit, since observing a correlation between two trends does not necessarily imply causation.

To download the full whitepaper, The ETF Ecosystem: Myths vs Reality, click here.