By Jason Chen, DWS.com

When deciding whether or not to hedge the currency risk on international equity exposures, investors often put their expectations of the directionality of the U.S. dollar and non-dollar currencies front and center. The reality is, however, that long run returns on many of these currencies (see The Euro – for he’s not a jolly good fellow) against the dollar have historically been underwhelming, and always articulating strong views on the directionality of the level of spot currencies can be challenging at times.

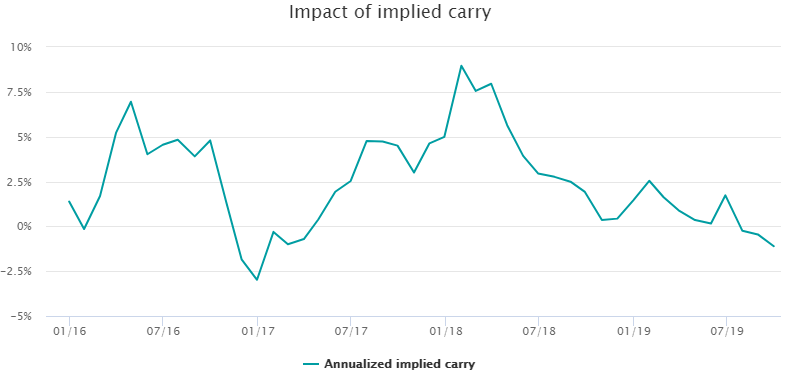

While we’ve explored extensively the importance of risk, or volatility, in making determinations about currency hedging, we haven’t highlighted the importance of the currency carry story in recent years. Currency carry represents the differential in 1-month currency forward exchange rates relative to spot currency rates, which investors monetize when they implement carry hedges on international exposures. In effect, by purchasing a currency forward contract on top of their equity exposure, an investor or ETF is seeking to negate most of the explicit exposure to currency risk, with the byproduct of incurring a cost or benefit tied to this forward.

Since the Federal Reserve Bank began hiking interest rates in 2015, and as other developed market central banks have continued with broadly dovish monetary policy, interest rates have diverged, with U.S. rates measurably higher than international rates. This short term interest rate differential, combined with persistent demand for U.S. dollar borrowing, has resulted in carry having been the determining factor in the relative performance of MSCI EAFE U.S. Dollar Hedged Index vs. the MSCI EAFE Index. Higher U.S. rates have meant that U.S. investors have received a benefit tied to hedging currency risk that accompanies investing in other, lower interest rate, developed markets.

Examining a specific window of time in which the spot returns on the currencies underlying the MSCI EAFE Index were effectively flat, we can demonstrate the importance to investors’ total return experience of currency carry. From November 2015 to September 2019, the MSCI EAFE Currency Index, on a spot basis, was down -1.11%.

Source: DWS calculations, Bloomberg, MSCI as of 9/30/2019. Currency performance represented by the Index returns assume reinvestment of all distributions and do not reflect fees or expenses. It is not possible to invest directly in an index

Over that same time frame, while the underlying currency basket return was mostly negative, for U.S. dollar investors, MSCI EAFE U.S. Dollar Hedged Index would have outperformed MSCI EAFE Index by roughly 828 bps. As the below chart demonstrates, this can be explained by the contribution of the currency carry to an investor’s returns.

This outperformance of the hedged index over the unhedged index of 8% was entirely a function of the FX forward carry U.S. dollar investors received by hedging their international developed market exposure back into U.S. dollars. Relatively higher interest rates in the U.S. as well as demand for dollar borrowing has benefitted currency hedged investors to the tune of 773bps over this time frame.

Source: DWS calculations, Bloomberg, MSCI as of 9/30/2019. Past performance is not indicative of future returns. Hedged volatility is represented by the volatility of MSCI EAFE U.S. Dollar Hedged Index; unhedged volatility is represented by the volatility of MSCI EAFE Unhedged Index. Index returns assume reinvestment of all distributions and do not reflect fees or expenses. It is not possible to invest directly in an index.

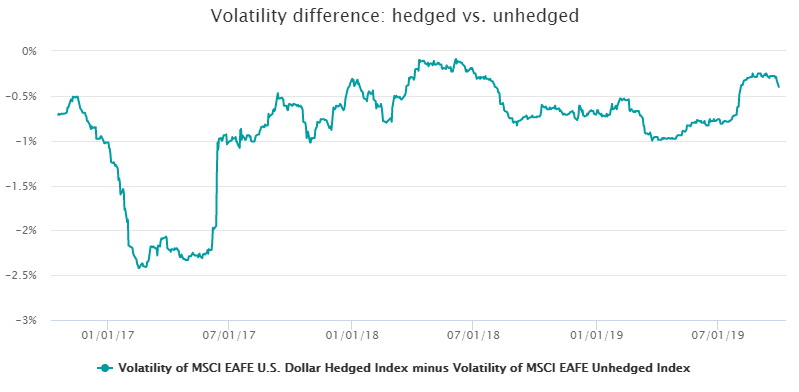

For investors looking to invest in international equities, we’ve long argued that not hedging currency risk has the potential to add price volatility to their return experience. Over the past five years, and in the foreseeable future, as long as U.S. interest rates outyield interest rates in other developed countries, the incremental currency carry U.S. investors receive from hedging their currency risk has been and may continue to be an important contributor to investment returns.