The turmoil on Wall Street early last week reignited talk of the big “R-word.” Recession. Much of it is tied to mounting concerns about cracks in consumer spending. There’s no denying that consumers are digging around for more deals and prioritizing essentials over discretionary items. Consumer discretionary is now the lone negative sector this year, down 2%, while consumer staples are up 11%.

But the retail earnings parade begins in earnest this week, and results from Walmart, Home Depot, and Tapestry will paint a clearer picture – as will July retail sales on Thursday. Home Depot beat on both the top and bottom lines but mentioned homeowners are holding off on major home renovations and cautioned that sales will be weaker in the coming months.

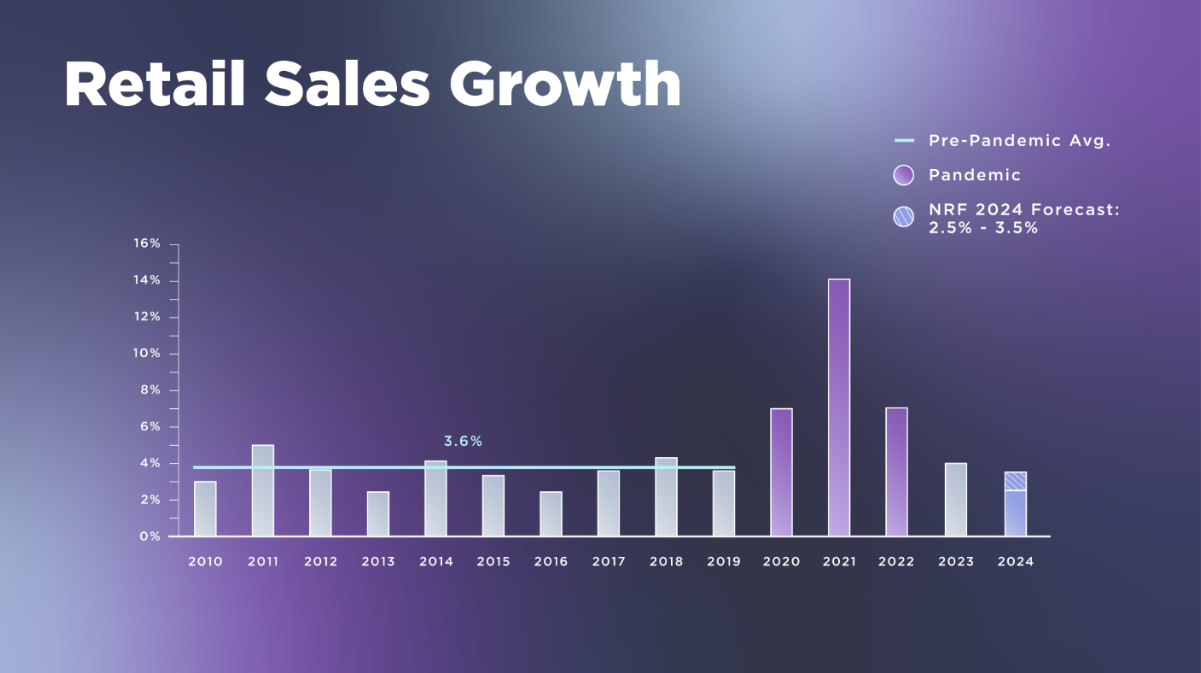

On the data front, economists are expecting a tepid 0.4% rise in monthly retail sales and an even more modest 0.1% when you strip out autos. But for the year, the National Retail Federation projects retail sales will still grow between 2.5% and 3.5%. That’s right in line with the 10-year average annual sales growth before the pandemic.

Online sales are expected to jump between 7-9% year-over-year to roughly $1.5 trillion. Amazon alone boasted a record $14.2 billion in sales from its Prime Day – its biggest shopping event ever, up 11% year-over-year. Millions more Prime members took advantage of the two-day shopping event this year than in 2023, with consumer electronics and back-to-school among the strongest spending categories.

Consumers Getting Pickier

Despite strength in e-commerce, overall credit card spending has started to wane, and we’re seeing some signs the consumer could be feeling the squeeze. A new report by TransUnion found that the average credit card balance in the US is now $6,329, up nearly 5% from last year. The personal savings rate is near an all-time low and loan delinquencies are inching up. Subprime consumers, which make up nearly a third of the U.S. population, are also showing signs of financial strain. As the economy softens, these lower-credit consumers are often the first to take a hit.

Source: Equifax

Christine Short, Head of Research at Wall Street Horizon, noted the consumer may well be getting stretched and are clearly on the hunt for more bargains. “We’ve already heard from some consumer-focused companies, specifically restaurants, and consumer staples, which showed consumer spending continues to cool and that shoppers are more discerning and value-driven,” she said. “Add to that a softening labor scenario, with unemployment rising to 4.3% in July, the highest level since 2021.”

So far, the early innings have turned in decent results from the likes of Costco, Under Armour, and Restaurant Brands. However, there are obvious signs of the consumer’s growing price sensitivity. Burger King and McDonald’s are trying to entice customers back with more value meals. Under Armour’s earnings topped estimates but the retailer noted plummeting online sales after cutting discounts and promotions. Yum Brands CEO David Gibbs spoke about a “more cost-conscious consumer,” as fast-food chains like Taco Bell weather the pullback in consumer spending.

Retail ETF Roundup

Only a handful of retail ETFs exist and, apart from levered products, almost all of them have suffered net outflows for the year. The lone exception has been the VanEck Retail ETF (RTH), which has seen modest net inflows and has risen nearly 6% year-to-date. Meanwhile, the ProShares Online Retail ETF (ONLN) focuses on the online marketplaces themselves, such as Amazon, which makes up more than 22% of its total portfolio. Shares of ONLN are up almost 10% for the year, trading virtually in tandem with Amazon’s stock price.

For a much more diversified approach, the Amplify Online Retail ETF (IBUY) offers a completely different take on e-commerce. The first of its kind, IBUY offers exposure to global companies whose revenues are predominantly tied to online sales – including online marketplaces, online travel, and both traditional and omnichannel retail. Top holdings include Chewy, Carvana, Revolve Group, and eBay. IBUY maintains a 75% exposure to the U.S. and 25% to international markets. The fund charges 0.65% and has suffered modest losses and net outflows for the year. However, if retail spending starts to broaden beyond Amazon, the fund could certainly prove a beneficiary.

Finally, the largest and most liquid product in the space is the SPDR S&P Retail ETF (XRT). The $400 million fund also provides a more broad-based approach, with unconcentrated exposure to big-box retailers and apparel retailers alike. No single holding exceeds 2% of the overall fund.

Overall, while there are signs of consumer strain, particularly among lower-credit consumers, the retail sector shows resilience in certain areas, especially online sales. The upcoming retail earnings and sales data will be crucial in understanding the broader economic impact and consumer behavior trends.

For more news, information, and analysis, visit VettaFi | ETF Trends.