Bull vs. Bear is a weekly feature where the VettaFi writers’ room takes opposite sides for a debate on controversial stocks, strategies, or market ideas — with plenty of discussion of ETF ideas to play either angle. For this edition of Bull vs. Bear, Karrie Gordon and Elle Caruso debated the case for and against increasing allocation to mega caps as the potential for recession looms large.

Karrie Gordon, staff writer, VettaFi: Elle, it’s so great to circle up with you again today, particularly since in our first Bull vs. Bear column, we talked about Meta (META) — which I would like to point out is up 77.3% year-to-date as of Monday, April 24.

I thought I’d shake things up a bit this time around and revisit Meta as well as all its heavyweight class of friends, the mega caps, and give us a chance to weigh whether or not it makes sense to increase mega cap exposure in a recessionary year for the U.S.

Elle Caruso, staff writer, VettaFi: Hi, Karrie! A pleasure to be back at it with you. While I may have been a Meta Bull back in November (and for good reason, look at those numbers!), I’m actually going to take the bear case for overweighting mega caps in the current environment.

While mega caps may be performing well to start the year – with the top 10 names in the S&P 500 responsible for 90% of the index’s gains in Q1 – limiting the weight of mega caps has historically outperformed over longer periods.

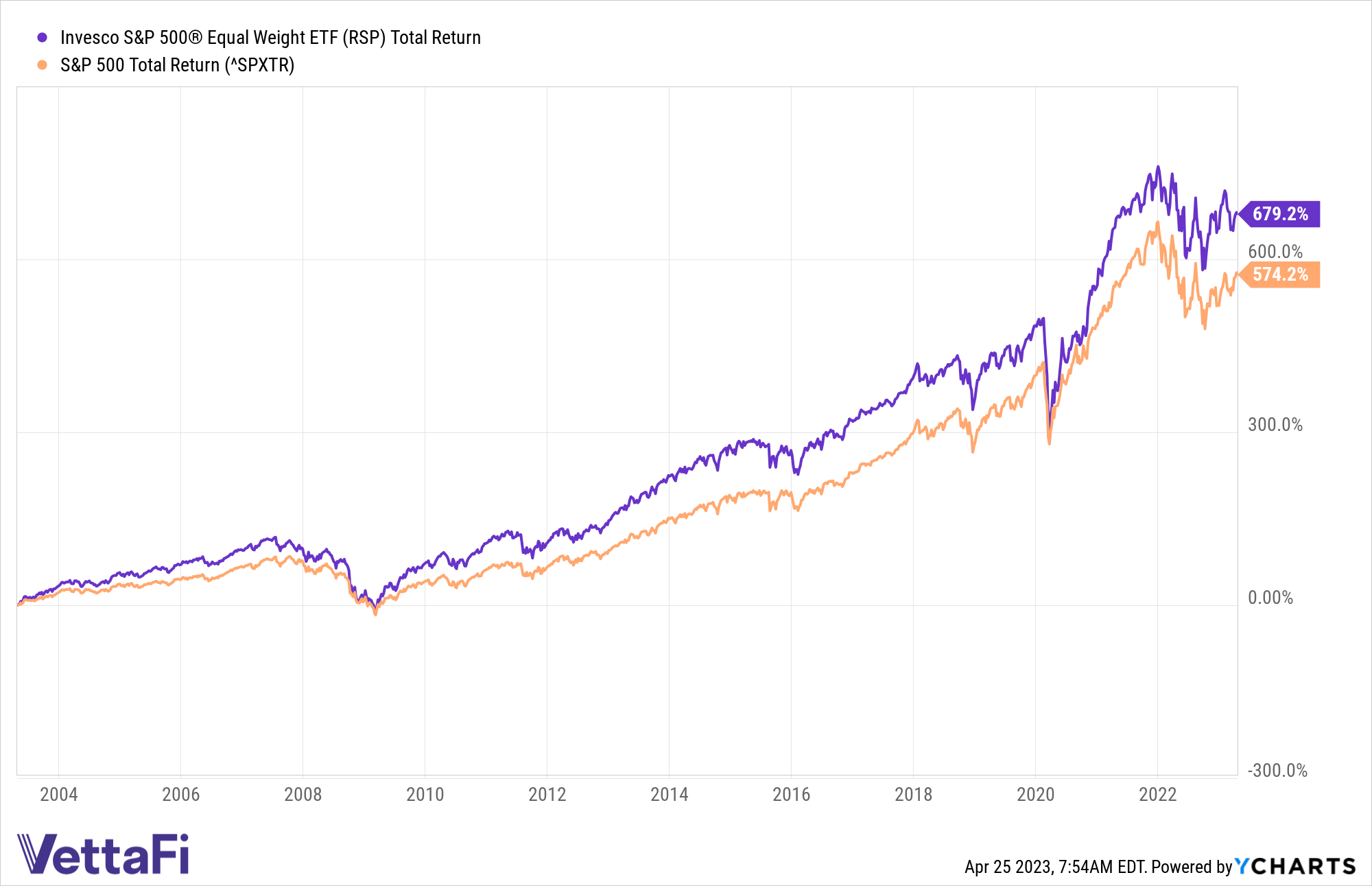

To start, let’s take a look at the Invesco S&P 500® Equal Weight ETF (RSP), which gives every security in the S&P 500 an equal weight at each quarterly rebalance. The fund has outperformed the S&P 500 over various market conditions. The charts below speak for themselves.

Since RSP’s inception on April 24, 2003, the fund has outpaced the S&P 500 by 10,500 basis points. That’s a significant spread!

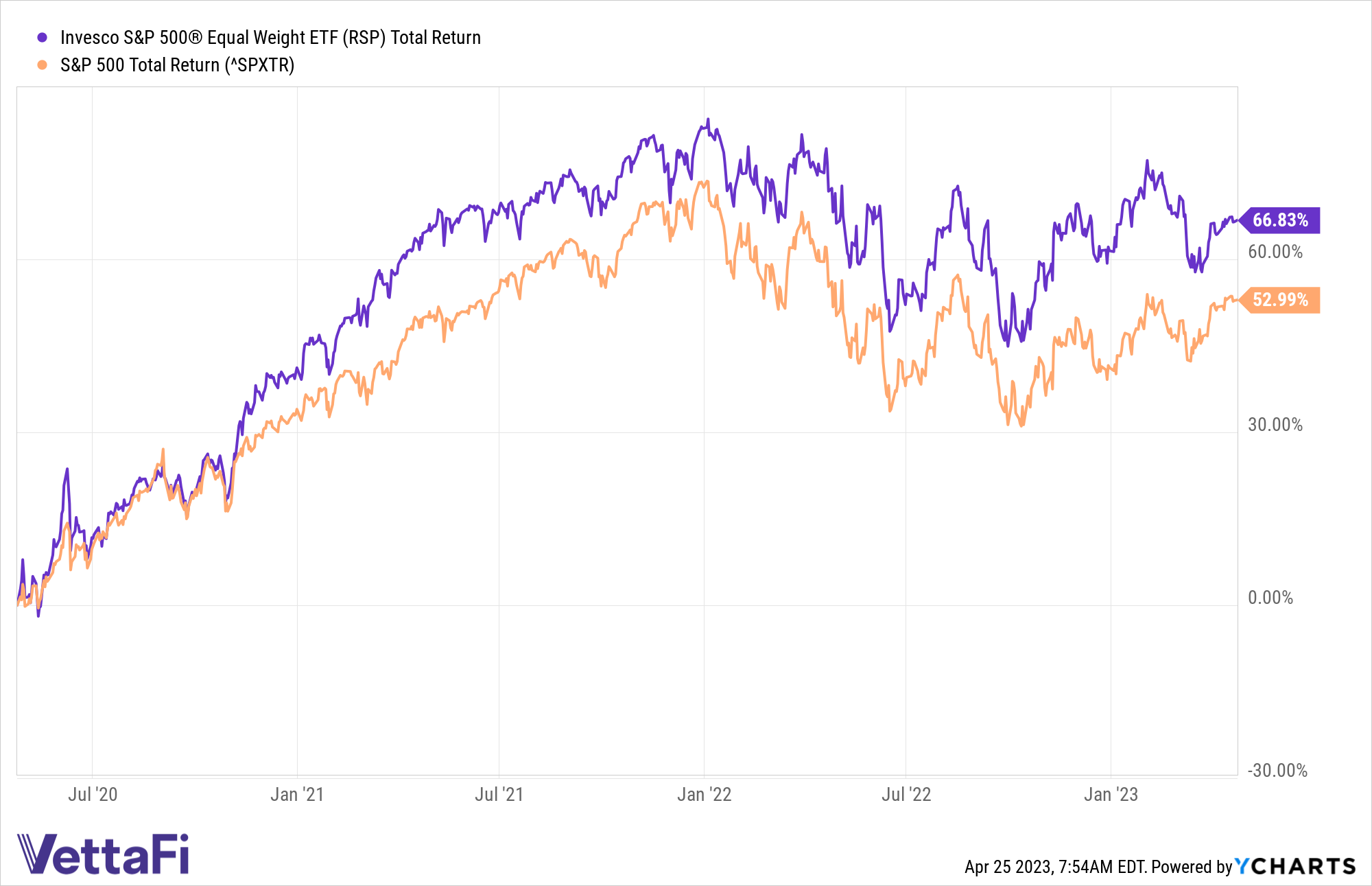

Equal weight continues to outperform in recent history, as RSP has outpaced the S&P 500 by over 1,300 basis points over three years ending April 24.

Gordon: Mega-cap companies are some of the best-known companies and are pillars of market performance. They’re companies with a market capitalization of over $200 billion, and while mega-cap companies change over time as the economy evolves, it’s virtually impossible to invest in the U.S. without core exposure to these equity giants.

It’s because of their outsized nature that they are worth considering added exposure to as the U.S. undergoes a recessionary period because mega-cap companies fall into that bucket of “too big to fail.” Mega caps offer fairly solid business models with long-established performance histories through a variety of economic cycles, often providing a more predictable rate of returns in times when many equities feel the squeeze of economic downturn.

Looking back at the most recent recession and recovery cycle from February 2020 to current, the Invesco S&P 500 Top 50 ETF (XLG) that invests at least 90% of its assets in the S&P 500 Top 50 Index has outperformed the benchmark SPDR S&P 500 ETF Trust (SPY).

It’s not just about performance for mega caps though, it’s about reliable income even during economic drawdowns and recessions. The Vanguard Mega Cap ETF (MGC) is a great example of the steady dividends that mega caps offer historically: in the last two recessionary periods (COVID-19’s onset in 2020 and the Financial Crisis of 2007-2008), MGC issued stable quarterly dividend payouts to shareholders that dropped a maximum of six cents a share only to rebound well above the pre-recession amount. It’s this stability that adds to the argument for increased mega-cap exposure during economic downturns and recessions when income generation becomes a higher priority.

Caruso: Sure, mega caps are pillars of market performance – but I don’t think they should be. Investors are currently facing historic levels of concentration risk. Mega caps have dominated cap-weighted indexes and funds over the past few years and have had an outsized impact on returns. This doesn’t come without significant risk.

As of the end of 2022, the top 10 companies in the S&P 500 accounted for roughly $8.2 trillion, or 26% of the value of the S&P 500. Just last month, the combined weight of the two largest constituents – Apple (AAPL) and Microsoft (MSFT) – reached the highest level on record, comprising 13.3% of the S&P 500 by weight.

It’s particularly timely that we’re discussing mega caps now, amid Big Tech earnings, as that was a large contributor to the S&P 500’s dismal performance last year. Apple declined 26.4% on a total return basis in 2022 (that’s right, I’m counting those dividends too), making it the largest contributing constituent to the S&P 500’s disappointing showing. Amazon.com (AMZN) and Tesla (TSLA) followed, falling 49.6% and 65.0% in 2022, respectively (the latter even fell right out of the top 10!) Shares of Microsoft dropped 28.0%, and Meta (META) plummeted 64.2% last year (also falling out of the top 10).

During that market downturn, the largest S&P 500 companies shed a greater share of value than other constituents in the index. The market cap of the 10 largest names in the index declined 37% from 2021. Meanwhile, the combined market value of all companies in the index fell about 20% during the year, according to S&P Dow Jones Indices.

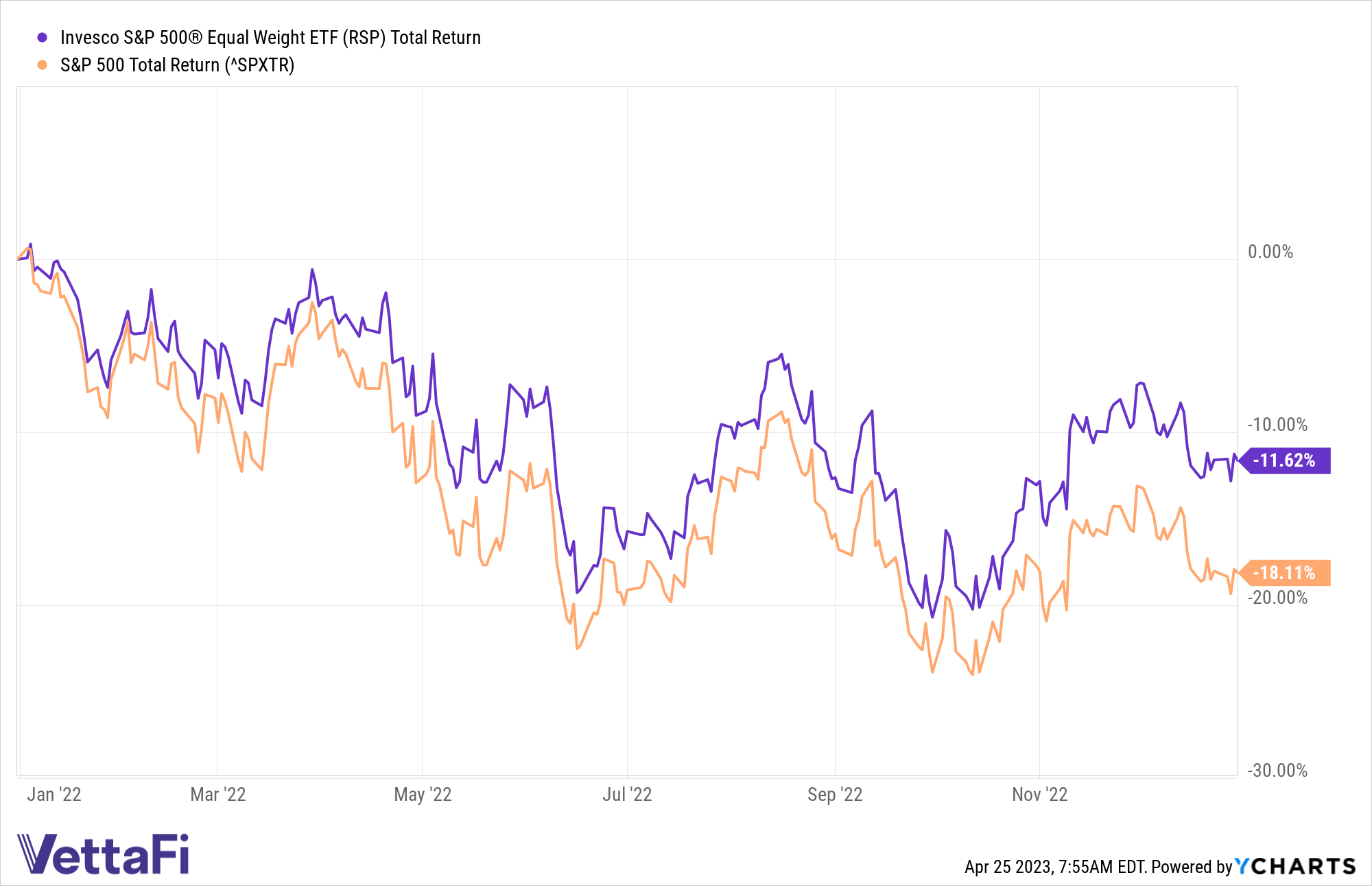

Investors in RSP, who effectively limited their exposure to mega caps, were spared some of the losses that cap-weight S&P 500 investors faced during the challenging year. As demonstrated in the chart below, RSP declined 11.62% last year while the S&P 500 declined 18.11%, each on a total return basis.

Gordon: Let’s not pull punches here, mega caps unequivocally underperformed last year. But one of the main reasons I’m all for increasing exposure to these heavy hitters is because the factors that weighed them down last year look to be largely resolving in 2023.

The aggressive Fed rate hiking regime of the past year that took interest rates from zero bounds to 5% where they currently sit. It wreaked havoc on equities and bonds alike but a leveling off of rate hikes this year while broad inflation continues to fall could prove a boon in the mid-term.

Just the hint of rate hikes easing alongside falling inflation so far this year has led to a strong rebound in technology mega caps, in particular, YTD: Meta soared 77.37%, Apple is up 27.25%, and Microsoft is up 17.33% as of Monday, April 24.

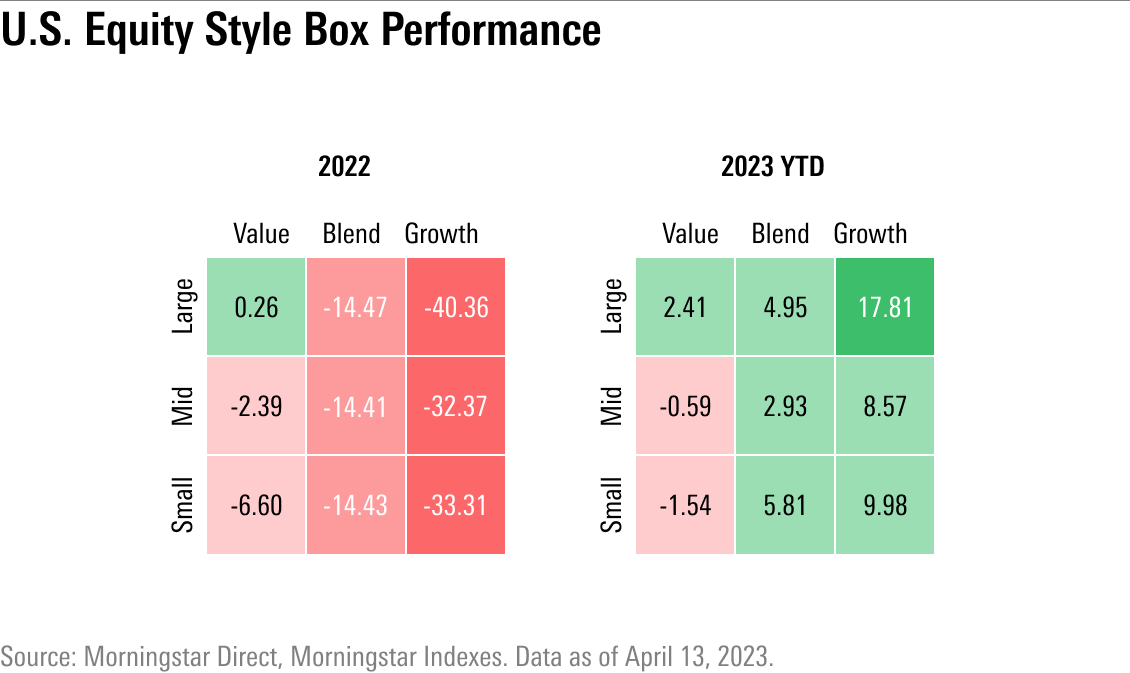

Image source: Morningstar

I don’t have a crystal ball and past performance is never indicative of future performance but it’s worth noting the rebound potential inherent in growth-oriented stocks and mega-cap technology companies in particular once impending (or possibly current) recession eases.

It’s also worth highlighting the great price opportunity right now in many mega-cap companies that are currently undervalued with reduced price-to-earnings ratios compared to their historic averages. Google’s parent Alphabet (GOOGL) has a current P/E ratio of 23.49 YTD and forward P/E of 20.90 compared to its five-year average of 29.50 while Johnson and Johnson (JNJ) has a P/E ratio of 34.22 YTD and forward P/E of 15.36 compared to its five-year average of 63.35.

Given the rebound potential of mega caps and an environment where mega caps stand to benefit in the mid-term as inflation and rate hikes ease and recession is resolved, the coming months are an ideal time to consider gaining added exposure to the future drivers of a recovering economy while also hedging into the added safety that mega caps can provide during recessionary times.

The Vanguard Mega Cap Growth ETF (MGK) is a fund to consider that was down –34.01% in 2022 but is up 18.35% YTD for those wanting a growth tilt, or the broader exposure Vanguard Mega Cap ETF (MGC) that was down –21.23% last year and is up 8.98% YTD. For reference, over the same period, the S&P 500 was down –19.44% in 2022 and is up 7.68% YTD.

Caruso: I see overweighting mega caps as a bet on the continuance of existing trends in the market — betting that the same large names will continue to generate strong returns. However, history has demonstrated that the largest companies as measured by market capitalization do not maintain their position forever. Even if they do look like a good buy on paper.

In 2003, the largest constituents in the S&P 500 included Wal-Mart Stores (WMT), General Motors (GM), Exxon Mobil (XOM), Ford Motor (F), General Electric (GE), Citigroup (C), ChevronTexaco (now Chevron [CVX]), IBM (IBM), AIG (AIG), and Verizon (VZ).

Twenty years later (as of December 31, 2022), the largest U.S. companies have entirely changed, and now include Apple, Microsoft, Amazon., Berkshire Hathaway (BRK.A), Google, UnitedHealth Group (UNH), J&J, Exxon, JP Morgan Chase & Co (JPM), and NVIDIA (NVDA). The only overlap is Exxon – but even Exxon fell out of the top 10 between 2010 and last year’s energy rally.

Focusing again on the two largest names, Apple and Microsoft: I can’t help but wonder how they could continue to grow meaningfully. After all, as of the end of 2022, Apple and Microsoft individually had greater total market cap than the entire S&P 500 utilities, real estate, and materials sectors, according to data from Bloomberg. Combined, their market cap is comparable to that of the entire S&P 500 financial sector. Is there really much more room to run?

Gordon: You’re right. The mega caps of today may not be the mega caps of tomorrow, but that doesn’t mean that companies that have fallen in valuation go on to inherently underperform. Many still retain the attractive qualities that they held as mega caps. Just look at Cisco (CSCO) which was a top company in 2000 but is currently shy of the $200 billion valuation mark. Cisco had a P/E ratio of 12.19 a decade ago (2013) but currently has a P/E of 17.36, with a historical forward P/E of 11.21 compared to the current 11.98, according to Morningstar data.

We’re talking about the mega caps of today though, and the current environment really is a huge reason I’m so bullish on mega caps in the near term. This potential recessionary cycle carries with it an additional element of bank risk that further enhances the bull case for mega caps right now. Tighter lending conditions from banks on the heels of regional bank collapses alongside persistent inflation will continue to have an impact on consumer spending as well as create cash flow problems for less-established businesses.

In an environment of reduced liquidity such as a recession, mega caps are extremely appealing for institutional and retail investors alike because of the deep liquidity they offer and leaning into mega caps specifically reduces regional bank exposure in portfolios.

In the weeks following the failure of Silicon Valley Bank and Signature Bank, investors flooded into safe hedges as banking sector contagion fears grew. The winners? Treasuries and mega caps. Microsoft’s price rose 10% between March 10-17, peaking at a 130% rise in trading volume (nearly 70 million) on March 17 over the average daily trading volume, while Google’s price rose 10.07% over the same period with trading volume increases of 58% (60 million) above the average on March 17.

In a recessionary environment, liquidity is king, and mega caps will continue to offer that in abundance and remain a safer bet for most advisors and investors, but it’s a bet that doesn’t have to be inherently tilted towards growth and technology during economic drawdown.

The Dow Jones Industrial Average is comprised of 30 blue chip companies and nearly half of those (13) are mega caps but only two of those are from the technology sector. The SPDR Dow Jones Industrial Average ETF (DIA) is a great fund to gain diversified sector exposure with significant weighting to mega caps, and for a value tilt with top sector allocations to healthcare, financials, and consumer staples, the Vanguard Mega Cap Value ETF (MGV) is also worth consideration.

Caruso: Karrie, I’ve had a great time discussing the merits of overweighting mega caps, but the concentration risk is still top of mind for me. We’ll have to check back in later this year to assess how things have played out!

Gordon: Elle, it’s been really great talking these market heavyweights and if they’re worth betting bigger on this year. The case for increased allocation to mega caps in a recessionary and challenging economic and market environment seems pretty solid to me. It’s hard to argue with steadier returns, reliable distributions, and deep liquidity that keeps portfolios flexible in volatile and uncertain times. I’m looking forward to checking in later this year but for now, I think it’s time for this bull to hang up the boxing gloves.

For more news, information, and analysis, visit the Portfolio Strategies Channel.