Investors and markets remain highly focused on economic data, looking for clear indicators of the direction of inflation and interest rates in the second half. Brian Hess, investment strategist at Natixis Investment Managers, moderated a discussion in a recent Natixis webinar that analyzed the likelihood of a soft landing and the path of interest rates in the second half.

Reason for Rates Optimism?

A hopeful Consumer Price Index reading in May lends credence to the potential for a soft landing. Headline inflation remained flat month-over-month while core CPI (excludes energy and food) rose 0.163% on expectations of .3%.

“When you pull back the layers, a lot of really good reasons to be optimistic,” explained Garrett Melson, CFA, portfolio strategist at Natixis Investment Managers. “Thinking about Powell’s checklist, it’s core goods, super core services, and shelter.”

Both super core services and core goods fell into deflationary territory, leaving shelter as the primary culprit for inflation in May. This reflects a broadening of disinflationary pressures beyond what was seen in the first quarter and could prove hopeful for improving inflationary conditions.

The most recent Fed meeting brought with it a downgrade of expectations to just one single interest rate cut this year. However, looking at the SEP, or Fed “dot plot,” one rate cut was the median range.

The dot plot is constructed from the anonymous perspectives of 12 Fed regional presidents and seven Fed governors. Jack Janasiewicz, CFA, portfolio manager, and portfolio strategist at Natixis, revealed that if just one more official had voted for two cuts, the median would have bumped to two 25-basis cuts this year.

“We would call the dot plot converging to what the market’s already pricing in,” Janasiewicz said. “It’s really not about the rate cuts — it’s more that they’re simply not hiking, and there’s a big differentiation there.”

Diving Into Consumer Resilience and Purchasing Power

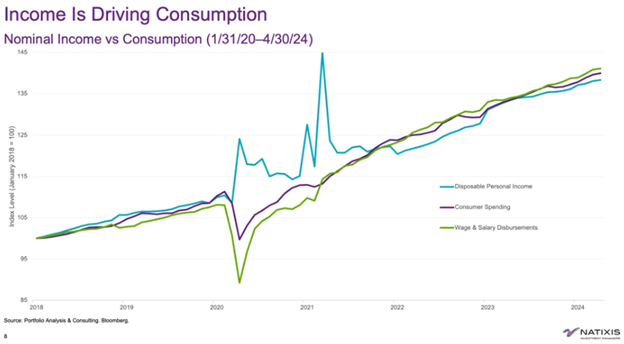

Despite May’s flat inflation print, sustained elevated prices continue to eat into consumer purchasing power. Credit card debt sits at all-time highs, and delinquencies remain on the rise. However, the rise in credit card debt adheres closely to its long-term trend of consistent, rising debt over time. When weighed against higher wages and asset gains, Melson believes the consumer balance sheet remains robust.

Image source: Natixis Investment Managers

“The vast majority of the consumer continues to hold up very, very well,” Melson noted. That said, “you are certainly seeing some signs of stress.” The rising bifurcation between lower income consumers and higher earning consumers remains notable.

Natixis broke out credit card delinquencies by zip code and found that lower income households were hardest hit.

While Melson forecasts moderation in consumer consumption throughout the second half, that leveling off begins from an elevated point at the beginning of the year. “Slowing and moderating from there does not mean we’re going into stagflation or recession. It just simply means moderating something that looks a lot more like a trend.”

Shelter and Car Insurance Carry Inflation… For Now

The main culprits for inflation currently fall into two categories: shelter and car insurance. Shelter diverged in the first quarter, with rents continuing to fall while Owner’s Equivalent Rent (OER) rose. Those two should begin to move more in tandem as disinflation kicks in.

The lag in shelter prices also carries over to auto insurance. Both show signs of softening in recent months and, according to Melson, prove promising looking ahead.

The disinflationary trend, alongside softening in the two categories currently driving inflation, could lead to low to flat CPI prints in the coming months. Janasiewicz believes that a reigniting of inflation would need to be driven by the consumer. Rising wages and a tightening job market would bear such a rise. Wage growth currently continues to decline, returning towards trend. What’s more, June’s jobs report reflected an increase in the unemployment rate and potential slowing.

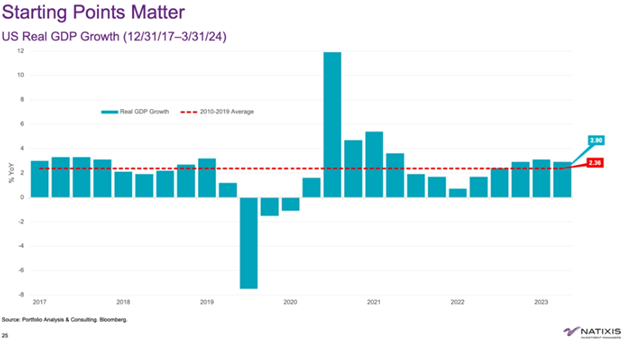

Meanwhile, real GDP growth may be lower than post-pandemic growth, but it also reflects a return to trend, according to Janasiewicz.

Image source: Natixis Investment Managers

“Historically speaking, if we go back and look at maybe the last ten years or so, that level’s been coming in at around 2.36%. We’re almost a good 50 plus basis points above that growth rate,” Janasiewicz explained. “I think that’s a pretty good backdrop for what we might consider a soft landing.”

For more news, information, and analysis, visit the Portfolio Construction Channel.