As worries about a near-term recession continue to fade, strategists now look to political impacts as the dominant second-half risk. Rates, inflation, and government rounded out macro concerns, according to a recent strategist survey from Natixis Investment Managers.

Natixis discussed the findings of their mid-year strategist pulse check in the 2024 Strategist Outlook: July Surprise. The survey included 30 market strategists across the Natixis family. These detailed macro risks and market opportunities (covered in a subsequent article) in the latter half of the year.

Political Impacts Top of Mind for Strategists

The U.S. presidential election looms large over markets late this year, and strategists rank it either medium risk (37%) or high risk (37%). The majority of global strategists (47%) believe the election may prove a headwind in the second half.

“Asked to predict how it will shape up at year-end, 60% of those surveyed think the US election is more likely to weigh on the market rather than support it,” Natixis wrote. However, 23% viewed the election as tailwind potential, while 30% believed it was mostly noise.

Beyond the potential turmoil created by an election (or unclear election outcomes, a concern before President Biden stepped aside), those surveyed also reported worries of the “politization” of the Federal Reserve during its rate cutting regime.

Looking further afield than the U.S. election, strategists overwhelmingly believe (80%) global geopolitics pose significant headwind potential in the second half. Between the ongoing wars in Ukraine, Gaza, and Israel and U.S.-China relations, geopolitical risk is rampant. Geopolitics, alongside consumer spending, are currently the top watched factors by strategists in the second half.

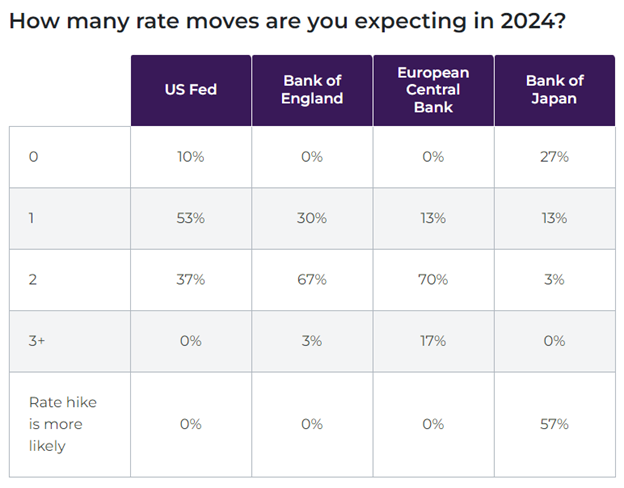

Inflation, Rates, and Government Spending

Inflation continues its slow decline in the U.S. but remains elevated. Nearly half of strategists (47%) surveyed believe inflation posts a medium risk in the latter half of the year. Notably, only 17% believe it poses a high risk. The impacts of inflation, however, will likely continue for consumers in H2, with Gen Z (those born 1997-2012) predicted to take the hardest hit.

With declining inflation comes a concern about higher for longer interest rates. “Their concern is further reflected in the 63% who are more worried about the number of cuts than the timing of any cuts,” explained Natixis.

Image source: Natixis Investment Managers

A major concern revolves around the coordination of central banks globally in their rate-cutting regime. Most strategists (70%) predict two rate cuts for the European Central Bank and two cuts by the Bank of England (67%), while 53% predict a single cut in the U.S. Slightly over a third (37%) believe the Fed will cut rates twice this year.

Rounding out risks is that of growing government debt. 70% of those surveyed reported that government deficits affect their market evaluation. “The question isn’t if high debt levels are sustainable but rather for just how long,” explained Natixis.

Only 10% reported no concerns regarding debt levels, while 37% believe current levels are unsustainable. Over half (53%) believe current deficits are sustainable but pose threats to the economy in the long term.

“The uncertainty of the US election cycle and geopolitical disruption may loom over markets in H2, but Natixis strategists see that the fate of markets will more likely be determined in the details of economic and monetary policy,” wrote the authors. “Inflation may have eased, but interest-rate cuts will need to be coordinated by central banks to complete the soft landing.”

For more news, information, and analysis, visit the Portfolio Construction Channel.