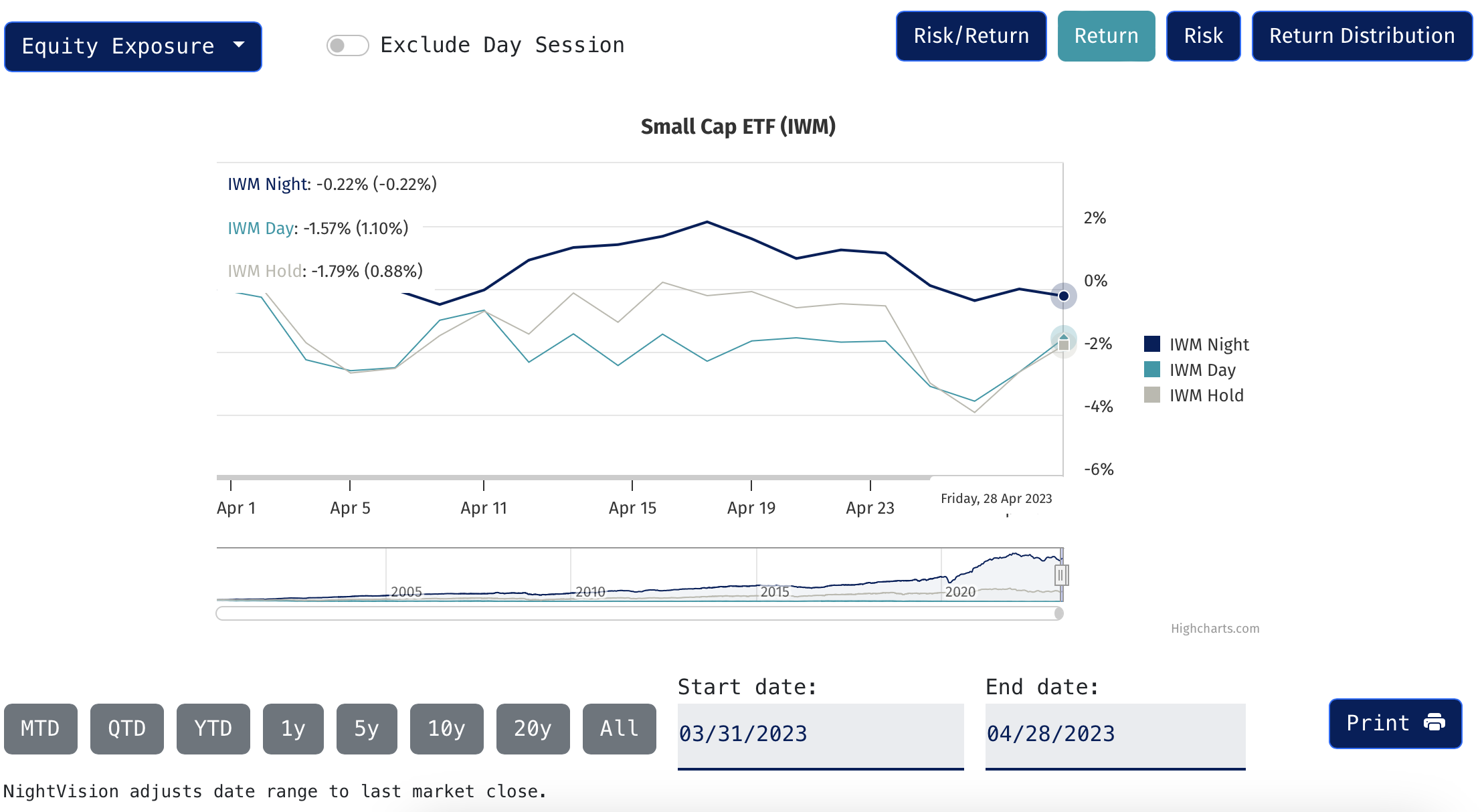

Small-cap investors who were out of the market during the day managed to limit losses and dampen volatility in April.

During the month, the iShares Russell 2000 ETF (IWM) fell 1.8%. The night session held relatively stable, declining just 0.2%, while the day session dropped 1.8%, according to NightVision and NightWatch Mobile App. This is referred to as the night effect, a market anomaly whereby overnight markets have historically outperformed the daytime trading session on a risk-adjusted basis.

Source: NightVision

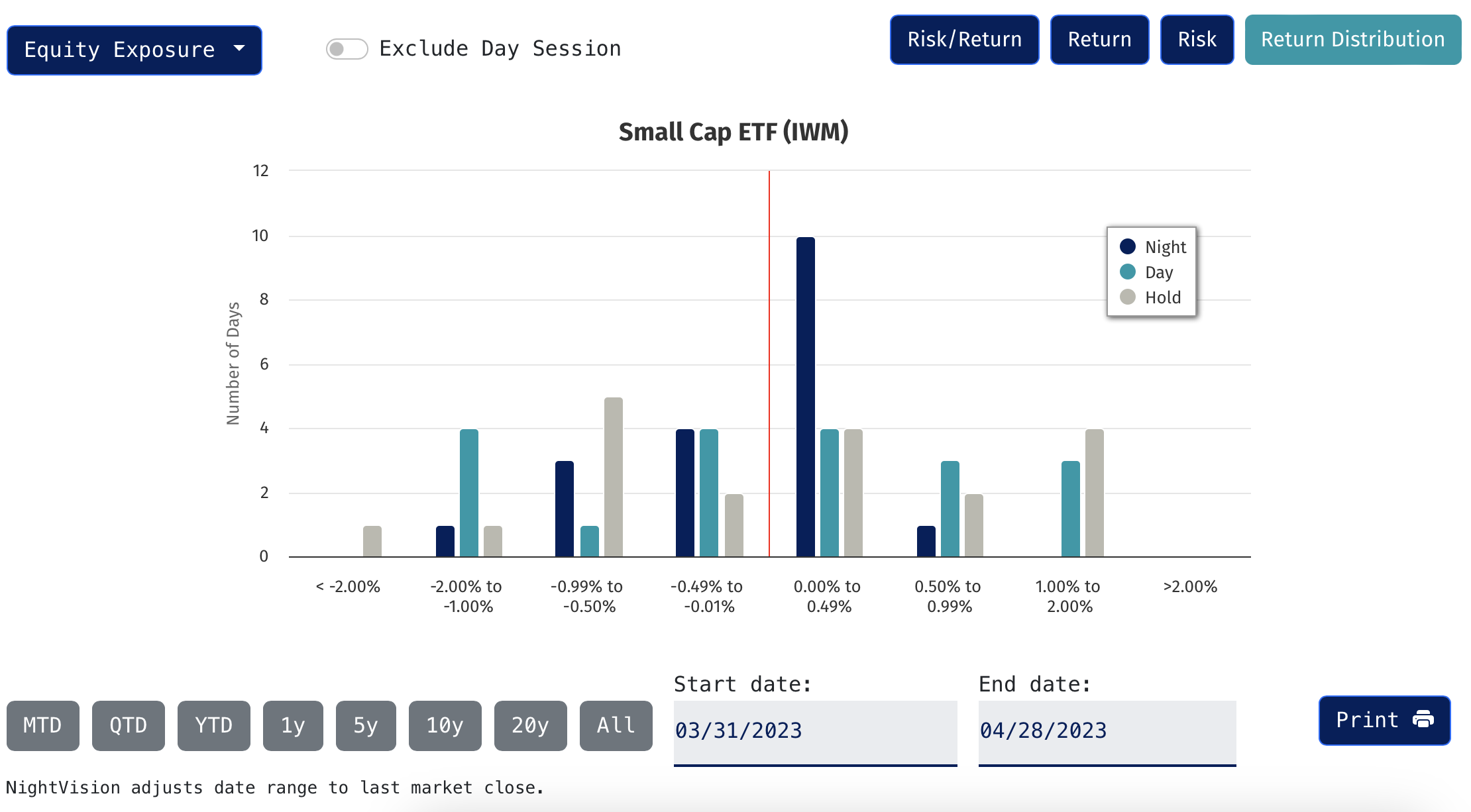

Both IWM’s day and night sessions were less volatile than historical averages in April; however, investors in the day still took on significantly more volatility than those who only held the fund at night as measured by the number of tail days in both directions (< -1.00 or >1.00).

In April, 32% of buy-and-hold sessions were in the tails, compared to the historical average of 40% of hold sessions in the tails. The day session of IWM had 37% tail days, compared to 33% of day sessions historically being in the tails. Just one night session (about 5% of all sessions during the month) was in the tails, compared to 13% historically, according to data from NightShares.

Source: NightVision

The NightShares 2000 ETF (NIWM) provides exposure to the night performance of 2000 small-cap U.S. companies (comparable to the night session of the Russell 2000 or IWM).

Looking at the IWM Sharpe ratio over 20 years (2003 through 2022) underscores the power of the night effect. The buy-and-hold session Sharpe ratio is 0.46. Meanwhile, the night session Sharpe ratio is 0.90, while the day session Sharpe ratio is -0.08. The day session Sharpe ratio is negative as the session’s returns over the 20-year period have been negative, meaning over 100% of the fund’s returns have come at night.

For more news, information, and analysis, visit the Night Effect Channel.