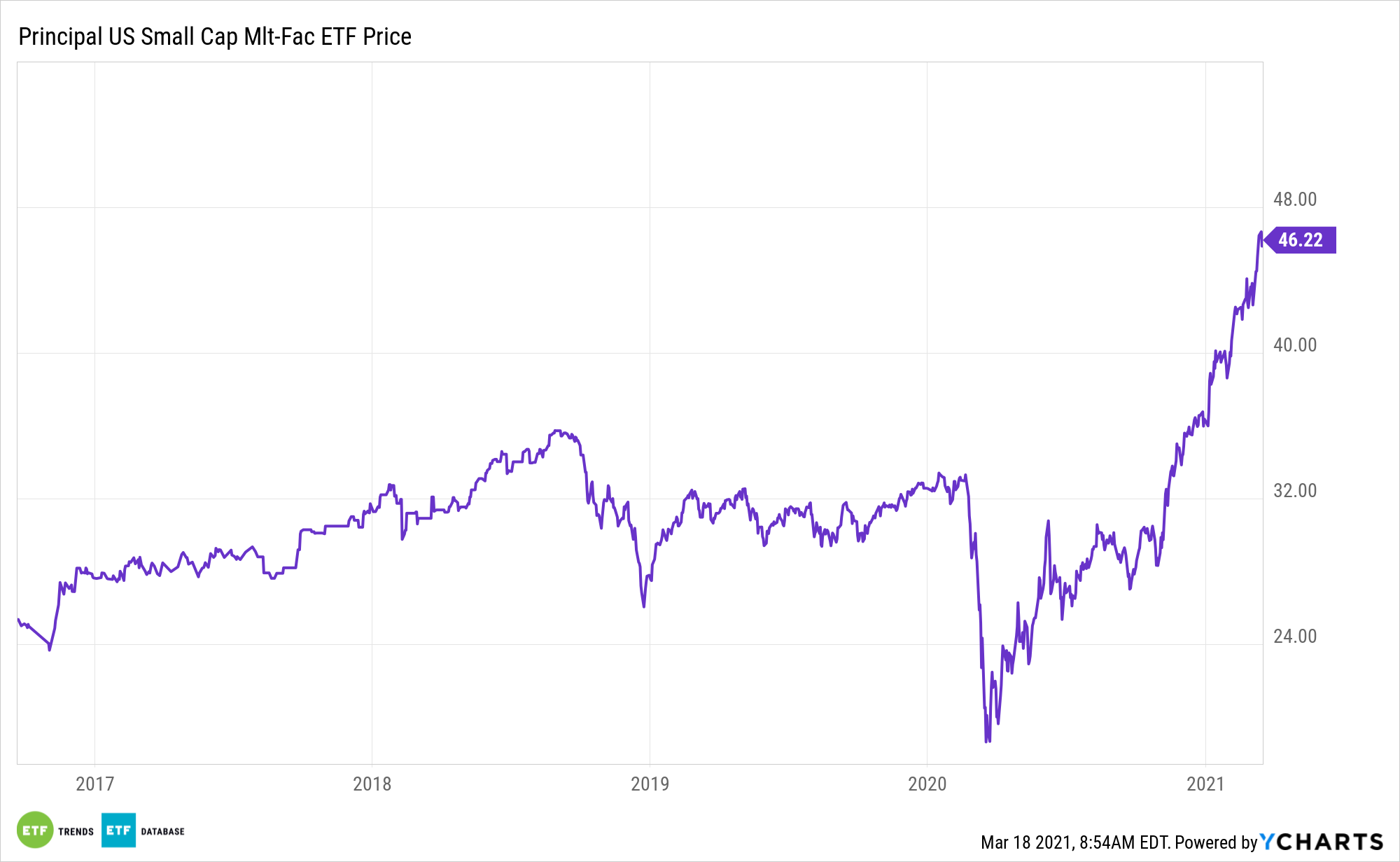

With small cap stocks currently standing out, investors may want to consider a multi-factor approach to the group. That’s accessible via an array of exchange traded funds, including the Principal’s U.S. Small-Cap Multi-Factor Index ETF (NASDAQ: PSC).

PSC’s underlying benchmark, the Nasdaq US Small Cap Select Leaders Index, “uses a quantitative model designed to identify equity securities (including growth and value stock) of small-capitalization companies in the Nasdaq US Small Cap Index (the ‘parent index’) that exhibit potential for high degrees of sustainable shareholder yield, pricing power, and strong momentum while adjusting for liquidity and quality,” according to Principal.

There are good reasons to go beyond traditional cap-weighted strategies with smaller stocks.

“While most multifactor funds focus on large- and mid-cap stocks, the payoff to factor investing has tended to be larger among smaller stocks,” writes Morningstar analyst Ryan Jackson. “Small-cap stocks may not always be in favor, but those who believe in factors should consider small-cap multifactor strategies, which have greater potential to beat their relevant benchmark than large-cap multifactor funds.”

With PSC, the Probabilities Look Compelling

PSC is worth a look as the economy rebounds from the ill effects of the COVID-19 pandemic. While investors may flock to the relative safety of large cap equities during a recession to lessen the blow of market volatility and provide a cushion during market downturn, small cap performance is worth watching as the economy exits a recession.

Historically, the small cap/value combination has been rewarding, but it took a big hit when value languished during the recently deceased bull market. The tendency of factor leadership to change from year to year underscores PSC’s utility: with the Principal ETF’s multi-factor approach, investors don’t incur the burden of factor timing.

“The value, momentum, low-volatility, size, and quality factors have historically been linked with superior risk-adjusted performance. The payoffs to value, momentum, and low volatility have tended to be greater among small-cap stocks,” continues Jackson.

Mispricing in the small cap market increases the allure of PSC’s multi-factor approach.

“Inefficiencies in the small-cap market offer the best explanation for these factors’ greater payoffs among smaller stocks,” adds Jackson. “Stock mispricing is more likely further down the market-cap scale. Smaller firms don’t receive the same degree of attention as their large-cap brethren. Because mispricing likely contributes to the success of each factor, it makes sense that greater mispricing would contribute to greater factor efficacy among smaller stocks.”

For more news, information, and strategy, visit the Nasdaq Portfolio Solutions Channel.

The opinions and forecasts expressed herein are solely those of Tom Lydon, and may not actually come to pass. Information on this site should not be used or construed as an offer to sell, a solicitation of an offer to buy, or a recommendation for any product.