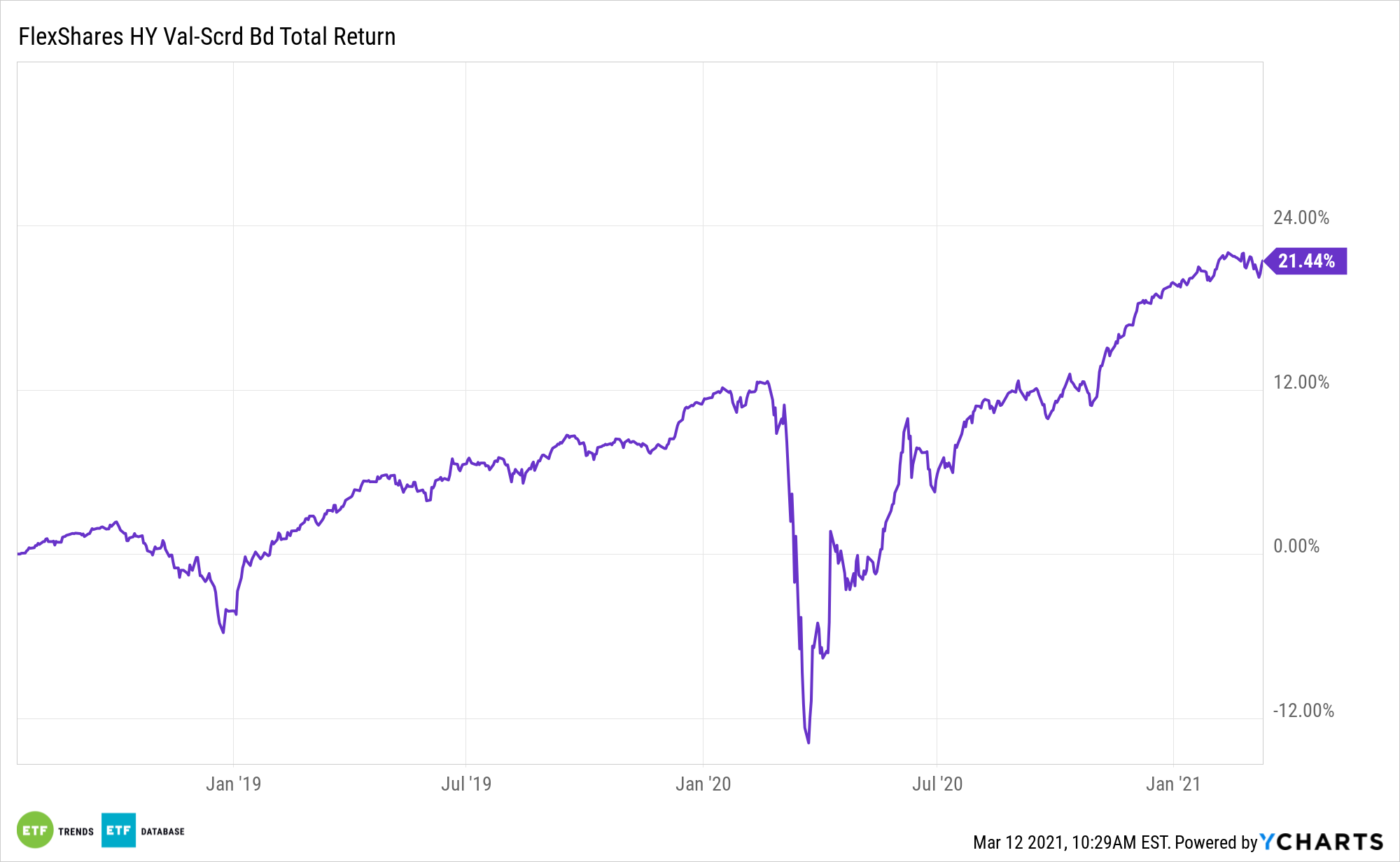

An emerging credit spread scenario could highlight opportunity with funds like the FlexShares High Yield Value-Scored Bond Index Fund (NYSEArca: HYGV).

HYGV’s index reflects the performance of a broad universe of U.S.-dollar denominated high yield corporate bonds that seeks a higher total return than the overall high yield corporate bond market, as represented by the Northern Trust High Yield US Corporate Bond IndexSM. The fund generally will invest under normal circumstances at least 80% of its total assets (exclusive of collateral held from securities lending) in the securities of its index.

“Both the average expected default frequency metric of U.S./Canadian issuers and first-quarter 2021’s credit rating revisions of U.S. high-yield issuers favor a renewed narrowing of the high-yield bond spread,” according to Moody’s Investors Service. “The net downgrades of U.S. high-yield issuers have sunk to a record low -55 thus far in 2021’s first quarter. Negative net downgrades imply the number of high-yield downgrades (40) was less than the number of high-yield upgrades (95).”

How a Return to ‘Risk On’ Can Lift ‘HYGV’

With yields on U.S. government debt depressed and likely to remain that way for several years, advisors are looking to other corners of the bond market to source income. Predictability, some will embrace high-yield corporate debt and its associated exchange traded funds.

HYGV focuses on value by pursuing the higher risk/return potential found by concentrating on a targeted credit beta; utilizing Northern Trust Credit Scoring methodology to eliminate the bottom 10% of issuers; performing liquidity assessment based on issuer’s debt outstanding, age, and remaining time to maturity with the purpose of eliminating the bottom 5% illiquid securities; and intending to match the duration of a market cap-weighted index (ICE BofAML US High Yield Index) while maintaining sector neutrality.

“The high-yield bond spread was much wider than what might be inferred from 1998-2000’s rapid economic growth mostly because the core pretax profits of U.S. nonfinancial companies contracted 6.7% annually, on average, during 1998-2000, after having advanced by15.8% annually on average during 1993-1997,” adds Moody’s.

Volatility rankings have acted as an early indicator of rating changes. After reviewing rating changes from B to BB and vice versa over a period from the 4th quarter of 1996 through the 2nd quarter of 2019, it was shown that a bond’s volatility ranking generally started to improve 25–30 months before the rating upgrade happened. Low-volatility bonds have also historically exhibited less credit risk than high volatility bonds.

For more on multi-asset strategies, visit our Multi-Asset Channel.

The opinions and forecasts expressed herein are solely those of Tom Lydon, and may not actually come to pass. Information on this site should not be used or construed as an offer to sell, a solicitation of an offer to buy, or a recommendation for any product.