Given the prolonged market uncertainty of the last 18 months, it’s no wonder that investors increasingly turn to covered calls to maximize equity income potential. Covered call ETFs continue to experience strong inflows this year as investors look to mitigate volatility and capture income opportunities.

The enormous popularity of funds like the JPMorgan Equity Premium Income ETF (JEPI) showcases the growing appetite for covered call strategies. While many investors shy away from options for their complexity, there is great value in understanding and deploying options strategies in portfolios, particularly covered calls.

Interested in looking to enhance your fixed income allocations? Want to learn more about the benefits of covered calls? Don’t miss the Fixed Income Symposium on Monday, July 24 at 11:00 Eastern. Follow this link to register.

What Is a Covered Call?

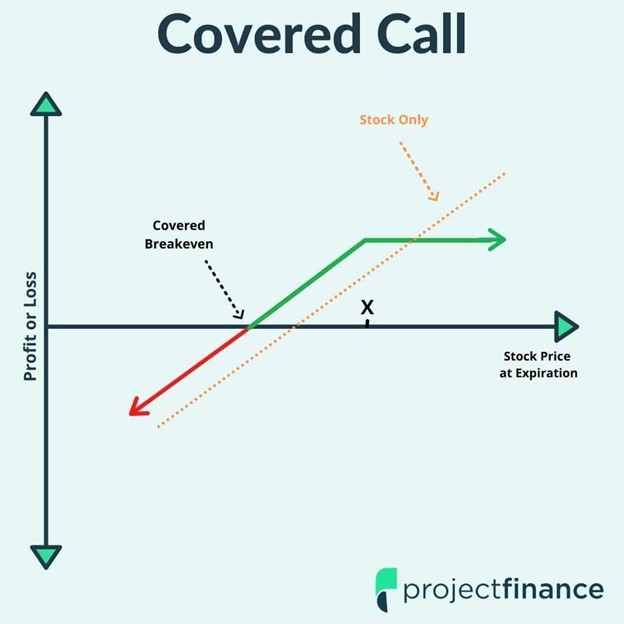

A covered call entails holding an underlying security while also writing a call on it. The writer of the call agrees to sell the underlying security at a strike price on a specific date. The purchaser of the covered call can exercise the call at any point up until expiration, thereby calling away the underlying asset. Those that purchase the covered call carry no obligation to exercise it.

Covered calls are popular because of the income generated from the premiums paid by the purchaser. These premiums can help to make up for stock declines should the underlying security fall before the option expires. They also can enhance income potential should the underlying stock gain but not rise above the strike price at expiration.

However, they do limit the ability to profit from upside potential of a stock should the stock rise above the strike price (considered in the money).

Image source: Project Finance

Ways to Deploy Covered Calls

Covered calls have a number of applications in a variety of options strategies. While some funds utilize straightforward call options, others employ them in ladders. Ladders allow options traders and fund managers to position for volatility, both market-wide and specific to the underlying stock held. Short call ladders are generally used when high volatility is expected for the underlying asset. A long call ladder is generally used when volatility is expected to be minimal.

There are an increasing number of funds that layer in covered calls, seeking to maximize income opportunities. The NEOS S&P 500 High Income ETF (SPYI) is one such fund that continues to garner strong flows this year, up $178 million YTD.

SPYI seeks to provide higher income through call options the fund writes that it then earns premiums on. It then can use the money earned from the written calls to buy long, out-of-the-money call options on the S&P 500 Index.

An out-of-the-money call option has no intrinsic value. That’s because the current price of the underlying asset is below the strike price of the call. Should equities rise or fall, NEOS can actively manage the call options to capture gains in the underlying assets or minimize losses.

The options that the fund uses are index options, taxed favorably as Section 1256 Contracts under IRS rules. Options held at the end of the year are treated like they were sold on the last market day of the year at fair value. Any capital gains or losses are taxed as 60% long-term and 40% short-term, no matter how long investors held them. This can offer noteworthy tax advantages.

The fund’s managers also engage in tax-loss harvesting opportunities throughout the year on the call options, equity holdings, or both.

SPYI has an expense ratio of 0.68%.

For more news, information, and analysis, visit the Tax-Efficient Income Channel.