One of WisdomTree’s flagship value Funds made some notable changes at the start of the new year.

The WisdomTree U.S. Quality Shareholder Yield Fund (QSY) was rebranded as the WisdomTree U.S. Value Fund (WTV). In addition, its expense ratio was reduced by 26 basis points (bps), to 12 bps.

While the name of the Fund has changed, its investment objective remains intact and continues to provide exposure to high-quality companies that are cheaply valued relative to their fundamental characteristics.

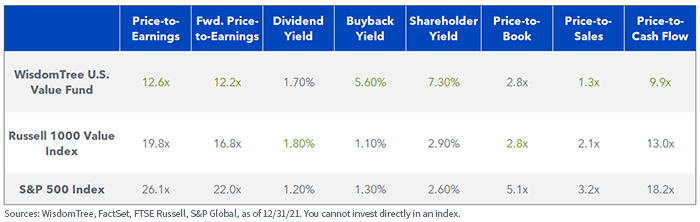

WTV is currently valued at a steep discount to the Russell 1000 Value and S&P 500 indexes across almost every measure of value, including a more than 30% discount to the value benchmarks on price-to-earnings.

In our view, WTV uses one of the most effective measures of value to select its constituents—shareholder yield. The companies in WTV are returning significant levels of capital, through dividend and buybacks, relative to their market capitalization.

For definitions of terms in the chart above, please visit the glossary.

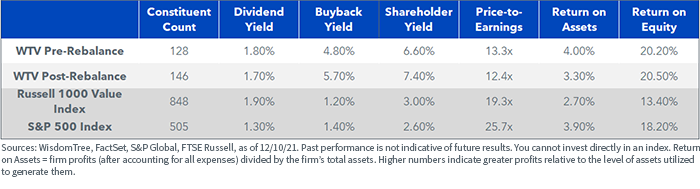

Just prior to the WTV rebrand, the strategy was reconstituted and rebalanced. This process identifies companies generating excess capital and returning it to shareholders, all while exhibiting superior quality characteristics, like high return on equity as well as attractive profit and cash flow margins.

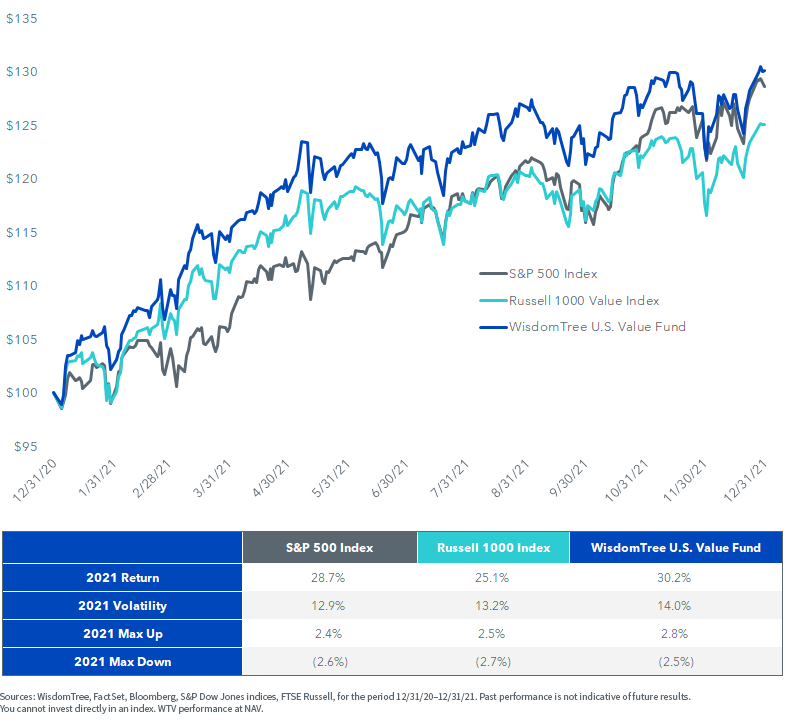

Before we launch into the details of the rebalance, let’s recap WTV’s 2021 performance.

WTV outperformed both the Russell 1000 Value Index and the S&P 500 Index in 2021, returning 30.2% compared to 25.1% (+507 bps) for the Russell 1000 Value and 28.7% (+151 bps) for the S&P 500.

Relative to the value benchmark, WTV’s up capture was 106%, while its down capture was 100%. This indicates that WTV outperformed the Russell 1000 Value during periods of positive performance and performed in line with the benchmark during negative periods.

2021 Performance–Growth of $100

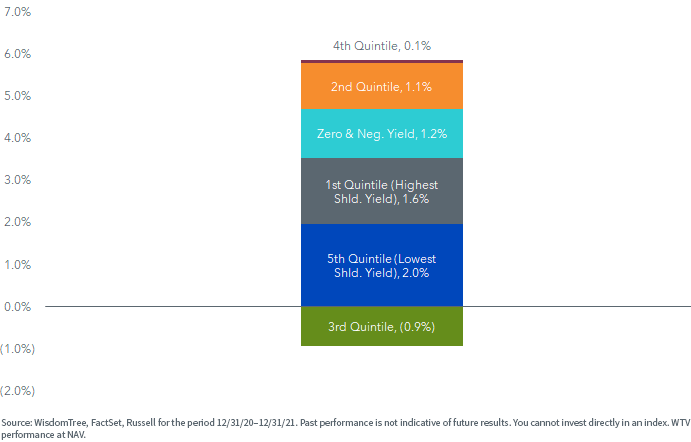

As intended by the strategy’s mandate, the majority of WTV’s outperformance was driven by having an overweight allocation to the highest shareholder yield companies and underweight allocation to the low shareholder yield and negative yielding companies.

As intended by the strategy’s mandate, the majority of WTV’s outperformance was driven by having an overweight allocation to the highest shareholder yield companies and underweight allocation to the low shareholder yield and negative yielding companies.

2021 Performance Attribution vs. Russell 1000 Value Index

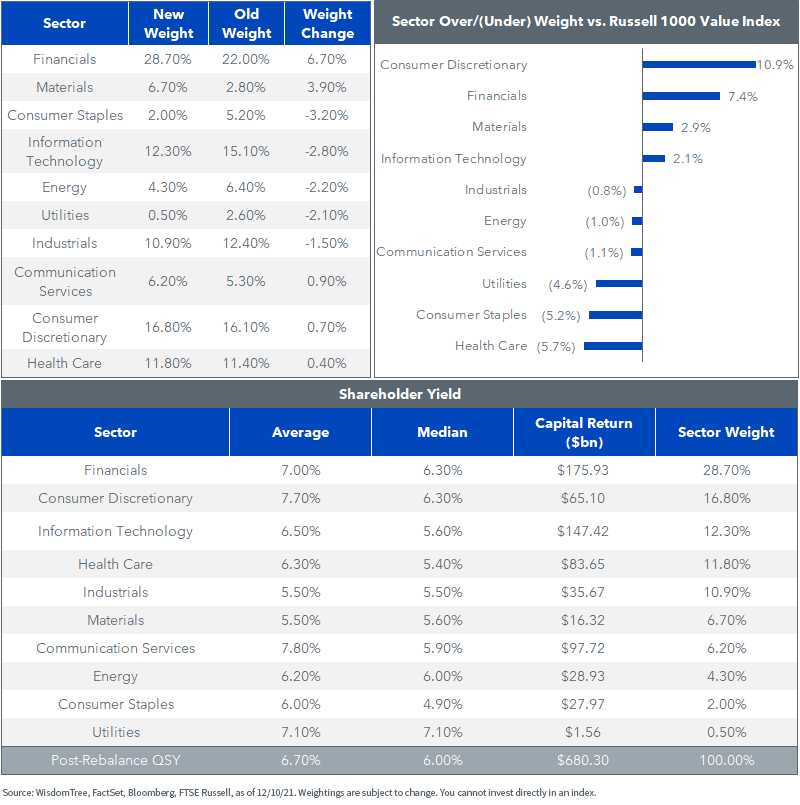

The WTV Rebalance Results

According to S&P Global, 2021 is expected to be a record year for share repurchases within the S&P 500 Index. Q3 2021 buybacks were $235 billion, surpassing the prior quarterly record of $223 billion. Similarly, dividends are also expected to reach a new annual high in 2021.1

Such a high capital return environment provides an interesting backdrop for a shareholder yield-focused strategy like WTV.

By design, the rebalance process increased the aggregate shareholder yield characteristics of the Fund while maintaining key quality metrics. With a shareholder yield of 7.4%, WTV is valued very attractively relative to both the Russell 1000 Value and S&P 500 indexes, both below 3%. Notably, the strategy’s price-to-earnings ratio of 12.4 times is half that of the S&P 500 Index and about 7 times cheaper than the Russell 1000 Value Index.

In terms of sector changes and exposure, WTV remains tilted toward Financials and Consumer Discretionary stocks, which currently offer higher shareholder yields on average. This subset includes names like Voya and AutoNation, both of which have returned over $1 billion in capital to shareholders over the trailing 12 months and boast a consistent history of large share repurchases.2

Interestingly, both WTV and the Russell 1000 Value Index have Health Care exposure within 80 bps of their historical peaks. Companies like DaVita, Cigna, and Quest Diagnostics have shareholder yields above 11% and have reduced their share counts by 8%–11% over the trailing 12 months.3

New Year, New Look, Same High Shareholder Yield Strategy with a Quality Tilt

WTV is a quantitative active strategy that combines a methodical approach to ranking stocks according to their shareholder yield and quality scores, with the added ability to apply discretion where risks or opportunities to the quantitative model are present.

At WisdomTree, we believe companies returning the most capital through dividends and buybacks can create value for shareholders in the form of excess returns.

We believe today’s case for WTV is three-pronged and compelling—WTV offers investors the potential for 1) higher quality and 2) higher capital return, at a 3) discounted valuation relative to benchmark indexes.

1 https://www.prnewswire.com/news-releases/sp-500-buybacks-set-a-record-high-301449031.html

2 Sources: WisdomTree, FactSet, Bloomberg, as of 12/10/21. As of 12/10/21, WTV held AutoNation and Voya at 1.1% and 0.8% weights, respectively.

3 Sources: WisdomTree, FactSet, Bloomberg, as of 12/10/21. As of 12/10/21, WTV held Cigna, DaVita and Quest at 1.1%, 1.3% and 0.7% weights, respectively.

Important Risks Related to this Article

For a prospectus, click here.

Performance is historical and does not guarantee future results. Current performance may be lower or higher than quoted. Investment returns and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. For the most recent standardized performance, 30-day SEC yield and month-end performance click here.

WisdomTree shares are bought and sold at market price (not NAV) and are not individually redeemed from the Fund. Total returns are calculated using the daily 4:00 p.m. EST net asset value (NAV). Market price returns reflect the midpoint of the bid/ask spread as of the close of trading on the exchange where Fund shares are listed. Market price returns do not represent the returns you would receive if you traded shares at other times.

There are risks associated with investing, including the possible loss of principal. Funds focusing their investments on certain sectors increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. While the Fund is actively managed, the Fund’s investment process is expected to be heavily dependent on quantitative models and the models may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

References to specific securities and their issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

U.S. investors only: Click here to obtain a WisdomTree ETF prospectus which contains investment objectives, risks, charges, expenses, and other information; read and consider carefully before investing.

There are risks involved with investing, including possible loss of principal. Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, currency, fixed income and alternative investments include additional risks. Please see prospectus for discussion of risks.

Past performance is not indicative of future results. This material contains the opinions of the author, which are subject to change, and should not to be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. There is no guarantee that any strategies discussed will work under all market conditions. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein. Neither WisdomTree nor its affiliates, nor Foreside Fund Services, LLC, or its affiliates provide tax or legal advice. Investors seeking tax or legal advice should consult their tax or legal advisor. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates.

The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or component of any financial instruments or products or indexes. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each entity involved in compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties. With respect to this information, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including loss profits) or any other damages (www.msci.com)

Jonathan Steinberg, Jeremy Schwartz, Rick Harper, Christopher Gannatti, Bradley Krom, Tripp Zimmerman, Michael Barrer, Anita Rausch, Kevin Flanagan, Brendan Loftus, Joseph Tenaglia, Jeff Weniger, Matt Wagner, Alejandro Saltiel, Ryan Krystopowicz, Kara Marciscano, Jianing Wu and Brian Manby are registered representatives of Foreside Fund Services, LLC.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S. only.

You cannot invest directly in an index.