By Behnood Noei, CFA

Key Takeaways

- Since its November 2024 rebalance, the WisdomTree U.S. High Yield Corporate Bond Fund (QHY) has outperformed its prior version by 37 basis points, driven by a strategic blend of equity momentum and free cash flow insights.

- By cutting exposure to weak-momentum names like Kohl’s and retaining high-momentum issuers with negative cash flow such as Carnival and Delta, the strategy sidestepped downside while capturing upside recovery signals.

- The updated strategy has outpaced the Bloomberg U.S. Corporate High Yield Index by 63 basis points year-to-date, highlighting the value of a disciplined, quality-first approach in volatile markets.

When markets feel shaky, investors naturally look for strategies built on stability and quality. Building on our last post, “Built for the Tough Times: QHY’s Edge in Today’s High-Yield Market,” we’re excited to share an update on the WisdomTree U.S. High Yield Corporate Bond Fund (QHY). In the sections that follow, we’ll remind the readers of the enhancements we’ve made, explain why they matter and show how they’ve helped us deliver stronger results.

Strategic Enhancements for a Resilient Approach

In the wake of COVID-19, many weaker companies stayed afloat thanks to support from the Federal Reserve and other central banks. To keep pace with changing market dynamics and fine-tune our risk/return profile, we added equity return momentum to our tool kit alongside our long-term free cash flow signals. Rolled out in our November 2024 rebalance, this new layer gives us a more timely read on an issuer’s financial health—helping us spot and sideline potential troublemakers before their fundamental weaknesses even register.

Momentum has long been a go-to tool in equity markets for spotting turning points and riding out volatility. We zeroed in on equity momentum, rather than debt momentum, because it cuts through the noise and gives us a clearer read on how the market feels about a company. In our backtests from 2016 through mid-2024, the issuers in the top momentum quintile (and especially those in the top 10%) consistently exhibited strong risk-adjusted results, proving that momentum can be a powerful complement to our fundamentals.

We balance momentum’s benefits against turnover by zeroing in on the most extreme signals—only issuers in the top or bottom 10% of equity momentum ratings make the cut. That way, momentum serves as a powerful reality check on our fundamentals:

- Strong momentum, weak cash flow: If a company is burning cash but its stock shows real momentum, the market may be pricing in a turnaround, and that’s a green light to stay invested.

- Strong cash flow, weak momentum: On the flip side, a company with healthy cash generation but cratering equity momentum can be a warning sign. In those cases, we’ll step aside before sentiment turns into fundamental pain.

One of the most important tweaks we made was knowing when to dial back the momentum signal. By tracking 12-month momentum, we stay grounded in longer-term trends and avoid overreacting to every short-lived swing.

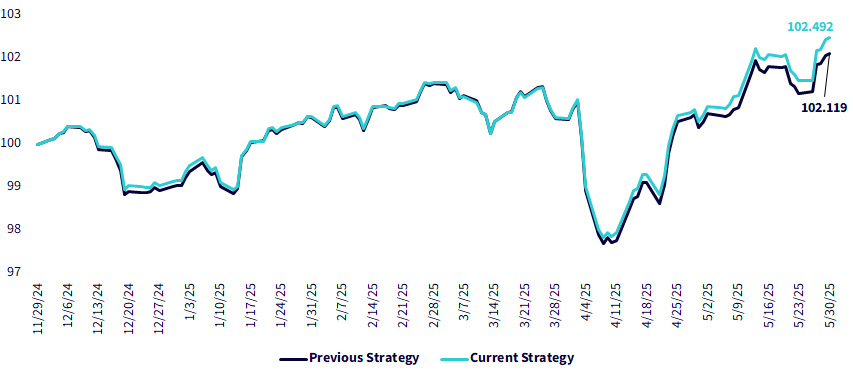

Outperformance in Action: New Strategy vs. Old

Our blend of deep fundamental research and well-timed momentum signals is proving its worth. Since our November 2024 rebalance, the enhanced high-yield strategy, the “Current Strategy,” has outperformed the previous version by 37 basis points.

Growth of $100

Source: WisdomTree, as of 05/30/25. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performances, click here.

A couple of factors have underpinned the strategy’s improved results:

- Timely removal of low-momentum issuers: Exposure to companies such as Kohl’s, Cleveland-Cliffs, B&G Foods and Organon & Co. was eliminated as soon as their equity momentum deteriorated, effectively mitigating potential downside.

- Selective retention of high-momentum, negative-cash-flow issuers: Positions in issuers like Carnival, Royal Caribbean, Fortress Transportation, United Airlines and Delta Air Lines were maintained despite negative free cash flow, since their strong equity momentum signaled anticipated market recoveries.

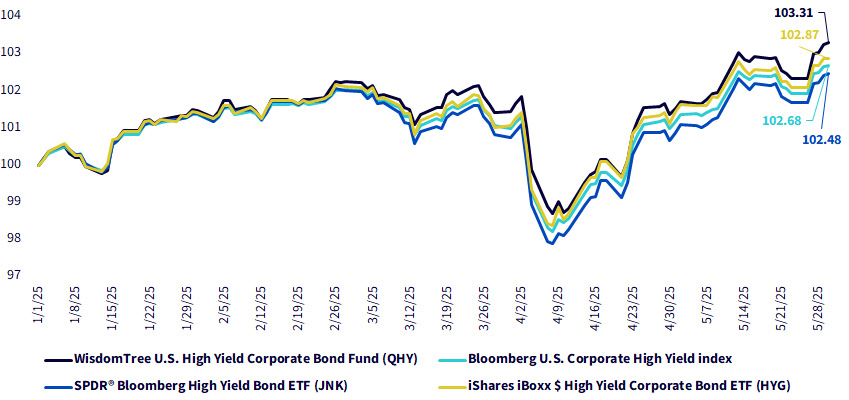

Benchmarking Success: Outperforming Peers in a Time of Distress

Our improved strategy hasn’t just outpaced the previous approach; it’s also held its own against peers and the broader market. Year-to-date, the Fund has beaten the Bloomberg U.S. Corporate High Yield Index by 63 basis points. We believe our emphasis on higher-quality bonds as well as more timely signals, both versus peers and the broader index, have been a major driver of the outperformance.

Growth of $100

Source: Bloomberg, WisdomTree, as of 05/30/25. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click the respective ticker: QHY, JNK, HYG.

Conclusion: Quality and Resilience in Volatile Markets

When markets become stressful, it’s the weaker issuers that usually suffer the most. By keeping quality at the forefront, and layering in timely equity momentum signals, we’ve been able to steer through recent ups and downs with greater confidence. Shifting toward higher-quality issuers and using momentum as an early warning system has helped QHY deliver stronger risk-adjusted returns.

For investors who want exposure to high yield without reaching for riskier credits, a disciplined, quality-first approach like QHY can offer a steadier path. We believe the recent changes to the strategy will leave us better positioned for whatever lies ahead. And ready to pursue strong, risk-adjusted performance in any market environment.

Additional Information

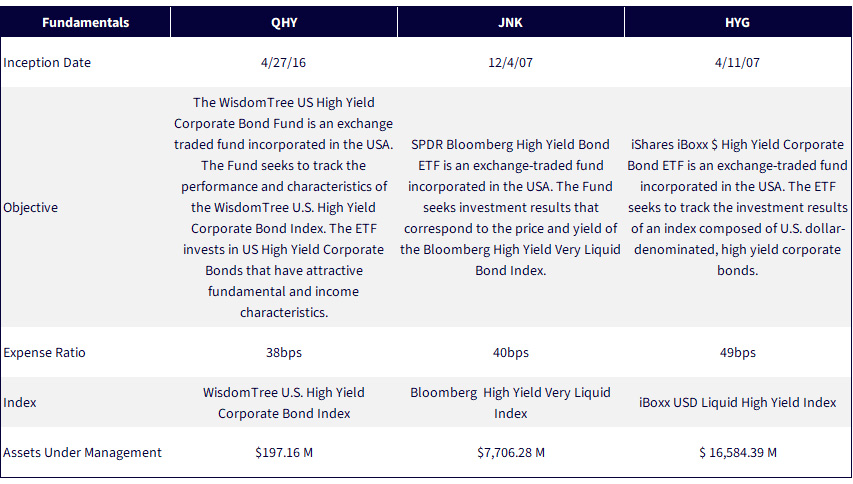

Sources: WisdomTree, State Street, iShares, as of 6/20/25.

This article originally appeared on WisdomTree’s website and is reprinted on VettaFi | ETF Trends with permission from the author. For more information, please visit WisdomTree.com.

For more news, information, and strategy, visit the Modern Alpha Channel.

Disclosure Information

U.S. investors only: Click here to obtain a WisdomTree ETF prospectus which contains investment objectives, risks, charges, expenses, and other information; read and consider carefully before investing.

There are risks involved with investing, including possible loss of principal. Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, currency, fixed income and alternative investments include additional risks. Please see prospectus for discussion of risks.

Past performance is not indicative of future results. This material contains the opinions of the author, which are subject to change, and should not to be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. There is no guarantee that any strategies discussed will work under all market conditions. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein. Neither WisdomTree nor its affiliates, nor Foreside Fund Services, LLC, or its affiliates provide tax or legal advice. Investors seeking tax or legal advice should consult their tax or legal advisor. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates.

The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or component of any financial instruments or products or indexes. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each entity involved in compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties. With respect to this information, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including loss profits) or any other damages (www.msci.com)

Jonathan Steinberg, Jeremy Schwartz, Rick Harper, Christopher Gannatti, Bradley Krom, Kevin Flanagan, Brendan Loftus, Joseph Tenaglia, Jeff Weniger, Matt Wagner, Alejandro Saltiel, Ryan Krystopowicz, Brian Manby, and Scott Welch are registered representatives of Foreside Fund Services, LLC.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S. only.

You cannot invest directly in an index.