By Kevin Flanagan, Head of Fixed Income Strategy

Key Takeaways

- July’s sharply revised jobs report, with payrolls averaging just +35k over three months, has significantly softened the labor market backdrop and opened the door for a potential September Fed rate cut.

- Despite Powell’s recent hawkish tone, Treasury yields dropped notably as markets quickly repriced expectations, highlighting the heightened sensitivity to labor and inflation data ahead of Jackson Hole.

- Fixed income investors may benefit from positioning in short-duration strategies like SHAG or USSH, which are likely to outperform if the Fed pivots to rate cuts later this year.

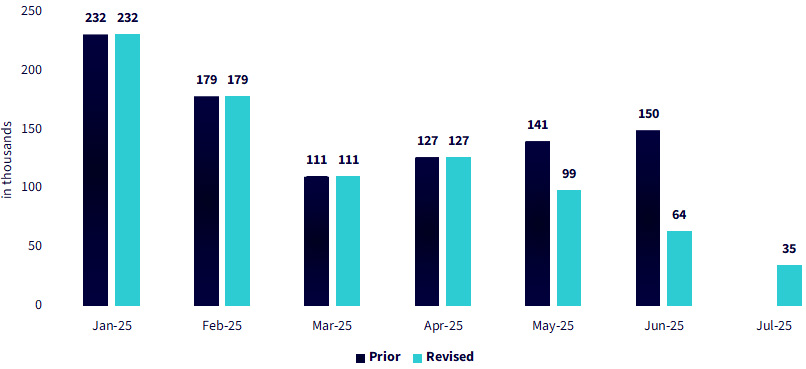

The busy week for the markets last week culminated in the July Employment Situation report. With the jobs data coming after the July FOMC meeting, investors were greeted with a dynamic that is somewhat unusual. With the July jobs data now in, the markets are faced with a visibly different labor market backdrop than what existed at 8:29 Friday morning prior to the release, i.e., much softer than previously thought over the last three months (see below).

Figure 1: U.S. Total Nonfarm Payrolls—Three-Month Moving Average

Source: Bureau of Labor Statistics, as of 8/1/25.

Here are some takeaways:

- Total nonfarm payrolls rose by +73k, visibly below the consensus estimate of +104k

- However, the bigger news is the fact that the prior two months were revised down by a combined -258k, the largest non-Covid related downward revision since 1979. As a result, the three-month moving average for payrolls plummeted to only +35,000 in July

- Powell’s new favorite indicator, the unemployment rate, ticked up by +0.1 pp to a still low 4.2%, in line with expectations

- While we still have another employment report and two more months’ worth of inflation data before the September FOMC meeting, today’s jobs report changes the labor market backdrop Powell has been basing his policy decisions on. Jackson Hole, later this month, provides the opportunity to change forward guidance for Powell

- On its own, this jobs report puts a September rate cut in play

- What happens if upcoming inflation reports are elevated and show more tariff pass-through effects? That’s the potential conundrum

- Needless to say, the Treasury market rallied, with the 2-Year & 10-Year yields falling more than -20 basis points (bps) and -10 bps, respectively on ‘Fed re-pricing’ following Powell’s ‘somewhat hawkish’ FOMC presser last week

- However, a further rally, especially for the 10-Year, is dependent upon upcoming inflation data, such as the CPI report on August 12

Conclusion

Against this shifting labor market, and potential Fed monetary policy backdrop, how should fixed income investors position their bond portfolio? If the Fed does shift into “rate-cut” mode, the front-end of the yield curve, or short-duration strategies, would be expected to outperform. I suggest investors consider either the WisdomTree Yield Enhanced U.S. Short-Term Aggregate Bond Fund (SHAG) or, for a Treasuries-only solution, the WisdomTree 1-3 Year Laddered Treasury Fund (USSH) from our fixed income suite.

This article originally appeared on WisdomTree’s website and is reprinted on VettaFi | ETF Trends with permission from the author. For more information, please visit WisdomTree.com.

For more news, information, and strategy, visit the Modern Alpha Content Hub.

Important Risks Related to this Article

There are risks associated with investing, including possible loss of principal. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

SHAG: Fixed income investments are subject to interest rate risk; their value will normally decline as interest rates rise. Fixed income investments are also subject to credit risk, the risk that the issuer of a bond will fail to pay interest and principal in a timely manner, or that negative perceptions of the issuer’s ability to make such payments will cause the price of that bond to decline. Investing in mortgage- and asset-backed securities involves interest rate, credit, valuation, extension and liquidity risks and the risk that payments on the underlying assets are delayed, prepaid, subordinated or defaulted on. Due to the investment strategy of the Fund, it may make higher capital gain distributions than other ETFs.

USSH: Because the Fund is new, it has no performance history. U.S. Treasury obligations may provide relatively lower returns than those of other securities. Changes to the financial condition or credit rating of the U.S. government may cause the value to decline. Fixed income securities are subject to interest rate, credit, inflation, and reinvestment risks. Generally, as interest rates rise, the value of fixed-income securities falls. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

U.S. investors only: Click here to obtain a WisdomTree ETF prospectus which contains investment objectives, risks, charges, expenses, and other information; read and consider carefully before investing.

There are risks involved with investing, including possible loss of principal. Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, currency, fixed income and alternative investments include additional risks. Please see prospectus for discussion of risks.

Past performance is not indicative of future results. This material contains the opinions of the author, which are subject to change, and should not to be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. There is no guarantee that any strategies discussed will work under all market conditions. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein. Neither WisdomTree nor its affiliates, nor Foreside Fund Services, LLC, or its affiliates provide tax or legal advice. Investors seeking tax or legal advice should consult their tax or legal advisor. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates.

The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or component of any financial instruments or products or indexes. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each entity involved in compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties. With respect to this information, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including loss profits) or any other damages (www.msci.com)

Jonathan Steinberg, Jeremy Schwartz, Rick Harper, Christopher Gannatti, Bradley Krom, Kevin Flanagan, Brendan Loftus, Joseph Tenaglia, Jeff Weniger, Matt Wagner, Alejandro Saltiel, Ryan Krystopowicz, Brian Manby, and Scott Welch are registered representatives of Foreside Fund Services, LLC.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S. only.

You cannot invest directly in an index.