By Kevin Flanagan

Key Takeaways

- The Federal Reserve kept rates unchanged at the January Federal Open Market Committee (FOMC) meeting, maintaining a 4.25%–4.50% range as it reassesses the economic landscape and recalibrates policy to a potentially higher “neutral” rate estimate.

- With the Fed signaling a more cautious stance, Treasury yields are expected to remain elevated, particularly for intermediate and long-term maturities, which could face upward pressure.

- The Fed’s expected shift to a more measured easing path, coupled with ongoing adjustments to its quantitative tightening policy, reinforces the need for careful fixed income positioning.

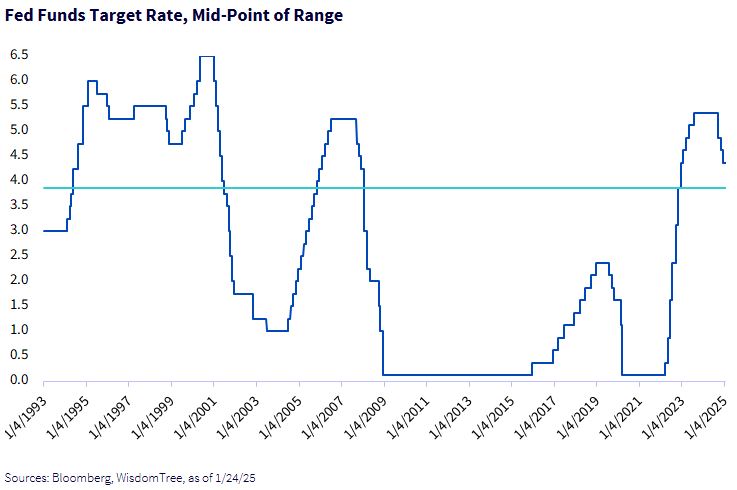

For the first time since the Fed began cutting rates at their September FOMC meeting, the voting members decided to keep rates unchanged to begin 2025. As a result, the Fed Funds trading range remains at 4.25%–4.50%. This level for overnight money is still 100 basis points (bps) below where Fed Funds were trading prior to the beginning of last autumn’s rate-cutting process, so sitting back and taking stock of the economic and inflation landscape does make sense. The question is whether or not this is the pause that refreshes and leads to future rate cuts later this year

One important aspect that comes to mind is the notable difference in the narrative that accompanied the January FOMC gathering, compared to back in September. Back then, the widespread belief in the money and bond markets was that economic/inflation conditions would result in an aggressive rate-cutting response from the Fed. While the aforementioned 100 bps decline in Fed Funds in just a three-month timeframe may have fit the bill, the current macroeconomic outlook is one where the Fed does not need to act with any further urgency at this time. Indeed, as of this writing, Fed Funds Futures are pointing to a year-end target of about 3.90%. This is not only right around the Fed’s own dot plot, but it is also more than 100 bps higher than where expectations were four short months ago. Speaking of 100-bps increases, that’s also what has happened to the Treasury 10-Year yield during this same period.

The more pertinent question is, where do Powell & Co. go from here? The Fed chair has reiterated that policy has been “recalibrated,” with the goal of becoming less restrictive and moving the Fed Funds target down to neutral territory, data permitting. That’s where the uncertainty comes in. What is a neutral Fed Funds Rate? In our opinion, the level is now higher than previous Fed estimates had been showing, and it could be in the 3.5%–4.0% area. The policy makers seem to think the neutral rate has risen as well, but what the Fed decides is the appropriate level may be a moving target in the months ahead.

Using the above graph, if the voting members follow through on bringing the Fed Funds target down to a neutral reading of, say, 3.875% (a level between 3.5% and 4% and similar to the Fed’s median estimate for 2025) and stop easing there, that would mean there could potentially be only a couple of rate cuts for 2025.

One other policy aspect to be on the lookout for from the Fed is their plan for quantitative tightening (QT). The policy makers have already tapered their pace of balance sheet reduction, so it appears it is now a question of when, not if, to end QT in the months ahead.

The Bottom Line

The updated outlook for both the macro background and rate cuts this year leads us to believe that Treasury yields will remain at “normal” elevated readings. In fact, the path of least resistance for intermediate and longer-dated maturities could actually be skewed more to the upside.

This article originally appeared on WisdomTree’s website and is reprinted on VettaFi | ETF Trends with permission from the author. For more information, please visit WisdomTree.com.

For more news, information, and strategy, visit the Modern Alpha Channel.