Christopher Waller, a member of the Federal Reserve Board of Governors, is supportive of another 0.75% interest rate increase at the July central bank meeting to aggressively fight inflation, reported the Wall Street Journal.

Following the July meeting, the Fed isn’t set to meet again until September. Waller has indicated that a 0.50% rate increase at this meeting would also likely be necessary. According to the Fed Governor, November would be the first time that the central bank could possibly revert to the traditional 0.25% increases, depending on inflation levels.

“Inflation is just too high and doesn’t seem to be coming down,” said Waller during a webinar today. “We need to move to a much more restrictive setting in terms of interest rates and policy, and we need to do that as quickly as possible.”

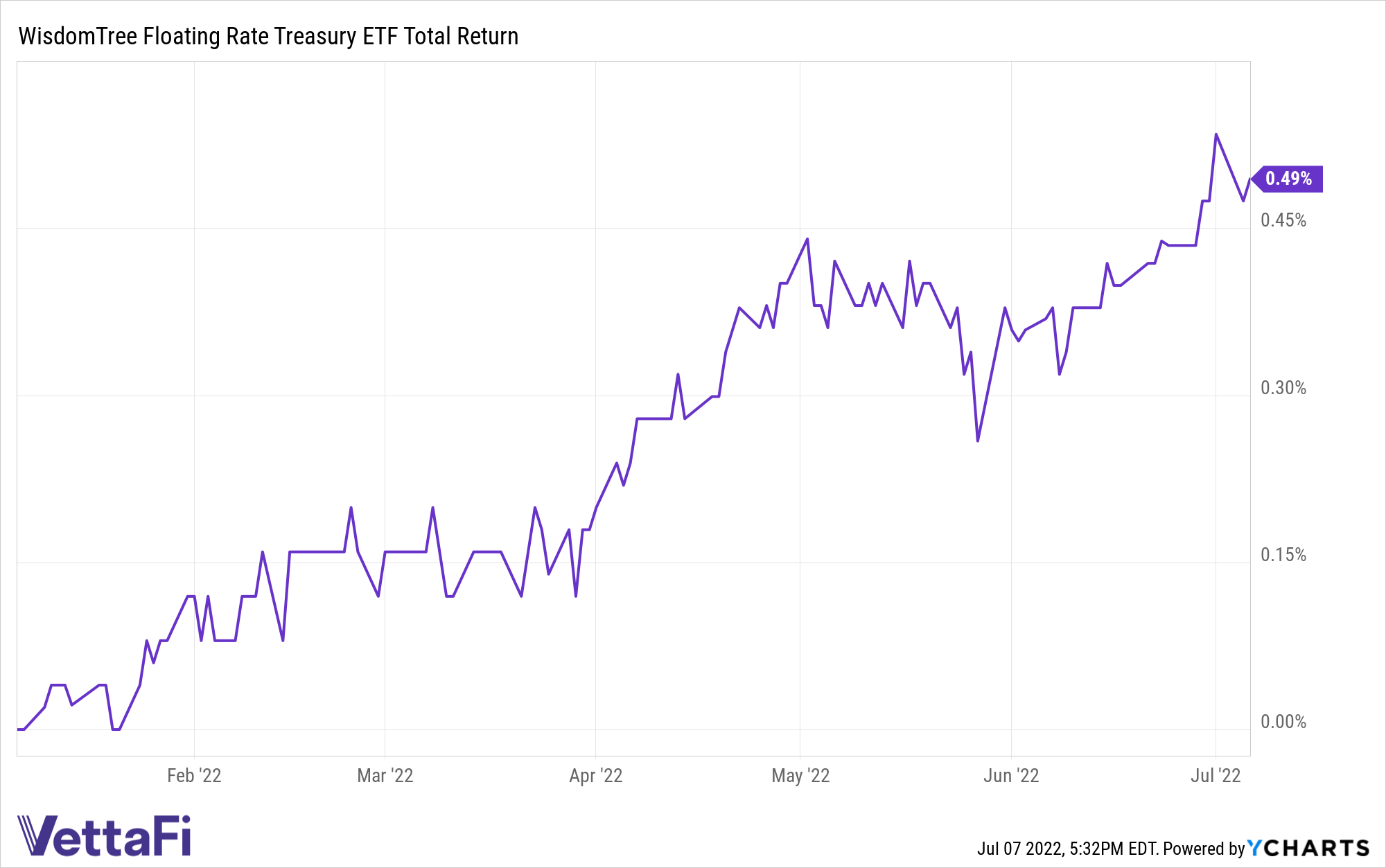

Many advisors and investors are finding themselves trying to predict Fed interest rate hikes to align their portfolios, but the WisdomTree Floating Rate Treasury Fund (USFR) can take the guesswork out of hedging portfolios for interest rate increases.

The fund capitalizes on the use of floating-rate notes by the U.S. Treasury and can be an excellent option for investors looking to limit their amount of credit risk but still capture higher yield potentials in rising rate environments.

WisdomTree believes that floating rate debt is an important bridge between long-maturity, fixed-rate Treasury Bonds and short-maturity Treasury bills. By investing in floating rate Treasuries, holders are paid out quarterly and the amount paid is based on a rate that resets daily in reference to a weekly rate. It can be a good option if Treasury bill yields are rising because it provides the opportunity for greater compensation over a fixed rate bond.

Another benefit to a floating rate is that price volatility can be somewhat lessened by the weekly resets when compared to fixed income bonds. Treasury floating rate notes are a good option when the yield curve is flat or inverted.

USFR seeks to track the Bloomberg U.S. Treasury Floating Rate Bond Index, which measures the performance of floating-rate notes of the U.S. Treasury and contains floating rate notes with two-year maturities and a minimum outstanding amount of $1 billion. The index uses a rules-based strategy and is weighted by market cap. The index excludes fixed-rate securities, Treasury inflation-protected securities, convertible bonds, and bonds with survivor put options.

USFR carries an expense ratio of 0.15%.

For more news, information, and strategy, visit the Modern Alpha Channel.