“Until you make the unconscious conscious, it will direct your life and you will call it fate.“

-Carl Jung

The View from 30,000 feet

Economic reports and corporate data last week highlighted the cautious stance of corporations, contrasted against a resilient consumer, who continues to be propped up by strong demand in the labor market and increasing wages. With 53% of the S&P500 having reported, the message from companies is widely better than expected, as companies have been able to hold onto the topline at the expense of volumes. Market reactions to earnings however are less sanguine, as nervous investors have been quick to punish bad news and less willing to reward good news. The backdrop of high valuations, the availability of a reasonably yielding risk-free rate as an alternative, concerns about a pending debt ceiling crisis and a chorus of data and news stories pointing to the potential of a recession, is keeping positioning bearish and capping attempts for a handoff to positive momentum.

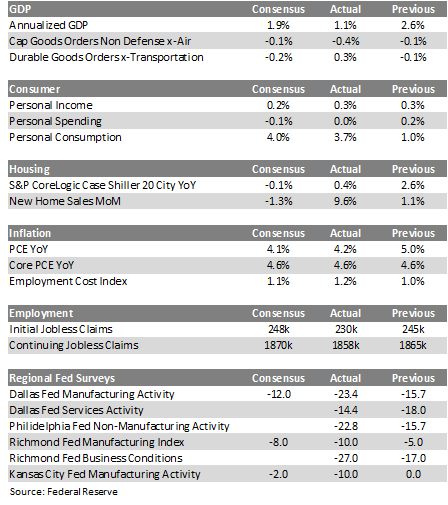

GDP, Fed Regional Survey data and Durable Goods Orders combine to tell the story of tentative corporate spending attitudes.

Earnings are better than expected with companies holding onto topline revenue forecasts utilizing price increases to drive strength against lower volumes and providing hints of optimism about the remainder of 2023.

PCE and ECI reports less than stellar, and reminders from outside the U.S. that the path to disinflation is a circuitous route filled with surprises and setbacks.

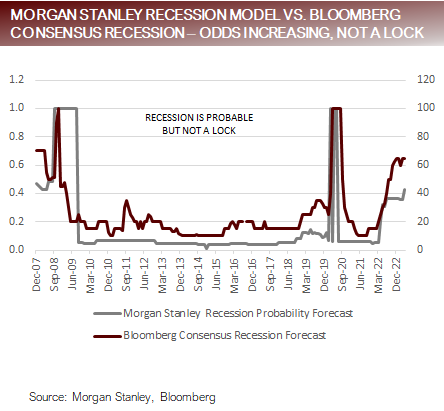

The most Frequently Asked Question from client’s this week: Is a recession inevitable?

GDP, Fed Regional Survey data and Durable Goods Orders, tell a story

- GDP

- The economy losing momentum but remains resilient despite the restrictive interest rate environment and credit tightening.

- Inventories grew 9b in Q422 and contracted $155.0b in Q123, wiping out over 2% from GDP, suggesting disappointing GDP was a result of conservative/nervous management destocking.

- Consumer

- Consumers are benefiting from strong labor market and continued wage inflation, which serves to prop up spending.

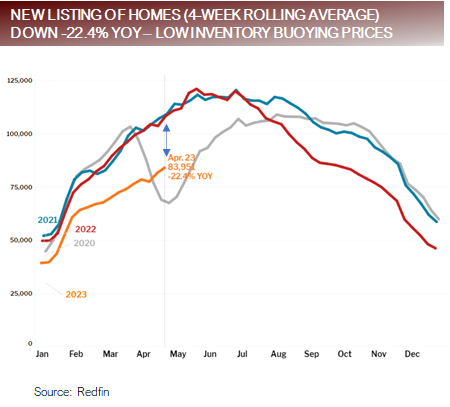

- Housing Market

- Falling mortgage rates and low housing inventories are creating an environment where housing prices can nudge higher.

- Employment

- Recent labor market weakness paused last week, as Unemployment Claims

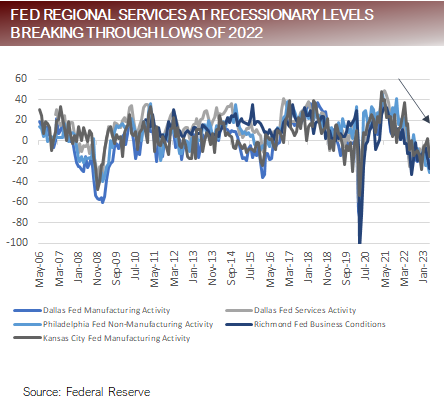

- Regional Fed Surveys

- In one word – dismal. Regional Fed surveys of business conditions, resumed their downward trend, taking out 2022 lows.

- Bottom Line

- Businesses are nervous and cutting back on spending, destocking inventories, and slashing capex, but no one told consumers who continue to benefit from wage inflation, job avvailabilirty and pandemic savings.

Regional Fed surveys stuck at recessionary levels, housing driven strength driven by low supply

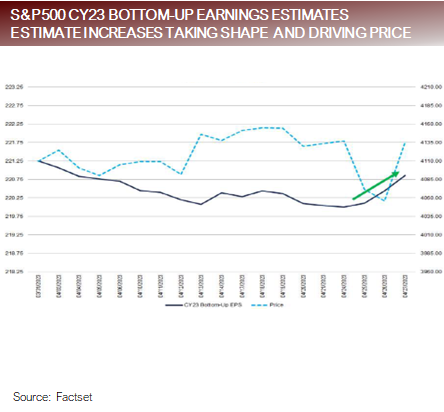

Earnings season – better than expected and increased prices making up for falling volumes

53% of S&P500 companies have reported Q1 earnings, with 79% of companies beating earnings estimates (above the 5- year average of 77% and 10-year average of 73%) and 74% beating revenue estimates (above the 5-year average of 69% and 10-year average of 63%). Companies have on average reported earnings 9% above estimates (below the 5-year average of 8.4% and above the 10-year average of 6.4%)

Q1 earnings are tracking to decline -3.7%, versus expectation at beginning of quarter of -6.7%. Amazon is having an outsized If Amazon were excluded Q1 decline would be -5.1%. Amazon by itself is adding 100 bps to CY2023 earnings for the S&P500.

CY2023 S&P500 earning estimates bucked the downward trend, increasing by 4% over the last week.

Companies that have reported a positive earnings surprise have had their stocks move up an average of +0.1% (two days prior to and two day after earnings report). This is significantly lower than the 5-year average of +1.0%.

Companies that have reported a negative earnings surprise have had their stocks move down and average of -2.4% (two days prior to and two days after earnings report). This slightly lower than the 5-year average of -2.2%.

Bottom Line: Expectations were low for the quarter and companies are beating estimates, particularly on the topline (well ahead of 5 and 10-year averages). Comments from companies, including Procter & Gamble, Coke, Nestle, and Unilever have all indicated that they have been raising prices and accepting lower volumes. However recent data from NielsenIQ shows that Procter & Gamble has begun to discount prices, calling into question the sustainability of never-ending price increases as a viable strategy. Nervous investors have been quick to punish earnings misses but unusually unwilling to chase winners.

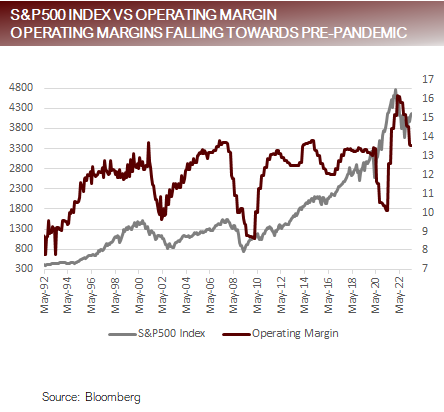

Operating Margins normalizing allowing companies to see the light at end of the tunnel

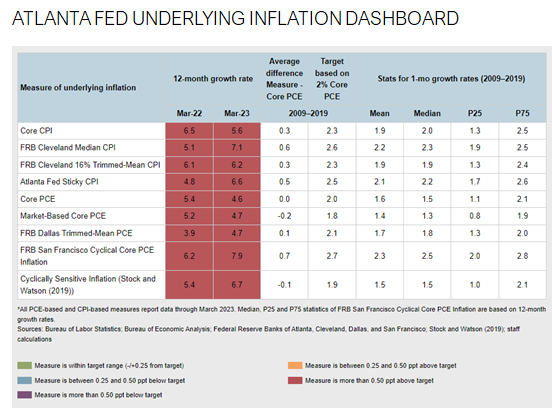

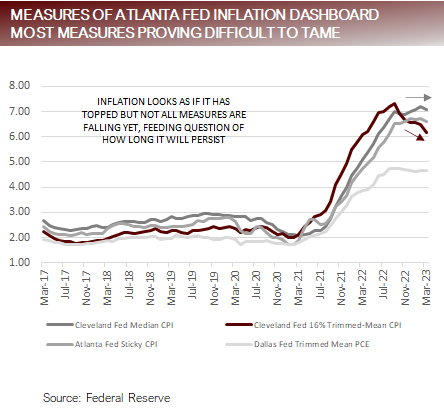

PCE and ECI report less than stellar, and signs that inflation may be surprisingly persistent

The PCE report was above consensus and Core PCE was inline with consensus. Inline to slightly higher inflation readings will not influence the Fed to back away from restrictive policy.

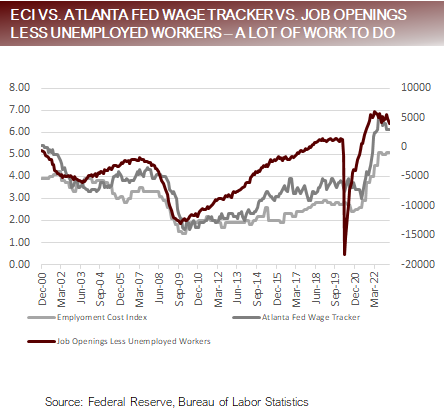

The Employment Cost Index was above consensus as well as above the previous month, indicating the labor market is still operating with an imbalance between supply and demand, pressuring wages higher.

Recent inflation data out of the United Kingdom, Brazil and Sweden have shown the persistence of inflation, suggesting the expectation building for a lengthier battle against inflation that will take a deeper toll on growth.

Brazilian Central bank Governor Roberto Campos Neto ruled out any imminent interest rate cut, speaking at a Senate hearing he said the current rate was appropriate to address inflation While, President Lula, demanded the central bank lower rates to prevent the economy falling into recession. The confrontation highlights potential conflict between central banks and politicians as reset time draws out.

Inflation no longer increasing but how quickly it begins to fall remains uncertain

FAQ: Is a recession inevitable?

Inflation was, and still is, unacceptability high. The solution to high inflation involves slowing aggregate demand to bring in it inline with supply.

In simple terms, the pendulum swung too far towards high growth and inflation (propelled by a decade of easy money, combined with the sudden shock of excess stimulus available from pandemic relief programs), and the Fed is imposing a force to push the pendulum back towards equilibrium. In practice, having the pendulum stop at equilibrium would be a tall order. The nature of a pendulum is that moves back and forth through The best that can be hoped for is a tight range around the equilibrium, but the economy was so far from equilibrium and the force that Fed needed to exert to drive the economy back towards equilibrium is so great, it will be very difficult to stop at equilibrium.

Each week we highlight a seemingly endless series of data points indicating a recession is a high probability. Leading Economic Indicators, Regional Fed Surveys, Yield Curve, … the list goes on, take your pick.

The National Bureau of Economic Research (NBER) is charged with dating the beginning and end of a They look at a handful of measures to make their determination, including real personal income less transfer payments nonfarm payroll employment, employment as measured by the household survey, real personal consumption expenditures, wholesale-retail sales adjusted for price changes (real manufacturing and trade sales) and industrial production. The aggregate of these measures does not currently indicate a recession.

Forecasting economics and the markets is part science and part art. The science side requires a data driven approach and to think in probabilities. The art side requires creativity and humility, and a constant rethinking of assumptions and imagining new realities that call into question historical relationships, interactions of data and evolution of feedback loops.

The bottom line is, nothing is inevitable. As market forecasters, we need to remain disciplined and invest prudently based on probabilities, but we always need to be open creative outcomes where probabilities may not be accurate.

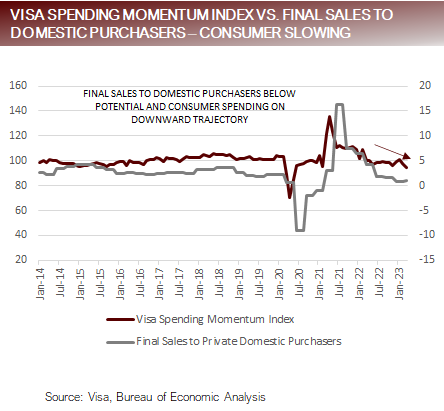

Probability of recession increasing, consumer driven factors of strength fading

Putting it all together

Last week’s corporate and economic data provided a number of insights:

-

- GDP is slowing. The slowdown was driven by nervous management team’s destocking inventory, more than a slowing is underlying demand from the consumer.

- Company earnings are holding up better than anticipated, with the ability to raise prices in order to increase the top line being the key to Q1 success However, there are early signs from Staples that companies are running out of room to raise prices.

- Consumer spending has been the driver of continued strength. There are early warnings signs that the consumer demand is slowing, which at a minimum will make growth harder to come by and will impact Goods before Services.

- Inflation has peaked and is headed lower. The path to lower inflation will not be a straight line and will unfold over a period measured in quarters and years. As long as the Fed is focused on current data rather than forecasting, they will have ammunition to stay hawkish longer than the markets expect.

Signals of a recession abound. What this tells us is that a recession is probable, but it doesn’t tell us when or how deep. It’s also important to keep in mind increased probabilities do not represent guarantees.

Structuring a portfolio in an environment when a recession is probable, depends on risk For investors, where minimizing the risk of a drawdown is important, portfolios should be structured with caution and prudence.

Given that the risk-free rate is providing about two-thirds of the long-term expected return of equities, and the risk-free rate is near the earnings yield of the S&P500, the decision to be cautious and conservatively position in Treasuries is less painful than it had been over the last decade.

Performance data quoted represents past performance, which is not a guarantee of future results. No representation is made that a client will, or is likely to, achieve positive returns, avoid losses, or experience returns similar to those shown or experienced in the past.

Focus Point LMI LLC

For more information, please visit www.focuspointlmi.com or contact us at [email protected] Copyright 2023, Focus Point LMI LLC. All rights reserved.

The text, images and other materials contained or displayed on any Focus Point LMI LLC Inc. product, service, report, e-mail or web site are proprietary to Focus Point LMI LLC Inc. and constitute valuable intellectual property and copyright. No material from any part of any Focus Point LMI LLC Inc. website may be downloaded, transmitted, broadcast, transferred, assigned, reproduced or in any other way used or otherwise disseminated in any form to any person or entity, without the explicit written consent of Focus Point LMI LLC Inc. All unauthorized reproduction or other use of material from Focus Point LMI LLC Inc. shall be deemed willful infringement(s) of Focus Point LMI LLC Inc. copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Focus Point LMI LLC Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Focus Point LMI LLC Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.

All unauthorized use of material shall be deemed willful infringement of Focus Point LMI LLC Inc. copyright and other proprietary and intellectual property rights. While Focus Point LMI LLC will use its reasonable best efforts to provide accurate and informative Information Services to Subscriber, Focus Point LMI LLC but cannot guarantee the accuracy, relevance and/or completeness of the Information Services, or other information used in connection therewith. Focus Point LMI LLC, its affiliates, shareholders, directors, officers, and employees shall have no liability, contingent or otherwise, for any claims or damages arising in connection with (i) the use by Subscriber of the Information Services and/or (ii) any errors, omissions or inaccuracies in the Information Services. The Information Services are provided for the benefit of the Subscriber. It is not to be used or otherwise relied on by any other person. Some of the data contained in this publication may have been obtained from The Federal Reserve, Bloomberg Barclays Indices; Bloomberg Finance L.P.; CBRE Inc.; IHS Markit; MSCI Inc. Neither MSCI Inc. nor any other party involved in or related to compiling, computing or creating the MSCI Inc. data makes any express or implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of such data. Such party, its affiliates and suppliers (“Content Providers”) do not guarantee the accuracy, adequacy, completeness, timeliness or availability of any Content and are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, or for the results obtained from the use of such Content. In no event shall Content Providers be liable for any damages, costs, expenses, legal fees, or losses (including lost income or lost profit and opportunity costs) in connection with any use of the Content. A reference to a particular investment or security, a rating or any observation concerning an investment that is part of the Content is not a recommendation to buy, sell or hold such investment or security, does not address the suitability of an investment or security and should not be relied on as investment advice.

Important Disclosures

This communication reflects our analysts’ current opinions and may be updated as views or information change. Past results do not guarantee future performance. Business and market conditions, laws, regulations, and other factors affecting performance all change over time, which could change the status of the information in this publication. Using any graph, chart, formula, model, or other device to assist in making investment decisions presents many difficulties and their effectiveness has significant limitations, including that prior patterns may not repeat themselves and market participants using such devices can impact the market in a way that changes their effectiveness. Focus Point LMI LLC believes no individual graph, chart, formula, model, or other device should be used as the sole basis for any investment decision. Focus Point LMI LLC or its affiliated companies or their respective shareholders, directors, officers and/or employees, may have long or short positions in the securities discussed herein and may purchase or sell such securities without notice. Neither Focus Point LMI LLC nor the author is rendering investment, tax, or legal advice, nor offering individualized advice tailored to any specific portfolio or to any individual’s particular suitability or needs. Investors should seek professional investment, tax, legal, and accounting advice prior to making investment decisions. Focus Point LMI LLC’s publications do not constitute an offer to sell any security, nor a solicitation of an offer to buy any security. They are designed to provide information, data and analysis believed to be accurate, but they are not guaranteed and are provided “as is” without warranty of any kind, either express or implied.

FOCUS POINT LMI LLC DISCLAIMS ANY AND ALL EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY, SUITABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE.

Focus Point LMI LLC, its affiliates, officers, or employees, and any third-party data provider shall not have any liability for any loss sustained by anyone who has relied on the information contained in any Focus Point LMI LLC publication, and they shall not be liable to any party for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including, without limitation, lost income or lost profits and opportunity costs) in connection with any use of the information or opinions contained Focus Point LMI LLC publications even if advised of the possibility of such damages.