By Lonnie S. Jacobs

Associate Director, Research Content

For the first time since 2002, the euro has traded below parity with the U.S. dollar. While it has rebounded along with other risk assets back above a few times, concerns about the economic impact of the war in Ukraine pushed the euro down to its lowest levels in 20 years.

While euro/dollar parity may have important psychological implications, we know definitively that currency performance can have a significant impact on U.S. investor total returns in foreign markets.

Since the introduction of the euro on January 1, 1999, the currency provided positive returns in 10 out of 23 years (43.47%). Over the same time frame, equities in the region had positive performance in 14 out of 23 years (60.87%). On one hand, equities seem to trend higher over time. On the other, developed market1 currencies can either appreciate or depreciate as they mean-revert toward fair value. Below, we examine four scenarios that try to separate equity risk from currency risk to try to understand which risks may be worth taking.

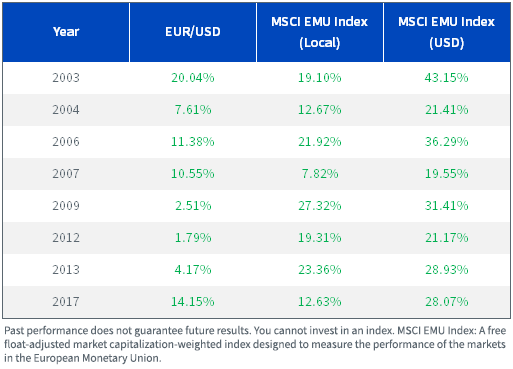

Scenario 1: Positive Calendar Year Returns for MSCI EMU Index and the Euro

When risk has been “on,” the euro and stocks have historically tended to appreciate together. This has had the added benefit of magnifying gains for U.S.-based investors. While the magnitude of gains has also been significantly higher for equities than EUR/USD, four out of eight years saw a double-digit appreciation for the euro. On its face, it seems that if an investor is bullish on European stocks, they should also be bullish on the currency.

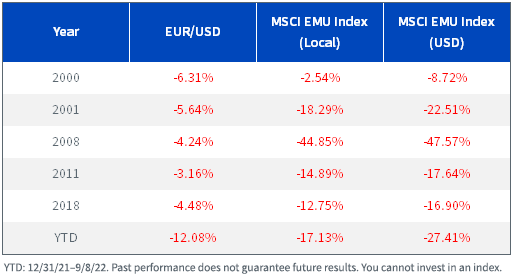

Scenario 2: MSCI EMU Index and EUR down

However, it seems that positive correlation can cut both ways. In years where European equities were down, the euro also tended to be down, thus magnifying losses for U.S. investors. In years with double-digit corrections in equities, the euro depreciated on average by 5.1% per year. During more modest corrections, the euro depreciated by 6.3% per year. In terms of risk management, it seems currency hedging could be one way to potentially dampen drawdowns relative to an unhedged benchmark.

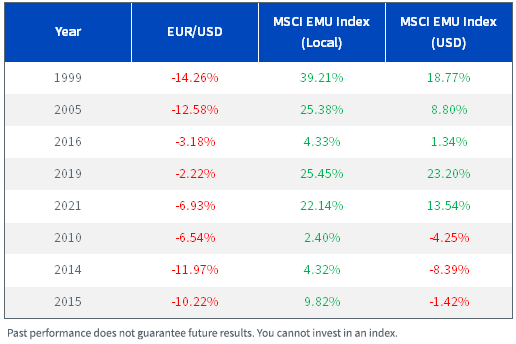

Scenario 3: MSCI EMU Index (Local) Up, EUR Down

In the most classic case for currency hedging foreign equities (years when stocks are up, but currencies are down), we see that at least one-third of the time, currency losses completely outstrip the gains in equities. Put another way, an investor can get the call right on equities, but still end up losing money.

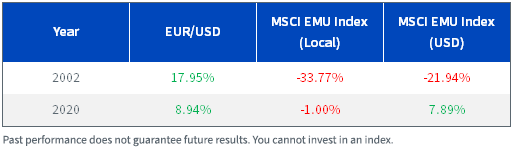

Scenario 4: MSCI EMU Index Down, EUR Up

While anything is possible, when risk has been off, EUR has seldom been a safe haven, with the exception of 2002 and 2020. In these instances, a currency-hedged strategy underperformed in a down market.

FX-Hedged Exposure

For investors who don’t have a view on the direction of the euro or think the dollar will continue to strengthen, a hedged option may be more suitable.

The WisdomTree Europe Hedged Equity Fund (HEDJ), which seeks to track the price and yield performance, before fees and expenses, of the WisdomTree Europe Hedged Equity Index, was launched in 2012 and provides exposure to dividend-paying companies with an exporter tilt in the eurozone. The Fund hedges exposure to fluctuations in the euro by investing in one-month forward currency contracts.

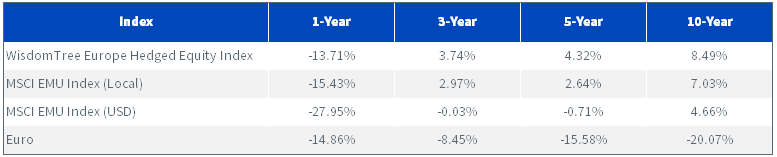

Returns

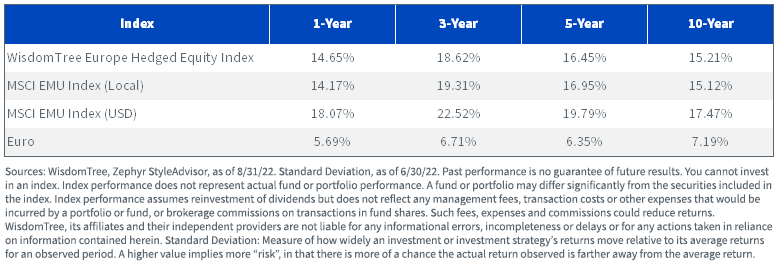

Standard Deviation

Additional Index information is available here.

See the Fund’s page for full performance, risks and other important information.

Currency-hedged strategies aim to isolate returns to stock performance in the local markets, without changes in the local currency. Comparing returns of the MSCI EMU Local index versus the USD version, an outperformance ranging from 175 to 1,017 basis points (bps) can be seen with lower volatility for all standardized periods. An even greater outperformance was generated for the WisdomTree Europe Hedged Equity Index over the same time frame, ranging from 345 to 1305 bps.

1 Past performance is not indicative of future results.

Originally published by WisdomTree on September 15, 2022.

For more news, information, and strategy, visit the Modern Alpha Channel.

Important Risks Related to this Article

There are risks associated with investing, including the possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. Investments in currency involve additional special risks, such as credit risk and interest rate fluctuations. Derivative investments can be volatile and these investments may be less liquid than other securities, and more sensitive to the effect of varied economic conditions. As this Fund can have a high concentration in some issuers, the Fund can be adversely impacted by changes affecting those issuers. Due to the investment strategy of this Fund it may make higher capital gain distributions than other ETFs. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.