Last year was a phenomenal year for most managed futures strategies, and this year as volatility and uncertainty continue regarding Fed rate hikes and potential recession, they’re likely to continue their strong performance. But exactly how much should you allocate to managed futures in your portfolio, and where should that allocation come from?

iM Global Partner, the issuer of one of 2022’s rock star ETFs, the iMGP DBi Managed Futures Strategy ETF (DBMF), broke down how various managed futures allocation levels would likely have performed in a traditional 60/40 portfolio historically to find the optimal level for advisors. In addition, the company also analyzed where the funding for the allocations should optimally come from within a portfolio to give the best overall return.

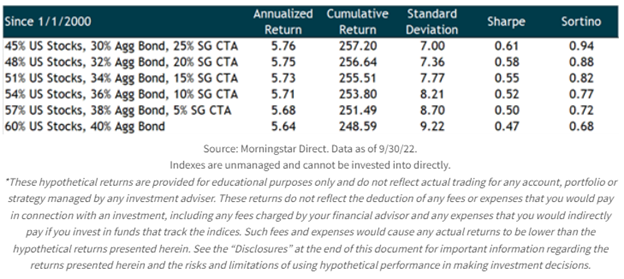

From a statistical standpoint, every additional 5% increment of managed futures added pro rata to a traditional portfolio (up to 25%) increases returns since inception while offering significant reduction of the portfolio’s standard deviation when looking back at a time period between January 1, 2000, and September 30, 2022, (accounting for annual rebalances).

Image source: iMGP Funds

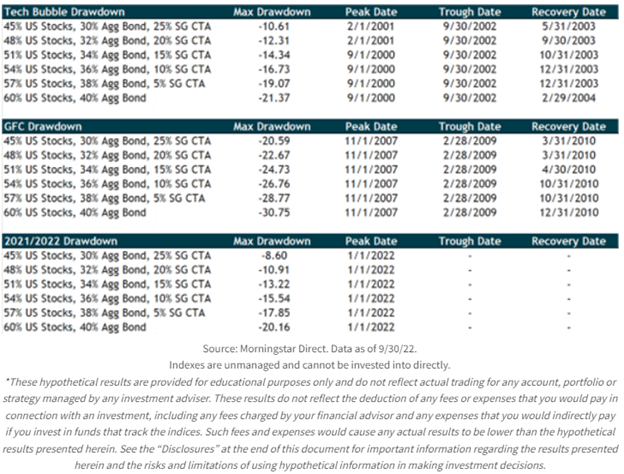

The strategy gets even more impressive when you narrow in on the times of market turbulence and drawdown — specifically the post-tech-bubble bear market in 2000–2002, the global financial crisis bear markets between 2001–2009, and the current bear market.

“Even a small 5% allocation to managed futures would have saved you about 2.3 percentage points of performance this year – from a loss of 20.2% to 17.9%. A ‘bold’ 10% allocation would have come close to cutting losses by a quarter,” reported iMGP.

Image source: iMGP Funds

Portfolio optimizers focused on risk-adjusted returns will generally attempt to allocate up to a full third of a traditional portfolio to managed futures, far more than most advisors and clients are even remotely comfortable with. Given the middling performance of most managed futures strategies during the last decade when traditional equities and bonds outperformed virtually anything else, even a 5%–10% allocation can feel like a hard sell, but it’s a practical allocation sweet spot that can reap multi-faceted rewards for portfolios.

“Why would an optimizer tell you to invest so much in managed futures? Simply put, because the strategy (as measured by the SG CTA Index) has similar long-term returns to a 60/40 portfoli, but with essentially zero long-term correlation to both stocks and bonds: -0.09 correlation to the S&P 500 Index from January 2000 through September 2022, and 0.08 correlation to the Bloomberg Aggregate Bond Index (using monthly returns),” explained iMGP.

How to Fund a Managed Futures Allocation

One of the greatest appeals of managed futures is their lack of correlation to other asset classes, and so funding them pro rata from a current allocation that’s already preset at a client’s risk tolerance and return stream goals is a logical next step. An alternative option is to fund the allocation greater than pro rata from bonds, particularly given that equities outperform bonds over a long enough time period and the strong performance of managed futures strategies during periods of sustained equity weakness.

For larger allocations, it’s important to keep in mind opportunity costs in the long term: “the further one moves away from pro rata funding, the more it becomes an active ‘bet’ against existing asset allocation, and the greater the chance of an extreme outcome that could derail an otherwise successful investment plan,” iMGP explained.

Ultimately, having an allocation percentage to managed futures that you are both comfortable with and can defend confidently to your clients during periods of underperformance is the goal. It’s a strategy that offers long-term, multifaceted benefits to a portfolio, and the goal is almost always to maintain long-term exposures to any asset class when possible.

According to iMGP, “A managed futures allocation should be big enough to move the needle in your portfolio when it’s working, otherwise the inevitable challenging periods along the way will hardly be worth it. But, the allocation can’t be so big that you (or your client) will throw in the towel during rough patches. It can be a tricky needle to thread, but one that we believe is well worth it when considering the long-term benefits to a portfolio.”

The iMGP DBi Managed Futures Strategy ETF (DBMF) allows for the diversification of portfolios across asset classes uncorrelated to traditional equities or bonds. It is an actively managed fund that uses long and short positions within the futures market on several asset classes; domestic equities, fixed income, currencies, and commodities (via its Cayman Islands subsidiary).

The fund’s position is determined by the Dynamic Beta Engine, which analyzes the trailing 60-day performance of CTA hedge funds and then determines a portfolio of liquid contracts that would mimic the hedge funds’ averaged performance (not the positions). The fund has a management fee of 0.85%.

For more news, information, and analysis, visit the Managed Futures Channel.