I recently had the good fortune to sit down with Corey Hoffstein, co-founder and CIO of Newfound Research, to discuss return stacking and return stacking models, a more unique approach to investing in stocks, bonds, and alternatives that can provide more traditional beta-like returns while also generating alpha from managed futures or other alternatives.

Hoffstein explained that return stacking enables a newer take on the kind of investing strategies that institutional investors have been using over the last four decades. It allows investors to capture alpha opportunities without being at the expense of beta allocations.

“The whole core concept was to say ‘we don’t have to make this trade-off of either/or: we can have our beta and have our alternatives and diversifiers as well,’” Hoffstein explained. “None of that was really available to retail investors unless they had margin accounts, which tended to be expensive [due to the margin/cost of borrowing being expensive], or unless they were willing to trade futures, which some are; most aren’t.”

Return stacking allows for a newer take on the traditional 60/40 that seeks to stay invested in the globally diversified risk premium allocations of stocks and bonds that will continue to drive markets over the long-term, but makes space within the portfolio to also allocate for inflation volatility. Something to which the traditional 60/40 portfolio is particularly susceptible.

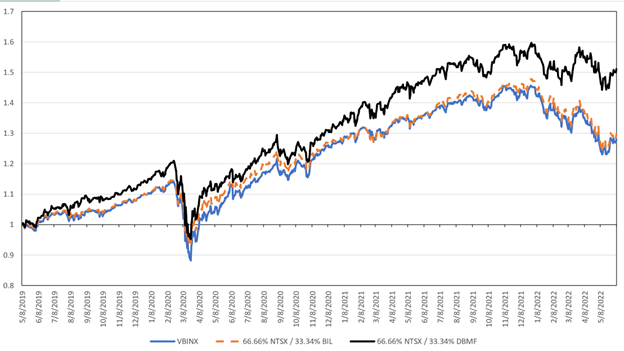

The return stacking concept can be seen as a 60/40/+, wherein a return stacking model the 60/40 is achieved through investment into a fund like the WisdomTree U.S. Efficient Core Fund (NTSX), an ETF that invests in both large-cap U.S. equities as well as U.S. Treasury futures contracts and boosts capital efficiency for a portfolio.

Through the use of a 1.5x leverage by NTSX to provide 60% equity and 40% U.S. Treasuries for the portfolio by allocating 2/3 of the portfolio assets to NTSX, the performance of the NTSX allocation mimics the Vanguard Balanced Index Fund Investor Shares (VBINX), Vanguard’s U.S. 60/40 fund. At the same time, 1/3 of the portfolio’s assets are freed up for alternative allocations, such as managed futures.

Graph courtesy of Corey Hoffstein, dates as of 06/08/22

In the current environment, some advisors might look toward commodities for this remaining allocation, but because of their heavy weighting towards energy and positive return potential that is linked heavily to inflationary periods and little else, Hoffstein doesn’t see them as an ideal option for investors in all environments.

Why Managed Futures and DBMF Work for Return Stacking

The temptation might exist to look at managed futures and the iMGP DBi Managed Futures Strategy ETF (DBMF) as a returns play in a return stacking model that utilizes NTSX and DBMF, given its outperformance this year (the fund’s year-to-date return is currently 30.49% as of 6/14/22 per the website). For Hoffstein, the inclusion of managed futures and DBMF, in particular, is about so much more.

“If you look at managed futures historically, whether you look at just the individual sleeves like a trend on rates, trend on equities, trend on commodities, trend on currencies, what you find is they actually perform well historically in both inflation and deflationary environments,” Hoffstein said.

The great appeal of managed futures funds is their optionality within so many different spaces, including long and short positions in commodities, long/short positions on interest rates, and long/short positions on currencies such as the U.S. dollar. Because of the number of markets managed futures trade in, they can position to respond better to the specific type of inflation that is happening.

DBMF in particular is appealing for a return stacking model because it avoids the dispersion that is common within managed futures hedge fund performance, explained Hoffstein. It does so by seeking to track the averaged performance of existing hedge fund strategies, pulled from 20 of the largest managed futures hedge funds through the performance data of the SocGen CTA Hedge Fund index, thereby eliminating bias and performance outliers that can happen when following just a single issuer strategy.

“What I love about what DBMF is trying to achieve, and has historically achieved, is giving you a highly correlated return stream to the broad index and completely eliminating the underlying fees associated with the hedge funds,” Hoffstein said. “You can really think about capturing the index plus 150 or 200 basis points over time because you’re eliminating so much of that cost.”

Hoffstein likens investing in DBMF as a managed futures option to investing in the S&P 500 as an equities option because of its low cost for the exact kind of exposure desired. It’s a strong core allocation for managed futures and works to fill the inflation volatility gaps that traditional 60/40 portfolios carry.

Newfound Research also utilizes DBMF in some of its portfolio models.

For more news, information, and strategy, visit the Managed Futures Channel.