I’m just going to go out on a limb here and admit something: I don’t get volatility.

I mean, I get the math, and I’ve read the books, but there’s a difference between becoming conversationally fluent in a language and thinking in a language, like, in your dreams. Heinlein brilliantly defined this empathic, internal understanding with the word “grok” in Stranger in a Strange Land.

Recognizing my failure, I’ve spent the better part of 2021 reading, talking, and really trying to “grok” what we mean by “volatility” in markets by reaching out and asking questions of a group of academics and investors often loosely lumped together in a big bucket called “long vol.”

Part 1: A Problem of Definitions

When I started down this rabbit hole, I thought I understood what the word volatility meant, at least. Boy, was I wrong.

Here’s what I do know: in financial markets, we tend to mean one of the following three things when we hear the word “volatility”:

- Realized Volatility — The actual measurement of price movements observed historically.

- Implied Volatility — The volatility, well, implied by options pricing models based on the current clearing price of options.

- The VIX — An algorithmic summation of the implied volatility of a specific set of ever-changing puts and calls, specifically on the S&P 500 Index.

The problem is that all three of these measure very different things, and none of them are particularly useful in assessing what actual investors and advisors care about: the probability of experiencing a “meaningful” decline between now and some point in the future. Let’s step through each in turn.

Realized Volatility

I learned about actual realized volatility in my remedial math class for business school (seriously). To calculate, you take all the observations in your data set (say, daily returns for the S&P 500); run them through your stats platform of choice (MatLab, R, Excel, whatever); and calculate a mean daily return. Then, making the outrageous assumption that our observations should be normally distributed around that mean, you calculate the deviation of each data point from that mean, square it, average them all, slap a square root over that to get “standard deviation.”

Standard deviation is useful because if our data was normal (which, again, it probably isn’t), we can expect that 66% of our outcomes should fall within the mean +/- the standard deviation.

If you’re already losing consciousness, you’re not alone. These details are part of why even smart investment folks get lost in the weeds when it comes to volatility.

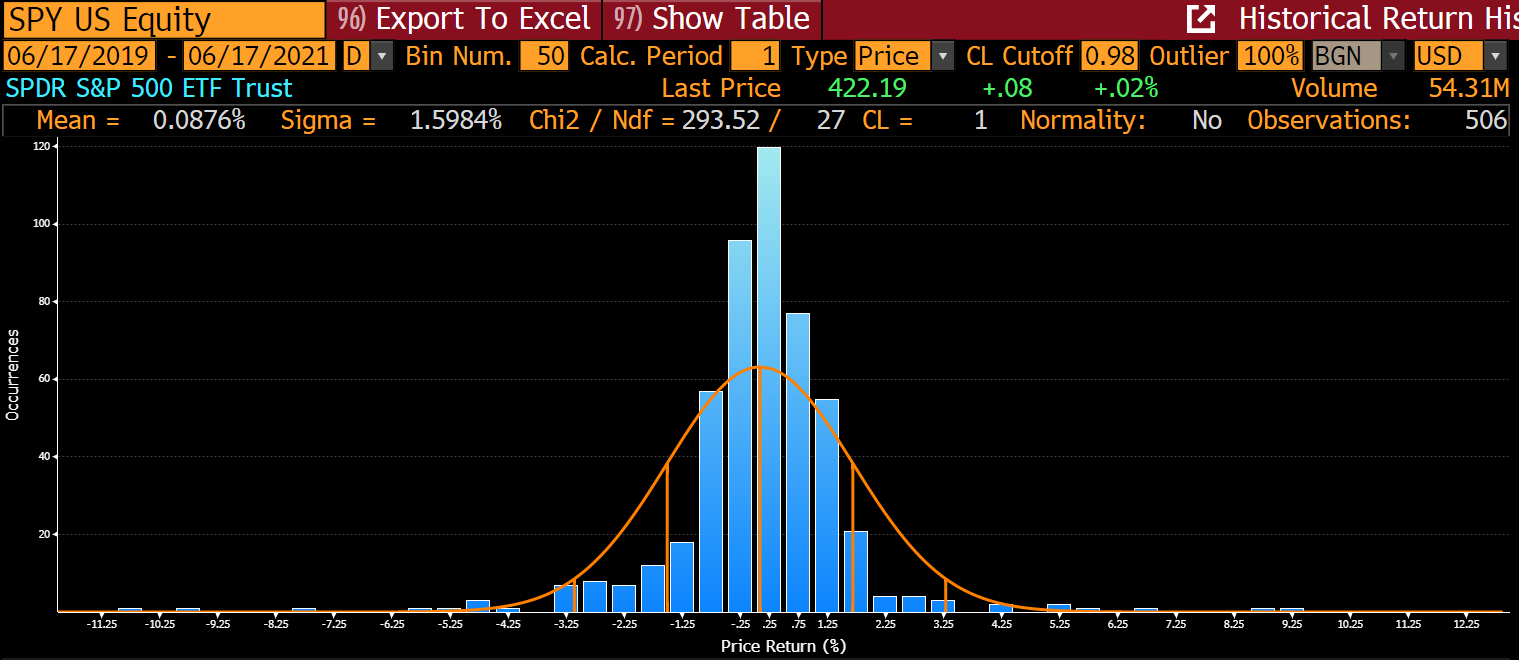

So let’s put it in context. Here’s a histogram of the daily returns of the S&P 500 for the past two years, where each column is the number of trading days in a given bucket of potential outcomes.

Source: Bloomberg. Data from Jun. 17, 2019 – Jun. 17, 2021

Over the past two years, the mean daily return has been a whopping 8 basis points, while the “sigma” (or the Greek symbol for standard deviation) is 1.59%.

That means that about 2/3 of the observed daily S&P 500 returns fall within that +/- range around that 8 basis point mean. The red vertical lines indicate where those brackets fall on the theoretical “bell curve.” You can also see a few days that were +/- 10% or more – big days!

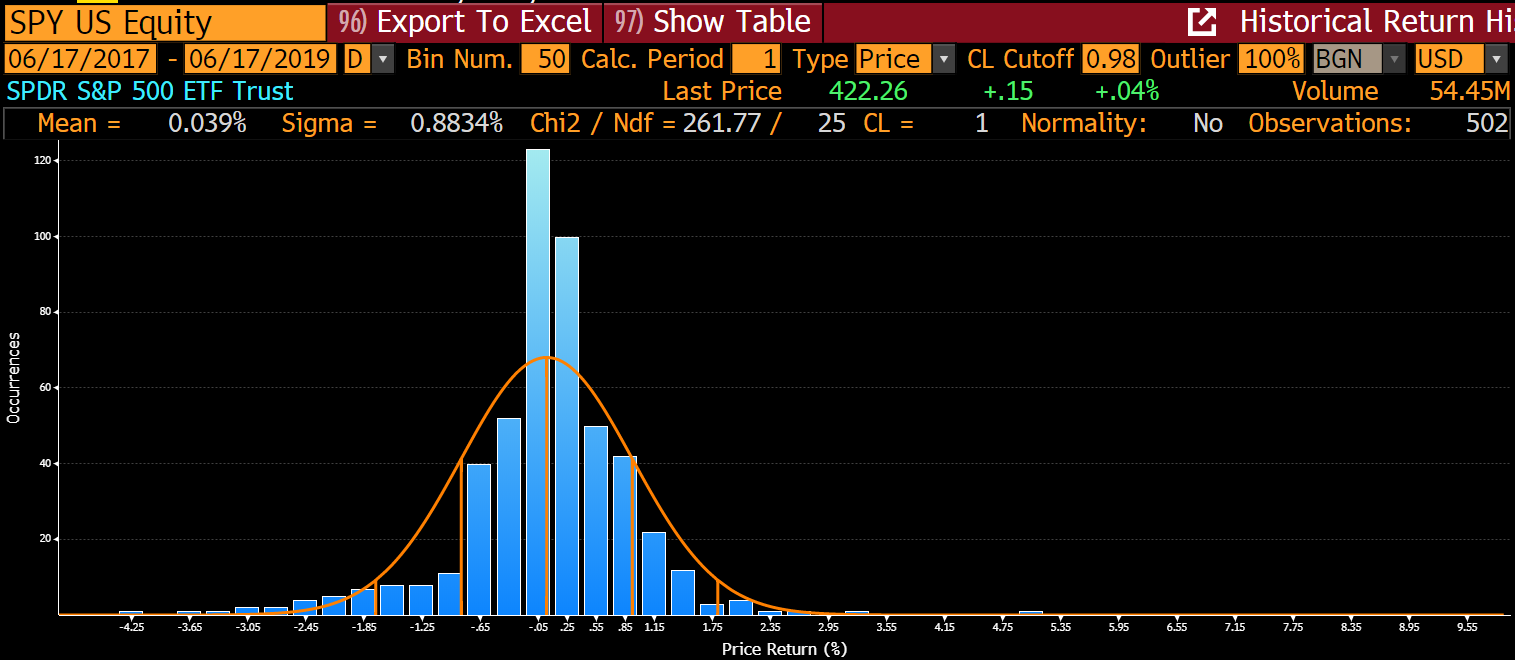

Of course, this doesn’t really tell us anything about what the next two years worth of returns will look like, any more than the previous two years told us about the above:

Source: Bloomberg. Data from Jun. 17, 2017 – Jun. 17, 2019

From June 2017 to June 2019, the mean of S&P 500 returns was quite similar, but the standard deviation back then was about half. So that means today’s market must be twice as volatile as it was back then, right?

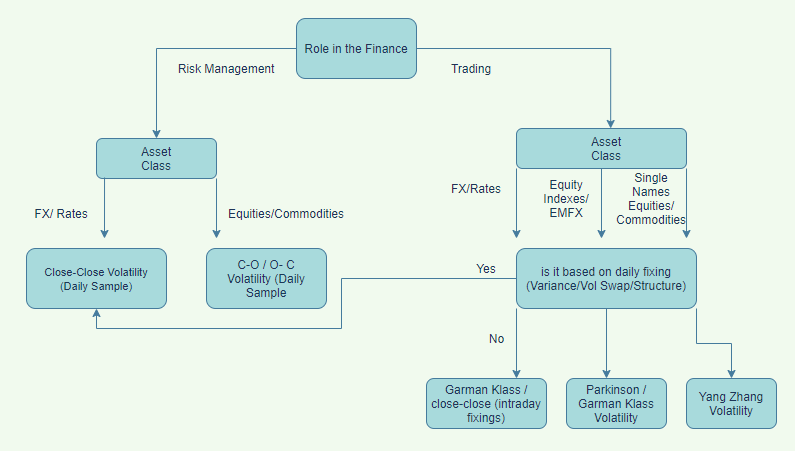

Well… not really. Because all we ever really care about is future volatility. To make matters worse, there are actually half a dozen ways of calculating realized volatility, with enough variation that this dude built a flow chart for aspiring analysts to help them figure out which to use:

Source: Harel Jacobson, “The Realized Volatility Puzzle“

To make matters much worse, even the concept of realized volatility may be misapplied at best, irrelevant at worst.

By definition, volatility is the amount of dispersion in some sample set over some specific period of time. So when we describe something like “the standard deviation of the S&P 500 over the past 30 days” and mentally apply that to our internal sense of “how risky” the market is right now, that’s flawed reasoning. Many smart people have written on those flaws, from Ole Peters, who asserted that we incorrectly assume “ergodicity” in finance (shorthand: the ergodicity assumption means that historical time averages can be used to make expected forward assumptions), to the work Benoit Mandlebrot did on “The MultiFractal Nature of Trading Time” back in the 1960s.

The point is this: simple historical realized volatility is something few folks can agree on and is also as essentially worthless as a predictor of the probability that Bad Things will occur.

Implied Volatility

As Buckaroo Banzai said: “Don’t tug on that. You never know what it might be attached to.”

When you read media coverage of volatility, you might get the impression that implied volatility is a magic observable data point that smart people extract from the options market.

In reality, implied volatility is a plug figure that explains how much options cost. To calculate, you punch your observed options premium into the Black-Scholes options pricing model (which almost nobody *actually* uses un-modified day-to-day, and in itself is so full of issues that it’s worth entire college courses on the topic); you put in all the other “knowns” (time-to-expiration, risk-free rate, spot and strike prices); then you literally just iterate over and over again, until you’ve solved for the volatility you’d need to justify the premia that are being demanded.

While this sounds impressive, the truth is that “implied volatility” really only tells you how cheap or expensive an option is, relative to some theoretical other option that might have the same inputs. It tells you very little about the actual probability that Bad Things will happen.

The VIX Index

The “VIX” is a calculation done by CBOE based on the implied volatility of options on the S&P 500 index. But it’s not a universal summary: it only and specifically considers option contracts that will expire between 23 and 37 days from today.

Furthermore, it uses a different kind of calculation for implied volatility, which is calculated from the variance of prices (that is, the options premia) for options with different strike prices, but which all have the same days to expiration (the idea being that if everything else is held the same, then price differentials can only be explained by implied volatility). Many different option contracts are used in the VIX, based on what’s trading, and all these little sub-calculations are then averaged and turned into a volatility number. It’s kind of like historical volatility, but imaginary!

That number is then multiplied by 100 (for no particular reason) to get the VIX metric. By all means, try calculating it for yourself—fun for the whole family.

As complicated as the VIX is, it too isn’t that great at describing “volatility,” at least outside its very narrow mandate. And it definitely doesn’t tell you anything helpful about how likely a Bad Thing is to happen.

So the TL;DR here is pretty simple: even in the best of times, finance is pretty bad at explaining what we mean by “volatility.” We (meaning me) use the word casually and unskillfully most of the time.

On top of which…

Part 2: Humans Are Messed Up About Risk

I realized during the past year and change of quarantine that there really isn’t a past or present. There’s only the now. No matter how much we plan for the future, all we have to work with at any given moment in time is what’s in front of us.

Despite this inherent truth, as advisors, you’re tasked with taking that present state of your client — say the $5 million nest egg they’ve socked away — and preserving and growing it for some unknowable future. And for the most part, the only tools we have to work with are those built from deep analysis of an irrelevant past.

That’s modern finance in a nutshell: we look at history, make observations, build models — whether conscious or unconscious — of how the future should go based on all the current-moment best guesses we can input into those models.

The most obvious problem is that the past is almost always a terrible predictor of the future. But slightly less obvious is that those of us in modern economics — as well as the models we build that everybody uses to predict the future — make a lot of really huge assumptions.

The biggest assumption, probably, is normalcy: that is, any pattern we analyze, from returns to health outcomes, follows that nice symmetrical bell-shaped curve we call a normal distribution. The second is that we often assume that the performance of a single security or metric over time (e.g., the average movement of one stock over a year) tells us something about the performance of an ensemble (e.g., the average movement of 500 stocks over one day). This “ensemble” vs. “time” way of looking at data is at the heart of Ole Peters tackling the aforementioned ergodicity problem.

Those are just two biggies. Pick any financial model, and there are some wild assumptions in it. I guarantee it.

As a result of all these assumptions, our modern financial models — perhaps most importantly our internal, mental models — are deeply flawed. This is probably why I keep hearing from folks repeatedly: the market feels a lot more volatile than the numbers indicate.

The Lion in the Bush

There are dozens of reasons for this impression, beyond ergodicity and misconceptions around math: historically high valuations, wealth inequality, the winner-take-all nature of markets, liquidity concerns, Reg NMS, regulatory capture…you name it. All these factors seem to add tail risk to our expected outcomes, but you can’t even see that tail risk if you’re just chasing last week’s numbers. But it’s definitely in there. Here’s how Newfound’s Corey Hoffstein described it in a recent email exchange:

Were we to analyze weekly returns for the S&P 500 over time, one of things we would notice over the last 20 years is that they’ve become increasingly fat-tailed In other words, more extreme returns – both positive and negative – are happening with greater frequency.

There’s a growing group of folks who’ve observed that the tails of our experiences are more than just fat–they’re almost irrevocably unpredictable, easily perturbed, and possibly unknowable. They’re also trying to figure out what, if anything, investors can do about it.

Mike Green, a quant who moved recently from the private wealth side of the balance sheet at Logica to upstart ETF manager Simplify, explained it to me this way:

We are wired from an evolutionary perspective to respond to adverse information far more seriously than we are wired to respond to favorable information. Just put yourself back on the plains of Africa. If I say to you, “Hey buddy, there’s berries in that bush.” You’ll say “That’s nice, but I already ate not a big deal,” and maybe footnote it. But if I say to you, “Hey, there’s a lion in that bush,” your head is going to pivot and you’re going to start running. And kind of what I’m saying is: “there’s a lion in the bush.”

Of course, the lion in the bush is just “the bad stuff” (however we define it). It’s really easy to put that in a market context and think market crash — but the more I’ve studied up on long vol, the less I think it makes sense to think about this purely in terms of “downside protection.” Because the underpinning observation isn’t something as simple as “we don’t like when things go down” (See Kahneman et al.). It has much more to do with our fundamental psychological makeup.

Here’s how Cem Karsan, noted vol-tweeter, emoji-lord, philosopher-trader, and Founder at Kai Volatility Advisors, explained it to me:

The world is long. You eat, you breathe, you sleep long. You live in a house, you work a job. Because everybody’s long, and people are alive, people have fear: of death or decline or poverty. And they have always thought, since the beginning of time, to hedge that risk. It’s the tail risk to being alive. Because people want to hedge and because that tail does exist, there must be somebody who’s willing to be in the business of insurance.

So that’s the setup: we measure volatility badly, our models are probably worse than we think, we’re inherently caught up in our own risk aversion, and so we — meaning, the collective “we” of human beings and asset owners — seek protection. And that hunt for protection may actually have become the dominant feature of our markets.

Part 3: The Biggest Insurance Market in the Universe

“The business of insurance” in this ill-measured market is almost exclusively now in the hands of the options markets–specifically, equities and their derivatives (options and futures contracts).

Cem again:

Ultimately, how does somebody who’s managing the risk on writing that insurance manage that risk? There are ways to hedge. The insurers are short-put/long-call, and they’re happy to be so. It’s a very profitable trade. Because they’re sitting on the other side of a unlimited demand machine, and they get to set the price to make sure it’s profitable.

I want to pause here and linger on these three sentences. Cem — and I think he’s a reasonable proxy for the zeitgeist here — is arguing that essentially, there is no limit to the demand for hedging risk. And because of that, the pricing power of the options market makers is limited only by their competition amongst themselves. The way they compete, long-term, isn’t just about price; it’s about how well they can hedge. That means the real competition is happening in on the risk management side of the business.

In trying to really understand this infinite demand engine, I leaned on Adam Butler, CIO at Resolve Asset Management, who thinks even the infinite demand machine doesn’t explain the full nature of how the tail has come to wag the dog (emphasis mine):

Consider that options are the ultimate source of leverage, and have become the instrument of choice for a large and increasingly dominant class of investors. Excess demand for leverage flows through options models and is reflected as higher implied volatility (among other things).

In other words: as an individual investor, I can get pretty substantial leverage out of the options market, even if I personally don’t care about hedging my downside. Which means I might still be a significant player in the options market, even if I’m just a degenerate gambler who wants to be maximally levered at all times. The options market makers are more than happy to feed that beast too.

Adam continues:

Moreover, many investors require regular cash flows to meet near-term liabilities. With yields on traditional instruments so low, many investors have turned to selling options (or buying products that implicitly sell options) to generate excess yield. These volatility sellers suppress volatility.

While we think of “the options market” as being nothing but pros, the “vig” (to use a gambling term, basically the cut charged by a sportsbook for taking a bet) is so good in this business that any investor with $100 in their Schwab account can essentially be in the insurance business, too. That’s all the various ETF wrapped options-writing strategies are: institutionalized and packaged access to the insurance market.

Of course, in the absence of people looking to “buy protection,” those types of strategies just go into the other side of the market makers balance sheet. Adam again:

At the same time, market makers facilitate the flows between these and other agents, but they do not wish to carry risk on their books. So they offset these risks by buying and selling the underlying cash instruments in markets to maintain their hedge. The ability of markets to absorb these flows may also impact measures of implied volatility.

I’m leaning on the dramatic bold here for a reason: this is the part where the connection is essential. Grab a coffee. Adjust your glasses.

The most important players in the market right now aren’t sovereign wealth funds or Calpers or meme lords or even traditional hedge funds. It’s the person sitting behind a screen trying to manage their equity market exposure to offset the risk of their options market-making book.

There are more than a few folks out there working to understand this better, from outsider-renegade Lily Francus’s work on options flows to Corey Hoffstein’s work on liquidity. But they’re all coming to pretty similar conclusions (from Hoffstein):

The “why” behind the data is heavily debated, but one theory is that significant adoption of call- and put-overwriting strategies by institutions has caused the order flow from option dealer hedging to become increasingly influential. Naively modeled, this hedging behavior is usually mean-reversionary, which helps keep markets pinned. If the hedging volume disappears, the market can suddenly move much further, faster.

That “much further, faster” is precisely what the market “feels” like, while at the same time, those traditional measures of volatility we started with aren’t flashing big red signs. If Parts 1 and 2 of this tried to show “stuff’s weirder than we really measure,” then here I’m trying to get to the “why?” and perhaps more importantly, the “so what?”

Why Hedging Matters

To understand WHY this options hedging can matter so much, I found I had to go past my basic understanding of options (and heck, I used to WORK for CBOE) and really try and grok-in-fullness what I personally would have to do if I was trying to be in this insurance market.

Let’s say I sell you a put that lets you sell me the S&P 500 Index at a price we decide on today, a month in the future.

Since we agreed on the price, I’ve become worried that the S&P will go down a lot. As Adam Butler pointed out, I don’t really want that risk, so I will short the S&P 500 some amount not to go bankrupt when things go down.

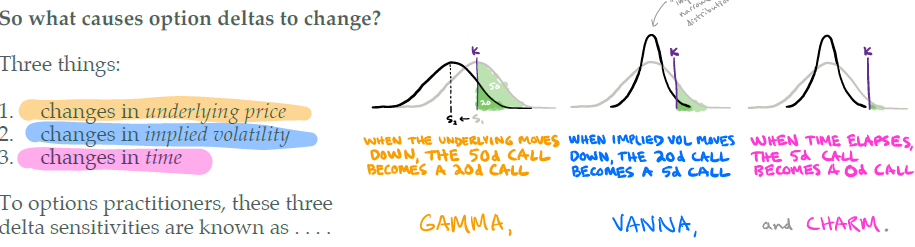

The amount I hedge is generally my “delta” — another options-related Greek symbol that means “how much this option will move based on a move in the underlying price.” A delta of 1 means “if the underlying moves 1%, the options price moves 1%,” and it’s usually quoted as points to the right of the decimal. So a 50 delta position means your position is exposed 50% to moves in the underlying.

The problem is that delta —which I’m using to determine the amount of that real-world short position I put on — constantly changes, but in fairly predictable fashion. The single-best thing I’ve ever read explaining this is the paper: “The Implied Order Book” from “Squeezemetrics.” Here’s the best chart:

I promise, there’s not going to be a quiz. The key point here is that the amount that usually-short hedge must change is based on THREE things: movement of the underlying (gamma); changes in implied volatility (vanna, which is another way of saying “how risky do I think this insurance is, and thus, how expensive is it?”); and changes in time (charm).

If you’re connecting dots here, what this means is that the hedging activity of the options dealers is actually a procyclical force. If most people want to hedge the downside, Then as time passes, the index will rise. When you get a calm week or two, the hedges roll off, which in turn becomes buying activity, which further supports the market.

That is, until you get some exogenous shock to the system and those fat tails show up.

So the very tools we have to mitigate the “fat tails” are likely contributing to them — in both directions. And people wonder why the market feels “janky” most days.

Part 4: So Now What?

Importantly, if this is the nature of the market, then what do you as an advisor actually do with this information? Here’s Simplify’s Mike Green again:

The reality is that this is a solvable problem, but it requires us to get past some of the deep misunderstandings … and moving into the long volatility space to protect your portfolio.

Here’s a more direct answer from Chris Cole and the team at Artemis Capital in their January 2020 client letter (which you should read, seriously):

Long Volatility must be differentiated from traditional Portfolio Insurance (“Tail Risk Hedging”) because it forgoes continuous protection for a lower carrying cost. The concept is to sacrifice the first move in an asset in exchange for lower costs while capturing the explosive second and third moves up or down.

I’ll be honest, that isn’t the most satisfying answer. Six months in a well, and it turns out all I need to do is… climb the ladder? What about all the hairy “life is long” stuff?

But the reality is, even considering long vol in a portfolio context is a pretty complex way of rethinking the total portfolio, which of course, means there’s now a cottage industry in helping connect the dots.

Jason Buck, CIO of the volatility-centric Mutiny Fund (and Co-Host of Pirates of Finance, the best financial content on YouTube), gives this take:

We think of the world as volatility parity. Your stocks and bonds, they’re all mean reverting or convergent strategies, which are short volatility. And then you combine those with your long volatility strategies or your commodity trend followers, which are all divergent strategies, which are long volatility. What we try to express to people is having the correlated, uncorrelated, negatively correlated all in the same book, rebalanced frequently, is how you can compound wealth over time.

How “long vol” folks implement their strategies are all over the map. Some stick to very tightly managed, at- or near-the-money straddles on a single index like the S&P 500–essentially “gamma scalping,” as the price movements create lots of small opportunities to profit. Others take more significant out-of-the-money bets, opportunistically generating income from selling options in some cases, reinvesting in insurance in others. In almost every case, proprietary models and data sets are feeding a usually quite-active trading strategy.

This is genuinely new, even if the foundation of “tails-centric” investing dates back to the 1960s, touching on behavioral economics and fractal math (and probably psychedelics, who knows). But changes in monetary policy and the rise of high-frequency trading have changed the game, to say nothing of the rise of ETFs and passive investing.

The actual observational work of how self-reinforcing systems, accidentally non-ergodic models, and modern policy combine to create risks and opportunities is being done every single day: on blog posts, on Twitter, at Epsilon Theory, on Real-Vision, on Hedgeye…and, like it or not, in the moment-to-moment pricing of every equity instrument in your portfolio.

As Buck put it:

If anybody has a backtest prior to 2015 on a long volatility strategy, I almost throw it out the window, because the markets have changed that much. And so now you have a flows based world. And then now the derivative world is becoming so big, it’s the tail that wags the dog.

So what do we do?

Well, we can look to products that bake in the “long vol” side of the trade, from upstarts like Simplify and old-guard firms like Nationwide. Most of them are great tools. But they’re also very, very fine tools — sharpened and refined in a machine shop that is itself being rebuilt daily.

So what we all should really do is check our preconceptions at the door about how markets used to work and wade deep, deep into the pool until we really understand how this flows-driven, risk-managed market is actually influencing our portfolios.

I, for one, no longer think what I learned in the 1980s and 1990s about economics and markets has really any value whatsoever, other than as a historical backdrop. But I also don’t think there’s a one-size-fits-all answer to the “so what?” As market participants, it’s on us to stay curious, stay informed, and get our hands dirty.

Look at your portfolios. Question your assumptions. Answer for yourself: “what happens if I’m wrong, and both tails of my future returns are much fatter than I think?”

There’s no “Groking-in-Fullness” otherwise.

[NOTE: Special thanks to all the folks mentioned here who gave me a lot of time answering my questions. I apologize to the few-dozen very good folks I just didn’t get a chance to chat with — all the “but you forgot!”s and any egregious errors here are entirely my own.]