Thought to ponder …

“Practice gratitude. It’s tempting to whine and complain when things go wrong. But it’s crucial that we acknowledge two cardinal truths. First, whining and complaining about unfavorable conditions does nothing to resolve them. Second, it can too easily introduce a host of negative emotions that result in further despair and disappointment. Maintaining a positive mindset is pivotal to facing adversity with courage. Each morning, reflect on things that have gone right for you. Each afternoon, think about everything you have for which to be thankful. Each evening, before you go to bed, contemplate the small victories you enjoyed throughout the day. Practice gratitude daily.”

–Damon Zahariades

“The Mental Toughness Handbook”

The View from 30,000 feet

Putting it all together

- The path for lower rates in the U.S. has finally arrived. Last week the Fed tipped the balance of risks on their scale from evenly balanced between inflation concerns and labor market concerns, to weighted to concerns about the labor markets.

- Powell was careful to note that the “timing and pace” of cuts are still in flux, but “the direction of travel is clear”.

- Historically a pivot in policy to lower rates is not a great thing for equities because the change in direction is either associated with a negative financial event / dislocation or a dramatic deterioration of economic activity. There is precedence dating back 1995 when neither negative outcomes occurred, and the markets continued to plug along higher, but rates didn’t move sharply lower either.

- The Fed’s balancing act is tricky. Inflation seems contained for the moment, but the trajectory of the labor markets, GDP and manufacturing are lower. On the flip side, the service side of the economy is holding up and the consumer continues to spend, so the economy is not devoid of momentum. Meanwhile, the world’s other two largest economies, the Eurozone and China, seem inextricably linked and struggling to find footing for growth, leaving it up to the U.S. to carve its own path.

- We think it’s possible for the economy to skirt a recession and continue to grow. We remain advising clients to be positioned for such an outcome, but a continuation of the pattern of strength in the economy and markets are by no means foregone conclusions. The economy is a complex system, where self-enforcing feedback loops can create both surprising strength and fragility.

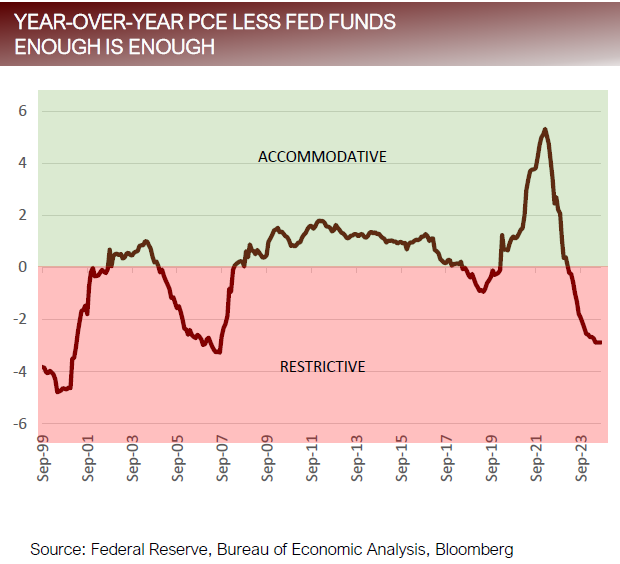

Powell dovish – confirms lower rates

- In 2022, Powell gave the public eight minutes of gut-wrenching

hawkish rhetoric. In 2024, he reversed course and provided a

dramatic dovish transition to a new era. However, there’s a lot

of wood to chop to get back to accommodative. - History shows the equity markets perform much better during

accommodative periods.- The average differential between year-over-year PCE and Fed Funds was -1.09 from 12/31/1999 to 12/31/2009. During that time, the S&P500 returned an average annual return of -0.95% per year.

- Conversely, the average differential between year-over-year PCE and Fed Funds was 0.85 from 12/31/2009 to 12/31/2019. During that time, the S&P500 returned an average annual return of 13.54% per year.

- Today, the differential between year-over-year PCE and Fed Funds is -2.90. The Fed needs to rapidly move rates lower by over 2.5% to prevent significant impairment of the economy.

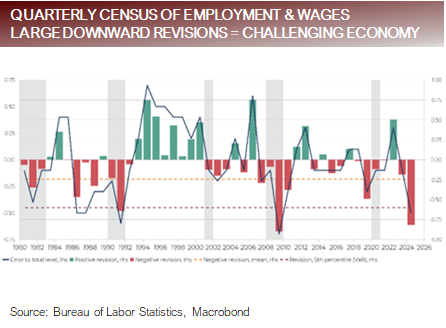

BLS revises payrolls sharply lower

- The Bureau of Economic Statistics April 2023 to March 2024 annual benchmark revisions indicated that the economy added 818k few jobs than initially reported over that time frame.

- Significant weakness in the numbers was shown in the white-collar sectors of business and professional services of -528k jobs.

- The likely cause of the size of the error in calculation, which is about 5x larger than average, has to do with adjustments in the birth/death model, which estimates payroll growth of new and closing businesses.

- Revisions for the first half of 2024 all but wipe out payroll gains this year, signaling a potential upwards revision in the unemployment rate. The downward revision won’t be fully reflected in the employment data until February 2025 when the BLS incorporates revision into the previous 12-months.

- Significant downward revisions in the QCEW have historically been associated with weak economic periods.

Fed meeting minutes confirm bias

- The minutes from the July Federal Open Market Committee had a handful themes:

- Broadness of disinflation across categories and among retailers

- Diminished factors for inflation and risks of disinflation in the future

- Citing “greater confidence” in reference to inflation retuning to the targeted range

- The “vast majority” indicating that inflation coming in as expected.

- Balance between inflation and employment mandates

- Better balance in labor markets, associated with levels of equilibrium

- Risk of accelerated deterioration in labor markets

- Agreement that it would be appropriate to begin cutting rates at the next meeting

- It’s not much of a stretch to conclude that if the economy is at balance between employment and inflation and there is downward momentum in the labor markets, policy should be erring on the side of dovish.

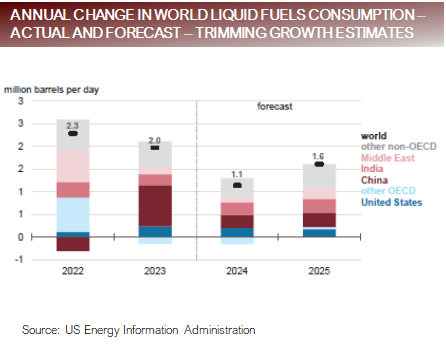

Oil demand forecasts point lower

- Demand forecasts for the major agencies that project energy markets indicating that oil demand will soften.

- US Energy Information Administration (EIA) – Projects global consumption of liquid fuels will increase by 1.6 mbd in 2024, down from 1.8 mbd in their previous forecast.

- International Energy Agency (IEA) – Noted that oil demand continues to decelerate to 710 kbd, the slowest quarterly rate of increase since Q4 2022, while at the same time strong production gains from non-OPEC+ members is driving an increase in production forecasts.

- OPEC+ – Cut their 2024 demand forecast from growth of 2.25 mbd to 2.11 mbd, based on weak demand growth from China. They also cut their 2025 estimates for demand growth from 1.85 mbd to 1.75 mbd.

- Energy prices are a major input into CPI and PCE. To the degree demand is falling, while non-OPEC+ continue to boost production, it likely places a ceiling on oil prices, barring geopolitical events that inject volatility.

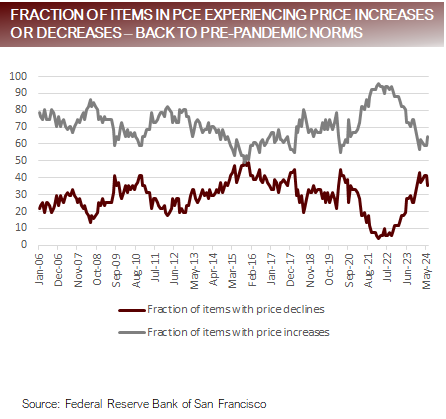

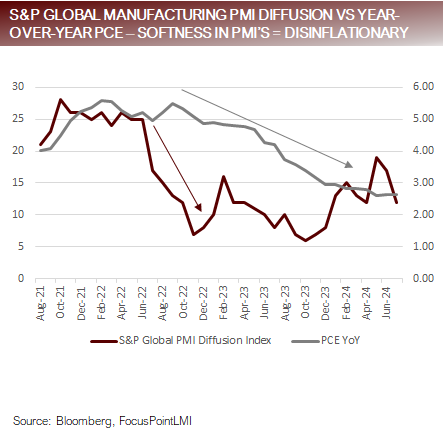

PMIs support disinflation confidence

Manufacturing Purchasing Manager Indices have traditionally been a good leading indicator of economic activity. However, since the pandemic they have been a less reliable leading indicator of activity, and instead been a much better leading indicator of inflation.

The S&P Global Manufacturing PMI captures survey data from 30 countries. Focus Point has constructed our own diffusion index, which shows the number of countries in “expansion”, defined as having a PMI above 50.

Since the pandemic, when the number of countries in expansion is above 20 or rising and approaching 20, inflationary forces are high, and have been associated with upside surprises in CPI and PCE. Beginning in Q2, Manufacturing PMIs began falling, which coincided with a reduction of inflationary forces throughout the summer.

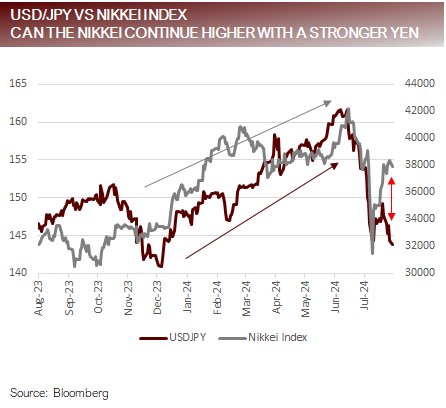

- Japan — Still a good bet with a strengthening yen?

- The central banks of the US and Japan indicated contrary paths last week, with the Fed providing an outlook for lower rates and BoJ indicating that rates would continue higher. There are a host of factors the influence currency crosses, such as:

- Relative interest rates policy

- Current account surplus vs deficit

- Relative growth trajectories

- Fiscal policies

- Geopolitical influences

- Sentiment

- Over the course of 2024, the Nikkei has broken out on a combination of a weak currency, expectations that the

corporate environment is becoming more investor-centric, the belief the years of disinflation are behind Japan and a manufacturing renaissance related to trading partners moving away from China. - We think the currency has had an outsized impact on the strength in the Nikkei and the path higher for equities will be challenging as the JPY strengthens.

For more news, information, and strategy, visit the Innovative ETFs Channel.

DISCLOSURES AND IMPORTANT RISK INFORMATION

Performance data quoted represents past performance, which is not a guarantee of future results. No representation is made that a client will, or is likely to, achieve positive returns, avoid losses, or experience returns similar to those shown or experienced in the past.

Focus Point LMI LLC

For more information, please visit www.focuspointlmi.com or contact us at [email protected]

Copyright 2024, Focus Point LMI LLC. All rights reserved.

The text, images and other materials contained or displayed on any Focus Point LMI LLC Inc. product, service, report, e-mail or web site are proprietary to Focus Point LMI LLC Inc. and constitute valuable intellectual property and copyright. No material from any part of any Focus Point LMI LLC Inc. website may be downloaded, transmitted, broadcast, transferred, assigned, reproduced or in any other way used or otherwise disseminated in any form to any person or entity, without the explicit written consent of Focus Point LMI LLC Inc. All unauthorized reproduction or other use of material from Focus Point LMI LLC Inc. shall be deemed willful infringement(s) of Focus Point LMI LLC Inc. copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Focus Point LMI LLC Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Focus Point LMI LLC Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.

All unauthorized use of material shall be deemed willful infringement of Focus Point LMI LLC Inc. copyright and other proprietary and intellectual property rights. While Focus Point LMI LLC will use its reasonable best efforts to provide accurate and informative Information Services to Subscriber, Focus Point LMI LLC but cannot guarantee the accuracy, relevance and/or completeness of the Information Services, or other information used in connection therewith. Focus Point LMI LLC, its affiliates, shareholders, directors, officers, and employees shall have no liability, contingent or otherwise, for any claims or damages arising in connection with (i) the use by Subscriber of the Information Services and/or (ii) any errors, omissions or inaccuracies in the Information Services. The Information Services are provided for the benefit of the Subscriber. It is not to be used or otherwise relied on by any other person. Some of the data contained in this publication may have been obtained from The Federal Reserve, Bloomberg Barclays Indices; Bloomberg Finance L.P.; CBRE Inc.; IHS Markit; MSCI Inc. Neither MSCI Inc. nor any other party involved in or related to compiling, computing or creating the MSCI Inc. data makes any

express or implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of such data. Such party, its affiliates and suppliers (“Content Providers”) do not guarantee the accuracy, adequacy, completeness, timeliness or availability of any Content and are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, or for the results obtained from the use of such Content. In no event shall Content Providers be liable for any damages, costs, expenses, legal fees, or losses (including lost income or lost profit and opportunity costs) in connection with any use of the Content. A reference to a particular investment or security, a rating or any observation concerning an investment that is part of the Content is not a recommendation to buy, sell or hold such investment or security, does not address the suitability of an investment or security and should not be relied on as investment advice.

This communication reflects our analysts’ current opinions and may be updated as views or information change. Past results do not guarantee future performance. Business and market conditions, laws, regulations, and other factors affecting performance all change over time, which could change the status of the information in this publication. Using any graph, chart, formula, model, or other device to assist in making investment decisions presents many difficulties and their effectiveness has significant limitations, including that prior patterns may not repeat themselves and market participants using such devices can impact the market in a way that changes their effectiveness. Focus Point LMI LLC believes no individual graph, chart, formula, model, or other device should be used as the sole basis for any investment decision. Focus Point LMI LLC or its affiliated companies or their respective shareholders, directors, officers and/or employees, may have long or short positions in the securities discussed herein and may purchase or sell such securities without notice. Neither Focus Point LMI LLC nor the author is rendering investment, tax, or legal advice, nor offering individualized advice tailored to any specific portfolio or to any individual’s particular suitability or needs. Investors should seek professional investment, tax, legal, and accounting advice prior to making investment decisions. Focus Point LMI LLC’s publications do not constitute an offer to sell any security, nor a solicitation of an offer to buy any security. They are designed to provide information, data and analysis believed to be accurate, but they are not guaranteed and are provided “as is” without warranty of any kind, either express or implied. FOCUS POINT LMI LLC DISCLAIMS ANY AND ALL EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY, SUITABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE. Focus Point LMI LLC, its affiliates, officers, or employees, and any third-party data provider shall not have any liability for any loss sustained by anyone who has relied on the information contained in any Focus Point LMI LLC publication, and they shall not be liable to any party for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including, without limitation, lost income or lost profits and opportunity costs) in connection with any use of the information or opinions contained Focus Point LMI LLC publications even if advised of the possibility of such damages.