Thought to ponder…

“Every action you take is a vote for the type of person you wish to become. No single instance will transform your beliefs, but as the votes build up, so does the evidence of your new identity. This is one reason why meaningful change does not require radical change. Small habits can make a meaningful difference by providing evidence of a new identity. And if a change is meaningful, it actually is big. That’s the paradox of making small improvements. Putting this all together, you can see that habits are the path to changing your identity. The most practical way to change who you are is to change what you do.”

– James Clear, Atomic Habits

The View from 30,000 feet

Putting it all together

- Employment data last week marked a turning point for investor expectations about the labor The combined weakness in Jobless Claims, JOLTS data and Unemployment spooked investors, who were caught trying to make peace with reassurances from Powell that it was okay to wait until September before cutting rates.

- According to Bloomberg’s market pricing probability model, in the last week investors have gone from looking for two and half 25 basis points cuts in 2024 to almost Keep in mind that there are only three meeting left in 2024, so the implications are that at least two of the cuts will be 50 basis points or there will be intra-meeting cuts, which is in fact what the CME FedWatch Tool indicates, with both September and November looking like 50 basis points.

- We expect the next few weeks to be littered with volatility leading up to Powell’s Jackson Hole speech, which has historically marked inflection points for the Fed. We expect more forceful assurances out of Powell given the current market volatility and would not be at all surprised to see an intra-meeting cut in September if we get another bad employment number at the beginning of next month indicating a non-linear move in employment is taking hold.

- None of this is good news. We continue to look for validation from consumer spending and earnings to support the notion that a significant economic slowdown is the destination. The employment market breaking down is certainly concerning and represents a significant domino falling but doesn’t necessarily topple other dominos.

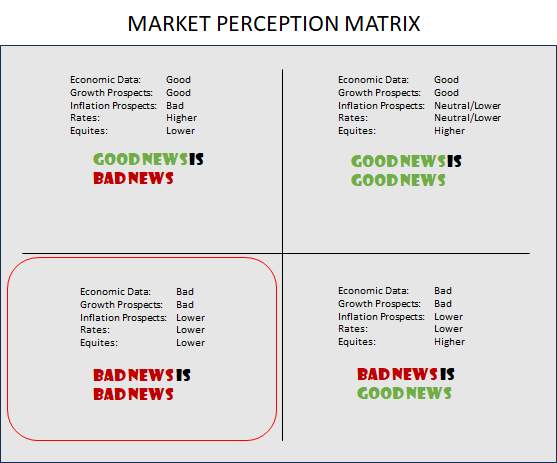

Updating the Market Perception Matrix

- The Market Perception Matrix is a framework we publish that provides a simplified way of understanding market reactions to economic data and news.

- We have transitioned to the Bad News Is Bad News quadrant. Several factors combined to shift perceptions over the last few weeks.

- Questioning the profitability of the AI trade

- Weak employment data

- An uptick in delinquencies signaling a deterioration of personal balance sheets

- The perception of central banks reacting to their agenda rather than the data

- This is quadrant can be extremely volatile, as investors are forced to wait out data to prove or disprove perceptions that the fundamentals are deteriorating, or central bank take actions to change psychology, or corporate earnings pull through to assure investors that any weakness in data are not flowing through to corporate prospects for earnings.

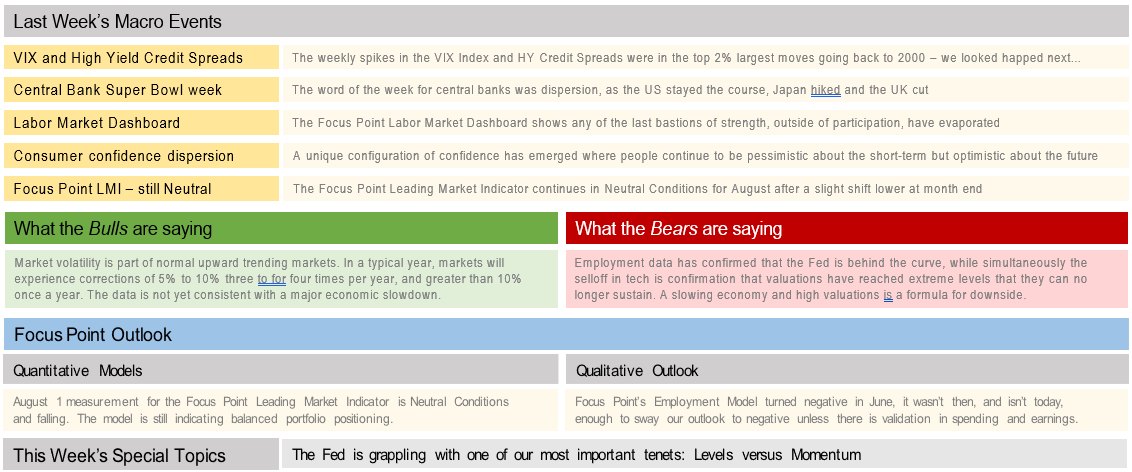

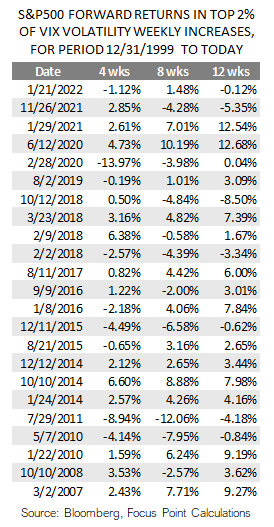

VIX and High Yield Credit Spreads

- Last week the VIX Index, which measures the expected volatility of the S&P500 for the next 30 days calculated by comparing a range of call and put options, increased from 16.39 to 23.39, which was an increase of 42.7% and in the top 1.9% of all weekly moves in the VIX Index since 2000.

- We looked at moves in the VIX Index and High Yield Credit Spreads, which moved up 7%, which was also in the top 2.0% of weekly moves since 2000, and compared periods in the top 2.0% for each with forward returns for the S&P500 Index. Some observations about historical periods:

- Average gains for the S&P500 during the top 2% over the next four weeks were less than 25% of the entire period, with the probability of a positive gain being slightly lower.

- Average gains for the S&P500 during the top 2% over the next twelve weeks was about 200% the average, with the probability of a gains rising materially.

- The conclusion based on historical analysis is that in the short- term the markets will likely remain choppy with lower-than-average gains, but as we move several months out, the probability of higher-than-average market gains increases significantly.

Central Bank Super Bowl Week

- Last week the U.S. Federal Reserve, The Bank of Japan and the Bank of England The scorecard was as follows:

- S. Federal Reserve – No change to rates

- Bank of Japan – Raised rates 15 bps

- Bank of England – Cut rates 25 bps

- From a qualitative standpoint:

- The U.S. Federal reserve is trying fend off the last remanent of inflation, while maintaining enough momentum in the economy to not crash the labor markets.

- The Bank of Japan is trying to normalize policy and protect their currency from policy actions dating back to 2016.

- The Bank of England is trying to normalize policy because headline inflation is below their target, but their job has been made complicated by services inflation remaining sticky and an economy at the whim of energy prices.

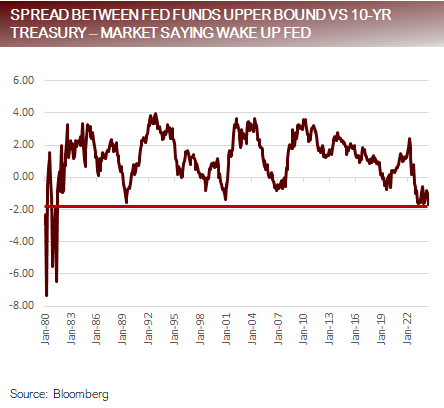

- The conclusion – The markets strongly disapprove of both Fed and BOJ policy decisions.

- The spread between the Fed Funds Upper Bound and the 10-year Treasury is -1.71, the highest since 1981.

- The Nikkei selloff in the last three weeks is the in the top 1% of the largest three-week drawdowns since 1980.

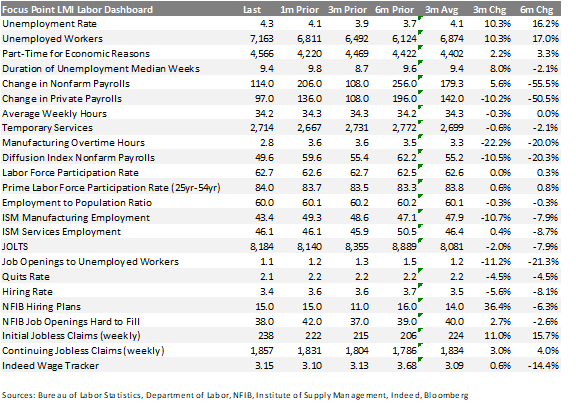

Labor Market Dashboard

- Looking at 24 different indicators of the labor markets provides a good sense of the relative strength or weakness in the labor markets as well as overall A few numbers from this month’s Dashboard stand out as particularly concerning:

-

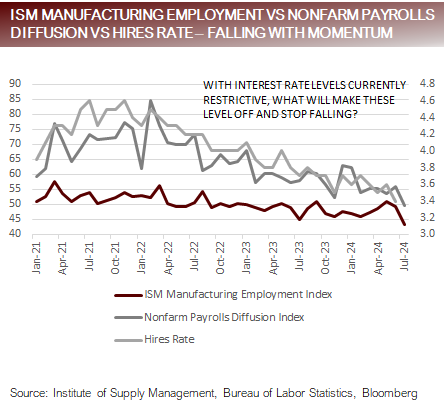

- The ISM Manufacturing Employment touched 43.4. Historically, readings below 44 and falling are strong signals of weakening labor markets.

- The Nonfarm Payrolls Diffusion Index, fell below 50 and is falling, which has historically signaled an extremely weak labor market.

- The Hires Rate fell to 3.4, the lowest it has been outside the pandemic since 2013, signaling that companies are freezing hiring plans.

- Interestingly, the rise in unemployment is being driven by an increase in participation of prime age workers. This is key, if participation begins to fall and unemployment also continues to rise, it would confirm the probability of a significant weaking.

- It should be noted that Focus Point’s Employment Indicator, which is used within the Focus Point Leading Market Indicator, turned negative at the end of June.

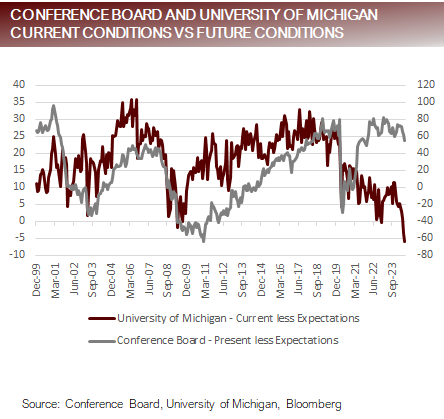

Consumer confidence dispersion

- Last week’s Conference Board Consumer Confidence release brought with it an interesting message in dispersion. The Present Conditions versus Expected Conditions, began to breakdown, and looks to be following the lead of The University of Michigan Consumer Sentiment Index.

- The bottom began to fall out of The University of Michigan spread between Present Conditions and Expected Conditions in May and the relationship has shown continued downward momentum since then.

- This begs the question of what is causing consumers to be so negative about their current situation, and optimistic about their future prospects? The surveys are heavily influenced by outlooks for inflation, employment and politics, so any of these could be the root cause. Our view is the downside deviation is being caused by consumers being hurt by inflation and high interest rates. When consumers look to the future these are topics they are hoping to get some relief from.

Focus Point LMI – still Neutral

- The Focus Point Leading Market Indicator continued in Neutral Conditions for the 17th consecutive Of the 28 indicators the make up the Focus Point LMI, two of them turned negative for the month causing a slight downward shift within Neutral Conditions.

- The Bloomberg Financial Conditions Index turned negative for the Focus Point utilizes information from two different Financial Conditions Indexes – The Bloomberg Financial Conditions Index and the Chicago Fed Financial Conditions Index. The major differentiator between the two is that the Bloomberg index is more heavily influenced by market indices, such as equities, fixed income and currencies, whereas the Chicago Fed index is more heavily influenced by liquidity, spreads and volatility. The former represents what we see on the surface of the markets, the later is more like what is lurking beneath the waters. To the degree there is a superficial selloff in the markets we would expect this to show up in the Bloomberg index, while a more serious problem with the plumbing would likely show up in the Chicago Fed index.

- Focus Point’s Treasury Momentum model also turned negative at the end of The 10-year Treasury began the month at 4.46 and ended the month at 4.02. Similarly, the 2-year Treasury began the month at 4.75 and ended the month at 4.25. These are massive swings. Although lower rates is welcome news to borrowers who might want to buy a home or car, dramatic shifts lower in rate have frequently been a bad omen for risk-asset prices because they indicate the types of shaky market conditions where the Fed is expecting to cut interest rates or some condition that is driving a flight to safety from an exogenous shock.

The Fed is grappling with one of our most important tenets: Levels versus Momentum

- When Focus Point develops an indicator, we look at three key metrics: Level, Velocity and Acceleration.

- Think of it as if you are driving a car from zero to 60. At any given point we could measure three things:

- How fast are you going?

- Is your speed increasing or decreasing?

- Is the rate of the increase or decrease in speed going up or down?

- In our opinion, this is where the Fed is missing the boat. They appear to be too heavily weighted on the Level, without recognizing Velocity or Acceleration.

- If I were going to ask the Powell a question at the pressor, my question would be – You have conceded that interest rates are restrictive and slowing the economy, if the employment indicators you are looking at are currently at or below levels that indicate a resilient labor market, what would make you think they would stay at that level, if they are falling with Velocity and Acceleration consistent with increasing momentum?

For more news, information, and analysis, visit the Innovative ETFs Channel.