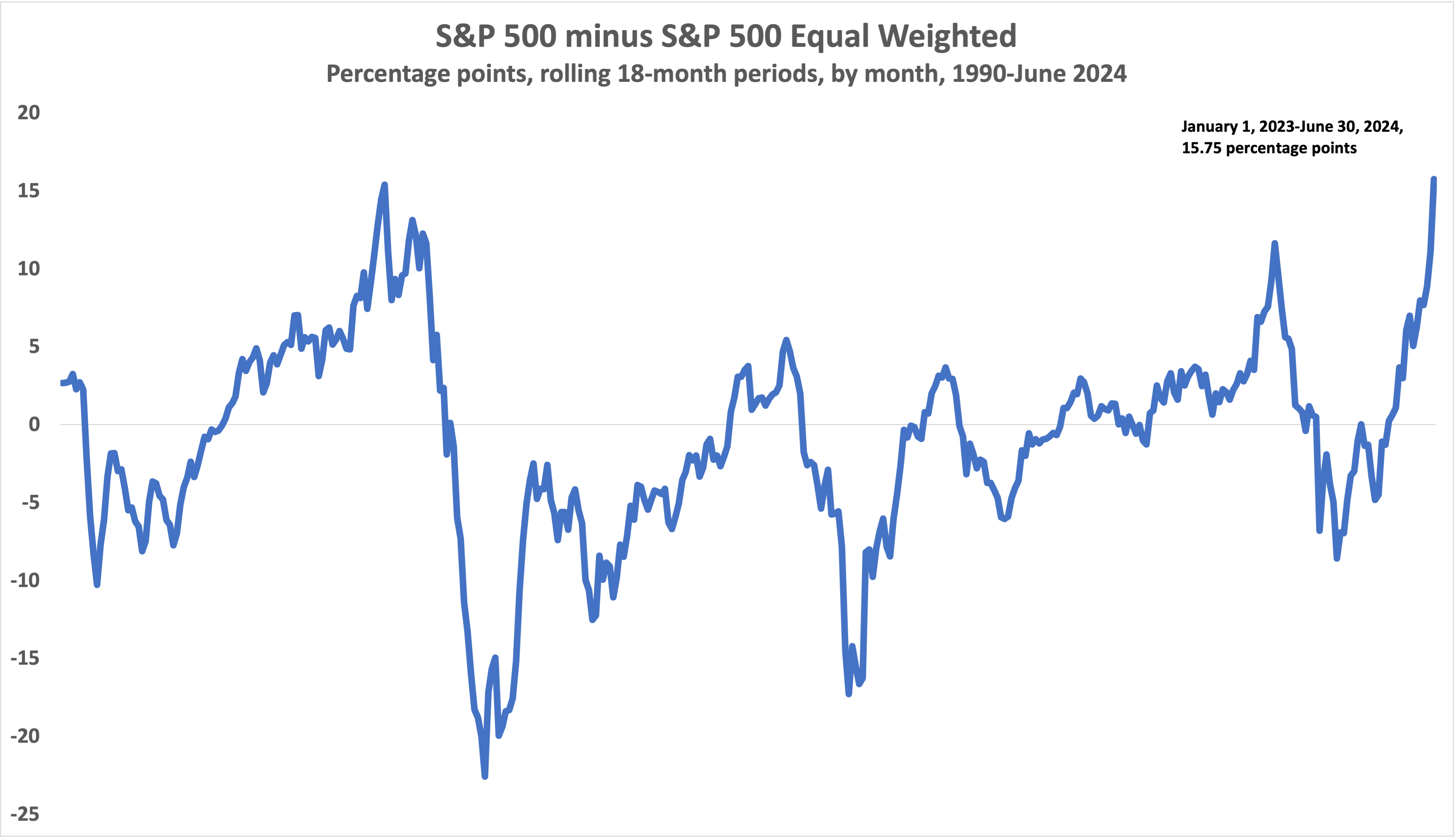

The SPDR S&P 500 ETF Trust (SPY) just posted its best 18-month performance period versus the Invesco S&P 500 Equal Weight ETF (RSP) since the latter’s late April 2003 inception.

We rolled 18-month periods by month from May 2003 through June 2024, more than 21 years, and SPY outperformed RSP by a blistering 15.82 percentage points for the 18 months ending in June 2024. SPY returned 28.3% on an annualized basis for the most recent 18-month period, while RSP returned 12.46%.

That outperformance took out the previous high for SPY outperformance over RSP of 11.71% from March 2019-August 2020. That period encompassed a stretch starting a year before the COVID-19 lockdown through six months into the lockdown. Both periods are marked by large growth stocks outperforming dramatically.

From March 2019 through August 2020, the Russell 1000 Growth index delivered a 28.73% annualized return versus an anemic -0.02% return for the Russell 1000 Value index. Similarly, over the most recent 18-month period, the growth index outperformed its value counterpart again, with a breathtaking 43.67% annualized return versus a 12.2% return.

Also, for the 18 months through June 2024, the worst-performing “Magnificent Seven” stock, Tesla, returned 37% on an annualized basis. The best performer, Nvidia, returned an eye-watering 315% annualized. Meta, in the second slot, returned 160%. Those stocks catapulted over SPY, while weighting them equally to the other 493 in the index took a massive toll on RSP.

RSP tracks the S&P 500 Equal Weight Index, which means it rebalances quarterly. Maintaining the underweighting of the large tech stocks with frequent rebalancing prevented them from driving RSP as high as SPY.

Comparing S&P 500 Performance: Back to the Last Tech Run

RSP’s inception date doesn’t take it back to the previous technology run-up in the 1990s. Therefore, we ran a second simulation pitting the S&P 500 TR against the S&P 500 Equal Weight index. The only other time the plain capitalization-weighted S&P 500 outperformed its equal-weight counterpart by 15 percentage points over an 18-month period was the October 1997 to March 1999 period, just before the tech bubble collapsed.

Reversal at Hand?

It’s impossible to say that tech bust will repeat this time, but it may be reasonable for investors to take some caution from this level of outperformance of the cap-weighted index versus its equal-weight counterpart.

For the month of July through the 29th, the funds underwent a modest reversal, with SPY posting a 0.13% return and RSP posting a 3.46% return.

That pattern is duplicated in the Russell indexes as well, with the Russell 1000 Growth Index returning a 2.93% loss and the Russell 1000 Value Index delivering a 4.25% gain.

A one-month modest reversal isn’t enough to hang your hat on, but investors should know too that from May 2003 through June 2024, RSP, even including this period of woeful underperformance versus SPY, has eked out a 0.04 percentage point annualized victory over SPY. Over that long stretch, RSP delivered a 10.88% annualized return versus a 10.84% annualized return for SPY.

Morningstar’s Rekenthaler Is Agnostic

Moreover, research from Morningstar’s John Rekenthaler in May 2023 (in the early stages of what turned out to be historic outperformance for the cap-weighted index) argues that the equal-weighted index has benefited from both value and small-cap tilts, though more the latter. Rekenthaler says in his article, “the equally weighted portfolio performed more like a small-company investment than a value portfolio. That said, the equally weighted portfolio did indeed favor value.”

Rekenthaler compared the costless indexes (not funds), and found that from June 1998 through April 2023, the equal-weighted index “thrashed the conventional index,” turning an initial $10,000 investment into $90,000 as opposed to $61,000 for the conventional index. Still, he doesn’t forecast that will continue.

Equal-weighted strategies initially suffered from a rollout by Dean Witter of an absurdly expensive equal-weighted fund in the 1980s that underwent its first transition in 1998 (when the tech bubble was near its peak). That makes the original performance records Rekenthaler compares favor the cap-weighted index, though the equal-weighted index didn’t perform abysmally.

Now that the Invesco fund has proved its mettle though, Rekenthaler “cannot explain why the equally weighted portfolio has been superior to the sum of its parts [or]prophesy that its success will continue.”

Modesty is a good trait in investing. Some pundits don’t think there’s a small-cap or value factor, after all, lately. Quality, though harder to define, has seemingly replaced those original Fama/French sources of outperformance. But those who want to put their money on an equal-weighted comeback at least can do it now after a historically bad period. Although it’s too short to call a reversal, for the month of July, SPY was up 1.21%, while RSP was 4.46%.

For more news, information, and strategy, visit the Innovative ETFs Channel.