With a potential vaccine ready for the masses in the United States, there seems to be less uncertainty in the capital markets despite the marked increase in COVID-19 cases. But you can never get too much quality when it comes to the corporate bond market, especially in the convenience of an ETF wrapper like the Invesco Investment Grade Defensive ETF (IIGD).

IIGD is based on the Invesco Investment Grade Defensive Index (Index). The Fund generally will invest at least 80% of its total assets in securities that comprise the Index, which is designed to provide exposure to U.S. investment grade bonds with relatively higher-quality characteristics, including higher credit ratings and shorter maturities.

All eligible bonds are assigned a quality score, which is calculated based on the bond’s maturity and credit rating. The Fund does not purchase all the securities in the Index; instead, it utilizes a “sampling” methodology to seek to achieve its investment objective. The Fund and the index are rebalanced monthly.

IIGD has bounced beyond its pre-pandemic level, giving investors a year-to-date gain of 5.88% based on Morningstar numbers. The quality is there with a majority of its debt holdings in AA or A credit quality, and duration risk on the short side with maturities typically falling between the 1- to 5-year range (as of December 4).

Tightening Spreads A Sign of Good Things to Come?

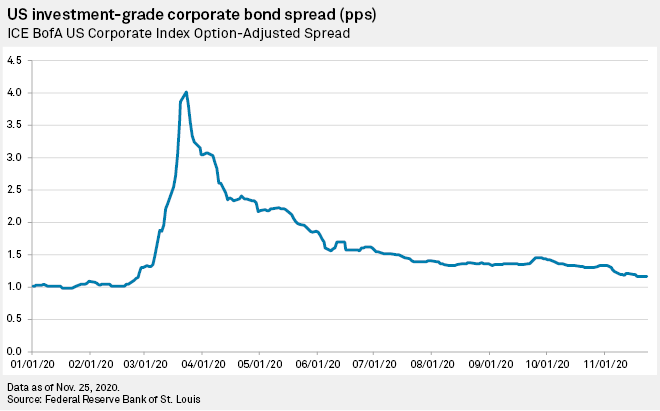

So where do corporate bonds go from here? Per a S&P Global Market Intelligence article, “As far as U.S. investment-grade corporate bonds go, the coronavirus pandemic is as good as over.”

“The ICE Bank of America investment grade corporate spread narrowed by 2 basis points in the week to Nov. 26 to 116 bps. The spread has now reversed 96% of the widening experienced during March when the implications of the pandemic for U.S. financial markets hit home,” the article added.

“Central bankers are principally concerned by elevated rates of unemployment and closing output gaps at a time when inflation remains well below target in most economies,” Dowding said in a market commentary. “This means adding fuel to asset purchases to push yields down and spreads tighter in order to promote accommodative financial conditions, even if the corollary of this is continued asset-price inflation in the near term.”

Additionally, a presidency under Joe Biden could bear fruit for the corporate bond market.

“A Biden presidency with a Republican-led Senate likely means more predictable foreign policy and no change in taxation, which implies lower uncertainty and higher corporate earnings,” Solita Marcelli, head of CIO Americas at UBS, wrote in a market commentary.