Economic indicators provide insight into the overall health and performance of an economy. They are essential tools for policymakers, advisors, investors, and businesses because they allow them to make informed decisions regarding business strategies and financial markets. In the week ending on May 16th, the SPDR S&P 500 ETF Trust (SPY) rose 1.64% while the Invesco S&P 500® Equal Weight ETF (RSP) was up 1.18%. Inflation has been an ongoing topic of conversation for the past few years because of its role in the Fed’s interest rate policy and its ability to quickly influence financial markets.

The Fed has been cautious about making any changes to monetary policy, emphasizing the need for confidence that inflation is moving towards their 2% target. This article looks to summarize three important economic indicators from the past week to provide insight into the latest trends in inflation and consumer spending.

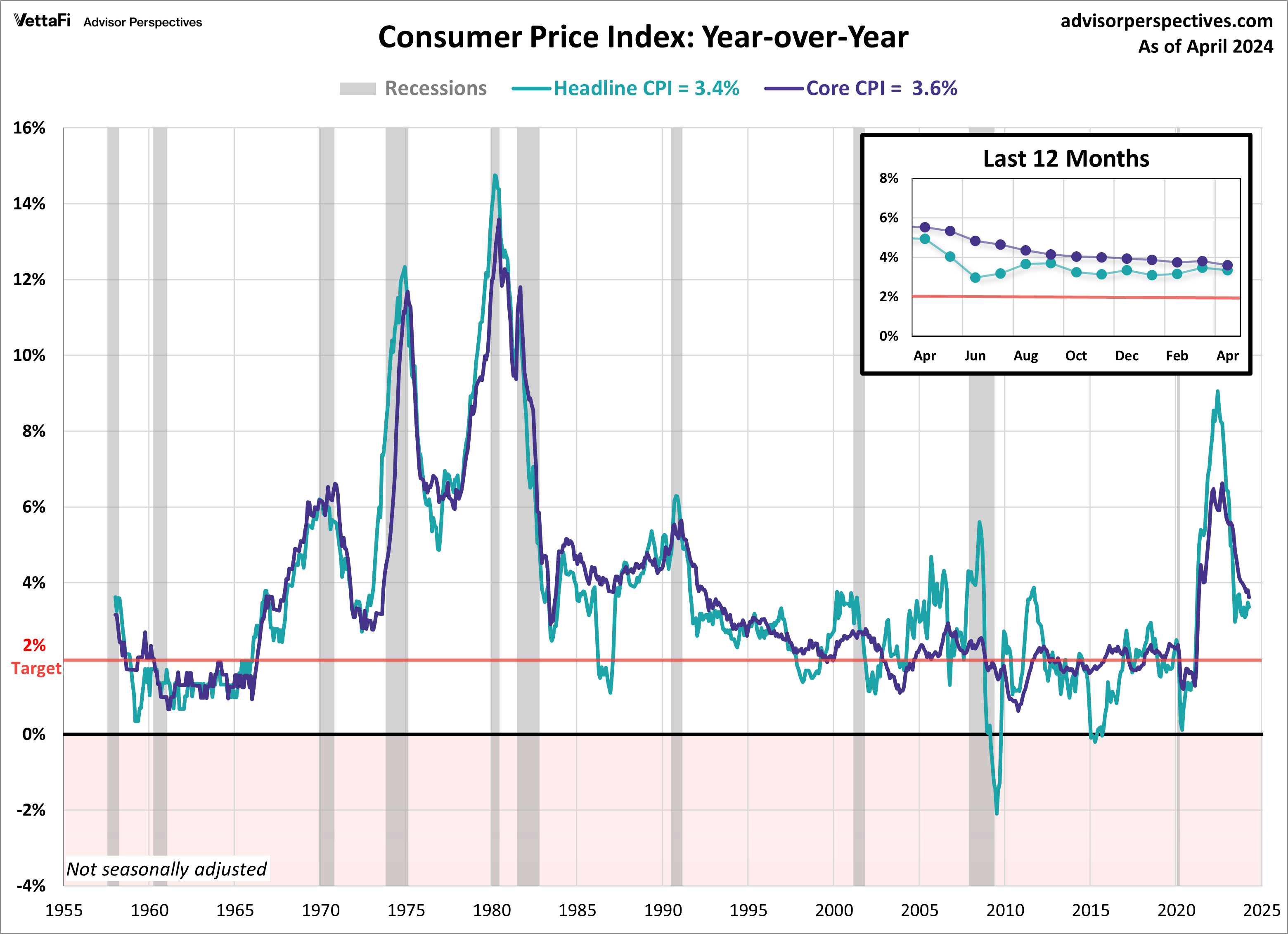

Consumer Price Index

Inflation finally showed signs of easing last month after several higher than expected readings to start off the year. The Consumer Price Index (CPI) rose 3.4% in April, down from 3.5% in March and in-line with expectations. Compared to the previous month, consumer prices rose 0.3%, which was lower than the expected 0.4% growth. The primary driver for April’s growth was the continued rise in shelter costs as well as an increase in gasoline. When combined, these two contributed to over 70% of the headline increase.

Core inflation, which excludes food and energy prices, cooled to its lowest level since April 2021. Core CPI fell to 3.6% on an annual basis, as expected. Additionally, core prices increased 0.3% from March, as expected.

The question remains as to when the Fed will begin to cut rates. While it’s still expected that the Fed will hold rates steady over their next couple of meetings, the latest CPI numbers support the notion for rate cuts later this year. At the time of writing, the CME Fed Watch Tool indicates a 91% likelihood for rate stability at the June meeting and a 69% probability for the July meeting. The CME Fed Watch Tool is currently showing a 51% probability that the first rate cut will take place in September.

Retail Sales

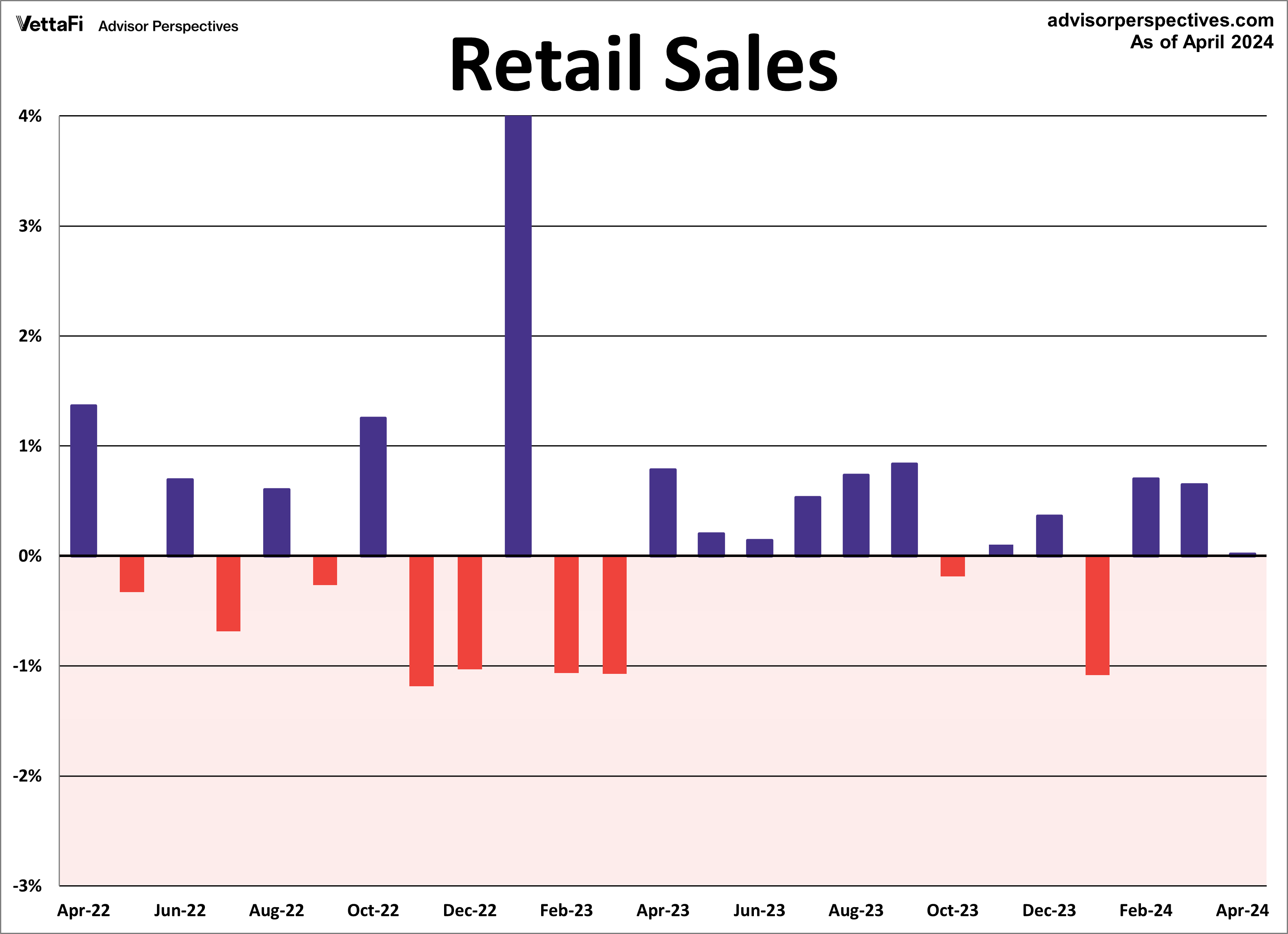

American consumers seem to keep growing more cautious as their spending took an unexpected pause last month. Retail sales were flat in April, lower than the anticipated 0.4% growth. Additionally, March’s growth was revised lower. Consumer spending picked up in a handful of sectors, led by gas stations (3.1%), clothing stores (1.6%), electronic and appliance stores (1.5%), and food and beverages stores (0.8%). Meanwhile, most other sectors saw a drop off in spending.

Core retail sales (excluding automobiles) were up 0.2% from March, as expected. Lastly, control purchases, which is thought to be an even more “core” view of retail sales, were down 0.3% from the previous month. While this series typically does not garner as much attention as the headline and core figures, control purchases are a more consistent and reliable reading of the economy because it strips out many volatile components.

Overall, consumer spending is off to a slower than expected start for 2024 as Americans continue to grabble with inflation and elevated rates. The latest retail sales data is unlikely to cause a major swing in the Fed’s interest rate policy but does bolster views that rate cuts are not completely off the table for this year.

Retail sales will have an impact on the interest in the SPDR S&P Retail ETF (XRT), VanEck Retail ETF (RTH), Amplify Online Retail ETF (IBUY), and ProShares Online Retail ETF (ONLN).

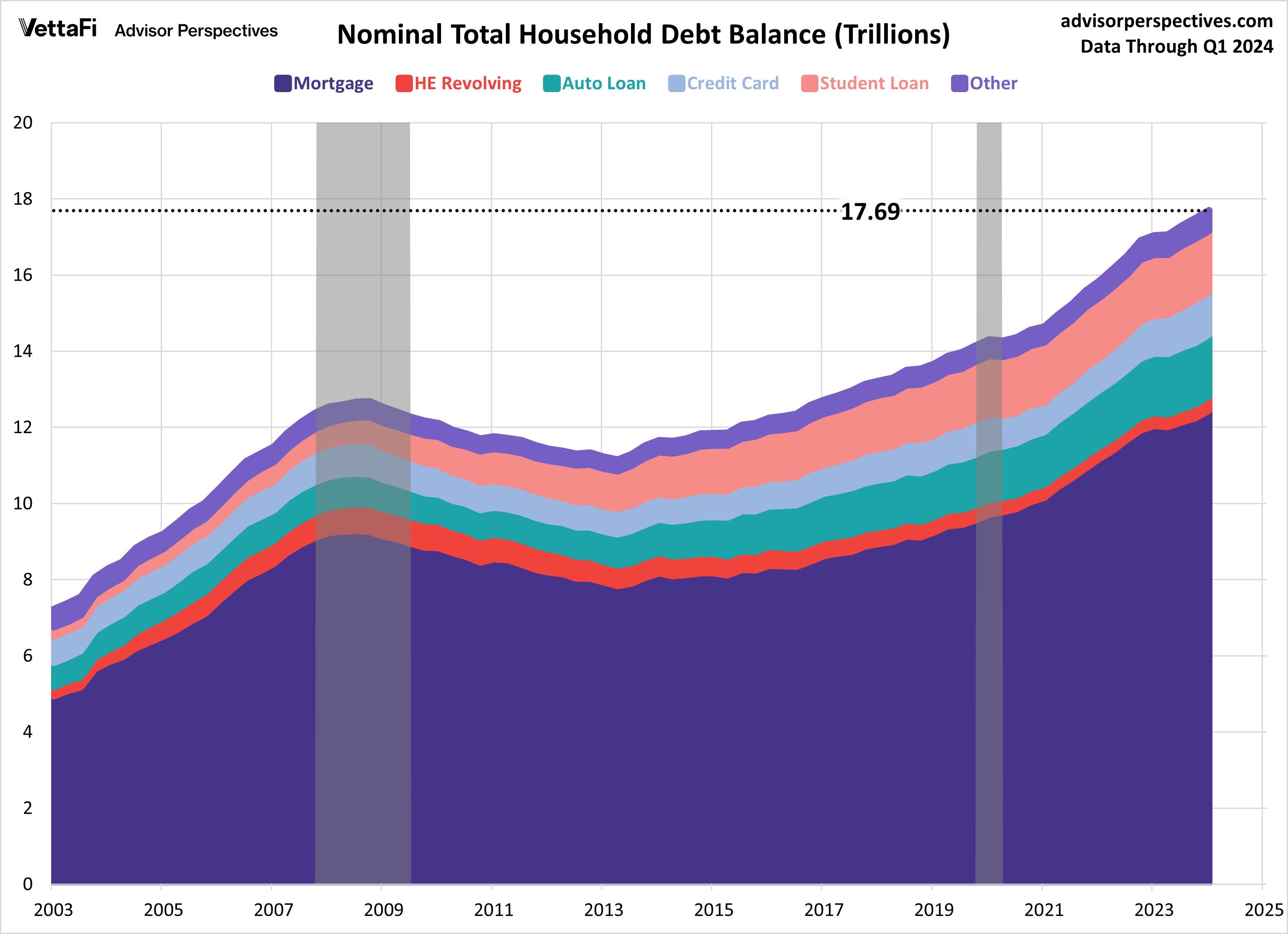

Household Debt and Credit

In the latest quarterly household debt and credit report released by the NY Fed, we saw a $184 billion uptick in household debt, reaching a record $17.69 trillion in Q1 of this year. The latest data represents a 1.09% increase from Q4’s debt level of $17.50 trillion. The first quarter increase was largely driven by mortgage and auto loan balances, which both hit new all-time highs. Specifically, mortgage balances increased $190 billion (1.55%) to $12.442 trillion and auto loan balances increased $9 billion (0.56%) to $1.616 trillion. Meanwhile, credit card and student loan balances both declined in Q1 but remain elevated. This comprehensive report serves as a gauge for the financial conditions of U.S. households, offering insights into their economic well-being.

Economic Indicators and the Week Ahead

This week we will receive data on a few more housing indicators. On Wednesday, the National Association of Realtors will release April’s data on existing home sales followed by the Census Bureau’s release of new home sales data on Thursday. These housing market indicators will have an impact on homebuilders and residential real-estate ETFs such as iShares U.S. Home Construction ETF (ITB), SPDR S&P Homebuilders ETF (XHB), and iShares Residential and Multisector Real Estate ETF (REZ). Existing home sales are projected to inch down to a seasonally adjusted annual rate of 4.18 million units. New home sales are expected to fall to a seasonally adjusted annual rate of 680K units.

Also this week, we will receive the latest consumer sentiment data with the University of Michigan’s consumer sentiment index. On Friday, this month’s final report, which could impact interest in the Consumer Discretionary Select Sector SPDR ETF (XLY), is predicted to remain at May’s preliminary reading of 67.4.

For more news, information, and analysis, visit the Innovative ETFs Channel.