Economic indicators are released every week to provide insight into the overall health and performance of an economy. They serve as essential tools for policymakers, advisors, investors, and businesses. That’s because they allow them to make informed decisions regarding business strategies and financial markets. In the week ending July 25, the SPDR S&P 500 ETF Trust (SPY) fell 2.58%. The Invesco S&P 500® Equal Weight ETF (RSP) was down 1.29%.

This article examines two important economic releases from the past week: Q2 gross domestic product (GDP) and the personal consumption expenditures (PCE) price index. That latter is also known as the Fed’s preferred inflation gauge. These indicators provide insights into the country’s economic landscape. They particularly focus on consumption and its role in economic growth.

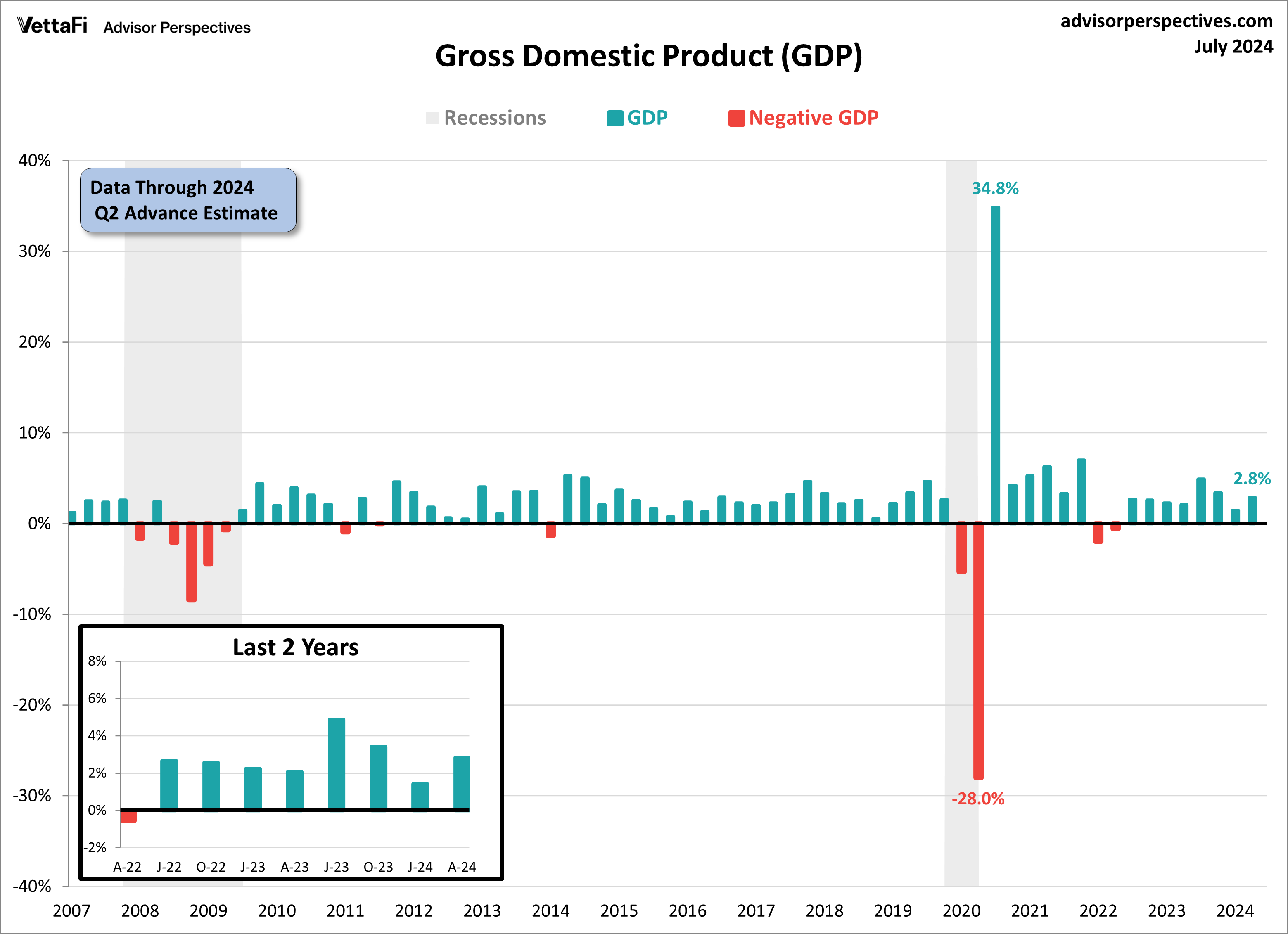

Gross Domestic Product (GDP)

The U.S. economy grew at a stronger-than-anticipated rate in the second quarter, according to the advance estimate for Q2 2024 Gross Domestic Product (GDP). The economy expanded at a rate of 2.8%. That’s twice as fast as the 1.4% growth in Q1 and well above the 2.0% growth forecast. The economy has now expanded for two consecutive years as inflation has cooled. That is boosting hopes that a “soft landing” can be achieved.

In the second quarter, three out of the four subcomponents contributed positively to real GDP. For the fourth consecutive quarter, consumer spending was the largest contributor to economic growth. Business investment also made substantial contributions. That’s specifically so in nonresidential expenditures and inventories, while government spending also contributed to economic growth last quarter. Net exports were the sole negative contributor last quarter as imports, which are a subtraction in the calculation of GDP, increased.

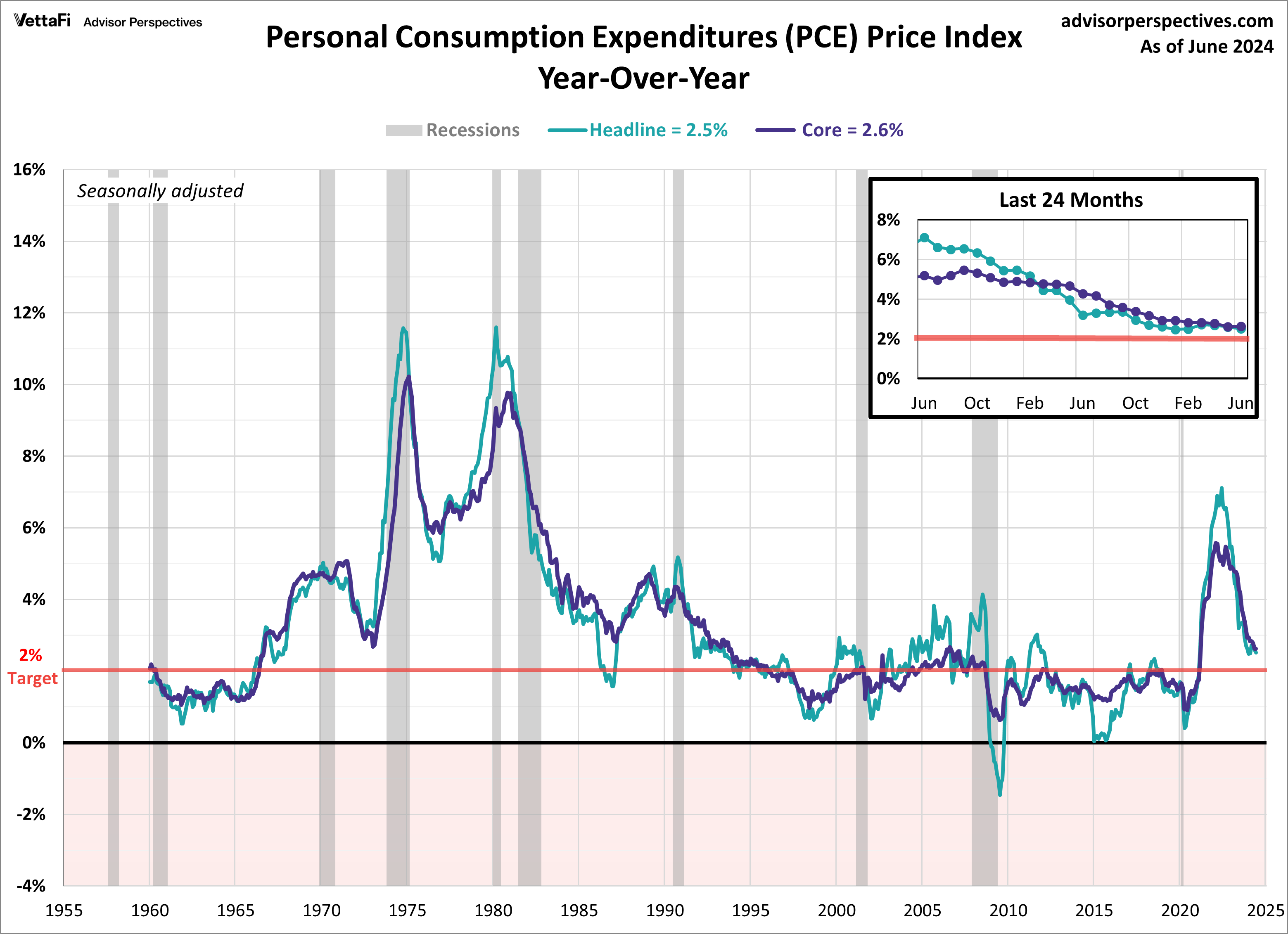

Personal Consumption Expenditures (PCE)

The Fed’s preferred inflation gauge cooled further last month. It is inching closer to the Fed’s 2% target rate. The PCE Price Index rose 2.5% compared to one year ago. That’s the slowest pace since February. Meanwhile, the core PCE price index, which measures inflation excluding volatile food and energy prices, rose 2.6% compared to the previous year. That is remaining at its lowest level since March 2021. On a monthly basis, headline PCE was up 0.1% while core PCE rose 0.2%. Both readings were consistent with their respective forecasts. The latest PCE numbers came in as expected for the most part. They should continue to provide relief that inflation is cooling as it crawls closer to the Fed’s target rate.

Economic Indicators and the Week Ahead

The labor market will be in focus this week as several key job reports will be released. The June JOLTS data and July employment reports will provide insights into the health of the labor market, a vital element of the overall economy. The labor market has been, and will continue to be, closely monitored as it is one of the key drivers behind the Federal Reserve’s policy decisions.

On Tuesday, the Bureau of Labor Statistics will release the latest job openings data where we will see if job openings continue their downward trend or if last month’s surprise uptick repeats. Then on Wednesday, ADP will release their latest employment report that will set the stage for the more comprehensive BLS employment report due on Friday. Expectations are that 185,000 nonfarm jobs were added in July, down from 206,000 in June, and that the unemployment rate remained at 4.1%.

For more news, information, and strategy, visit the Innovative ETFs Channel.