“Turbulence is dangerous. Its output—the pressure or velocity of water, the average or change in price—can swing wildly, suddenly. It is hard to predict, harder to protect against, hardest of all to engineer and profit from. Conventional finance ignores this, of course. It assumes the financial system is a linear, continuous, rational machine. That kind of thinking ties conventional economists into logical knots.”

– Benoit Mandelbrot, Richard L. Hudson The Misbehavior of Markets

The View from 30,000 feet

Last week was Central Bank Week, with decisions from most of the largest central banks, including the U.S., England, Japan, as well as a host of other central banks, such as Switzerland and Sweden. The overarching theme was that the wildfire of inflation sparked by monetary and fiscal responses to the pandemic has been contained but hasn’t stopped burning (spoken like a firefighter). As with most wildfires, once the fire has been contained, the firefighting continues, with the next phase focused on stomping out hot spots and dealing with flareups from unforeseen windstorms and bouts of hot weather that threaten to breach hard fought for parameters. Translating the metaphor into inflationary terms, windstorms and hot weather might equate to spikes in energy prices and potential new supply chain disruptions from the UAW strike. These factors pose serious threats to containment. You have to feel for central bankers, over the last couple years every time it looks like they have policy in place to corral inflation, they get an exogenous shock that calls their plan into question.

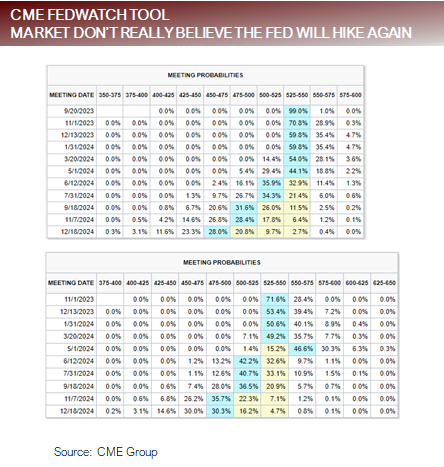

- An uncertain Fed, cautiously points towards the terminal level with less conviction

- Round trip on 2023 returns for broad markets, as the market near a tradeable low

- The difference between Forces and Measurements, and what it means for the markets

- The most Frequently Asked Question from clients this week: What happened to that Three-Legged Stool (earnings, balance sheets, jobs) of yours?

An uncertain Fed, cautiously points towards the terminal level with less conviction

- If you want to get a feel for the Fed’s attitude, there’s no better place to start than listening to the entire press conference and Q&A. It gets even more interesting if you listen to each of the pressors and note the change in tone.

- There was a definite change in tone between the last two The major difference was the increased sense of uncertainty and caution. In fact, Powell used the word uncertain, uncertainties or uncertainty a total of 11 times. In addition, there we multiple references to lacking confidence in the Fed’s modeling.

- The previous pressor provided a sense of optimism about path of At the most recent pressor, there was a loss of optimism and a reiteration of the view that battle against inflation is far from over. This is likely due to the rapid rise in oil prices and the realities that higher energy will likely bleed through to confidence and expectations.

- One of the more interesting comments Powell made was the reference that that consumer sentiment is driven by gas prices, while noting there is very little signal in this information as to the underlying inflationary pressures.

- Powell also noted that if the economy comes in stronger than expected the Fed will have to do more, crushing the no- landing narrative, that was holding out for a better-than-expected economy with no action by the Fed.

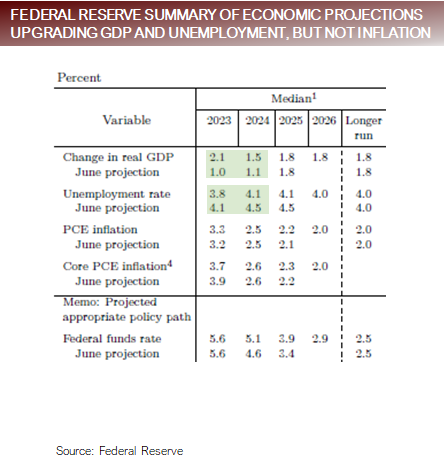

- The most criticized aspect of the revised Summary of Economic Projections was the notion that the economy will accelerate towards close to potential, unemployment will be subdued at near historical lows, yet inflation will continue to drift towards the Fed’s It seems unlikely that with an acceleration in the growth side of the economy inflation will cool without the Fed continuing to pressure rates higher, and also contradicts the Fed’s previous guidance that the economy will need a period of below trend growth to bring inflation inline with the Fed’s target.

Post meeting the market re-price for fewer cuts and a longer duration of higher rates

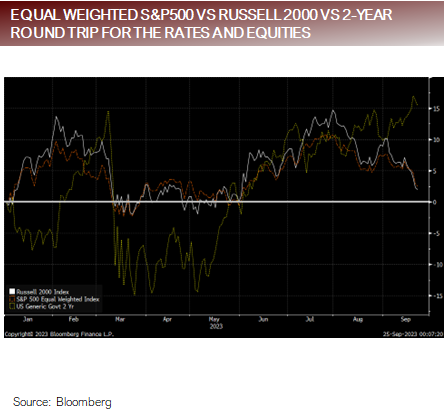

Round trip on 2023 returns for broad markets, as the market near a tradeable low

- The broader markets have quietly erased nearly all their gains in

- Equal Weighted S&P500 YTD: +2.49%

- Russell 2000 YTD: +1.95%

- The 2-Year Treasury peaked in Q1 on 3/8/23 at 07. At that time both the Equal Weighted S&P500 and the Russell 2000 were negative on the year. By May, the 2-Year Treasury had fallen to 3.79, setting off a rally in equities with the Equal Weighted S&500 rising +10.8% in May and the Russell 2000 rising +14.7%. Last week the 2-Year Treasury took out the March high closing at 5.18, creating a down draft in equities sending the broad market close to the lows of the year.

- As with 2022, the equity markets appear to be following where interest rates lead.

- The 3m10y yield curve troughed on 5/3/23 at -190 and currently stands at -96. Historically, the yield curve has been one of the best predictors of a recession, with a pattern that it inverts 6 to 24 months before a recession and then de-inverts as the recession is The de-inversion is a signal that a slowdown is coming.

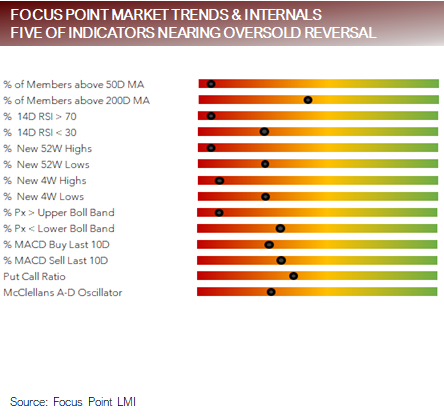

- Our Market Internals model, which measures short-term over-bought/over-sold levels has 5 out of 14 of the indicators within striking distance from reaching a tradeable low. Historically, when over half of the indicators in the model show a tradeable low, we reach selling exhaustion, making room for a relief rally. Although none of the indicators are signaling a tradeable low, another wave a selling may be enough to trigger a signal. As always, past performance is not a guarantee of future performance. If we do get a tradeable low signal, investors will need be extremely agile because the yield curve is signaling there is economic weakness that will follow.

Equity market being pushed around by rates approaching deeply oversold levels

The difference between Forces and Measurements, and what it means for the markets

- Forces represent the underlying policy, social, technological and political drivers that generate economic outcomes that trickle into the financial

- Measurements are the manifestations of the Forces in the underlying economic and market data that is

- Examples of Forces

- Consumers who have been able to stretch pandemic savings

- Wages that have been rising faster than goods prices

- Falling demand for goods (post-pandemic stuff hangover) combined with increased demand for services (YOLO)

- The continuation of massive deficit spending

- Companies’ hording employees for fear of not being able to hire

- Cost of Living Adjustments driving excess spending power for retirees

- Work from home changing living and consumption patterns

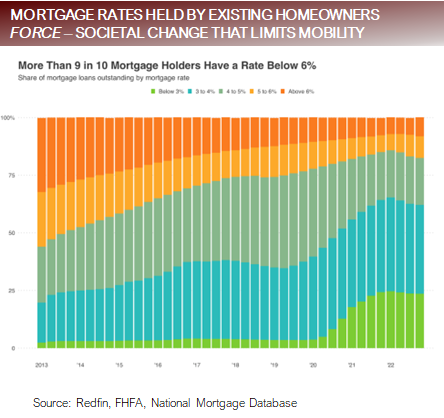

- Homeowners locked in ultra-low rates just before a historic move higher, creating in unwillingness to sell and refinance at higher rates

- AI frenzy driving FOMO in the magnificent 7

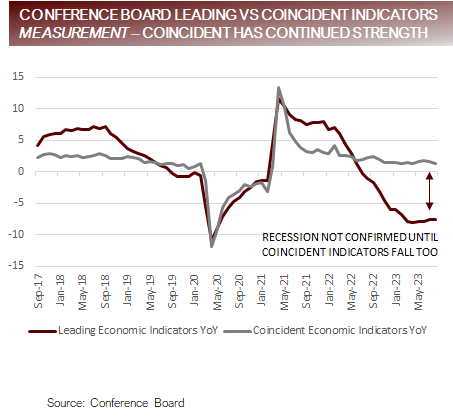

- Examples of Measurements

- Leading indicators failing to be confirmed by coincident indicators

- Manufacturing data weakening, while services data accelerates strong

- Savings rates falling signaling that consumers have confidence in employment and balance sheets

- Historically low unemployment rates

- Nominal retail sales remaining strong while unit volumes falling

Examples of Forces and Measurements

FAQ: What happened to that Three-Legged Stool (earnings, balance sheets, jobs) of yours?

- As a refresher, our argument has been that a material economic slowdown would be delayed as long as what we called, the Three-Legged Stool (jobs, earnings and balance sheets) provided a buffer from the impacts of rising rates.

- Earnings

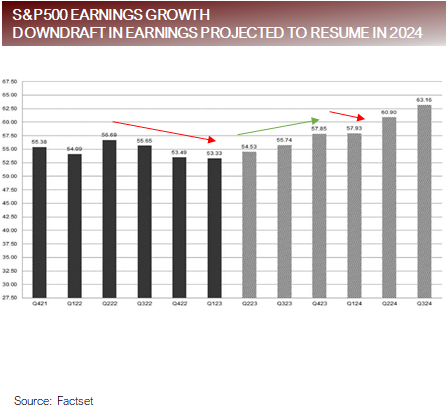

- Sequential quarterly earnings peaked in Q2 2022 and continued to fall until Q1 The downdraft in sequential quarterly earnings growth was accompanied by weak financial markets. According to analyst estimates, sequential quarterly earnings growth is set to rise until Q1 2024, when they begin a brief retreat. The financial markets tend to struggle when earnings are falling, indicating that another round of financial market softness may be ahead in 2024.

- Balance Sheets

- Excess savings that resulted from government pandemic policy responses has provided extra cushion for consumers and companies. After peaking at nearly $2.5t in excess savings, recent data from the San Francisco Fed indicates that as of Q2 2024, the excess savings has dwindled to around $500b and falling. Although this is still a lot of cushion, because it’s distributed unevenly among income cohorts, there may be a sharp fall in spending when excess savings hits its downward limit.

- Jobs

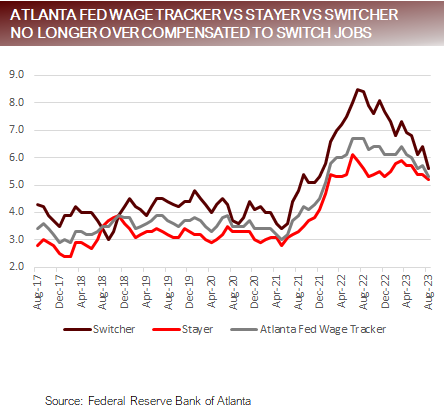

- Employment was impacted by several major forces. First, the evaporation of nearly 6m people out of the labor force. Second, companies concerned about hiring, began hoarding Third, as wages rose because of these forces, employees were incentivized to switch jobs. There are signs that these dynamics are shifting. According to the Atlanta Fed Wage Tracker, there is no longer a premium for workers to shift jobs. As a result of workers staying put, job openings are beginning to fall.

The final leg of the stool, jobs, is changing in front of another wave of projected earnings weakness

Putting it all together

- We’ve called the current market condition, the Picking Up Nickels in Front of a Steamroller While it’s true economic momentum continues to be driven by post-pandemic and reopening Forces. There are subtle shifts in data indicating that some of the Forces, specifically those related to jobs, are finally changing.

- It’s possible that the current momentum in the economy and residual Forces that have driven stronger than expected growth and financial market strength carries us past the rough patch caused by shifting Forces. However, it’s not It’s likely a function of how many Forces change at the same time.

- With what appears to be a convergence in weaker earnings in Q1 2024, excess savings dwindling and signs that the Forces that drove a strong labor market dissipating, there are warnings lights that are beginning for flash that the next soft patch may involve some pain.

- However, in the short-term, the markets are approaching a deeply oversold condition provides a set up for a Q4 rally, which coincides with seasonal However, investors should be careful as they step in to pick up those nickels of gains in Q4 because the Forces that are driving the steamroller appear to be gathering momentum of their own.

For more news, information, and analysis, visit the Innovative ETFs Channel.

DISCLOSURES AND IMPORTANT RISK INFORMATION

Performance data quoted represents past performance, which is not a guarantee of future results. No representation is made that a client will, or is likely to, achieve positive returns, avoid losses, or experience returns similar to those shown or experienced in the past.

Focus Point LMI LLC

For more information, please visit www.focuspointlmi.com or contact us at [email protected] Copyright 2023, Focus Point LMI LLC. All rights reserved.

The text, images and other materials contained or displayed on any Focus Point LMI LLC Inc. product, service, report, e-mail or web site are proprietary to Focus Point LMI LLC Inc. and constitute valuable intellectual property and copyright. No material from any part of any Focus Point LMI LLC Inc. website may be downloaded, transmitted, broadcast, transferred, assigned, reproduced or in any other way used or otherwise disseminated in any form to any person or entity, without the explicit written consent of Focus Point LMI LLC Inc. All unauthorized reproduction or other use of material from Focus Point LMI LLC Inc. shall be deemed willful infringement(s) of Focus Point LMI LLC Inc. copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Focus Point LMI LLC Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Focus Point LMI LLC Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.

All unauthorized use of material shall be deemed willful infringement of Focus Point LMI LLC Inc. copyright and other proprietary and intellectual property rights. While Focus Point LMI LLC will use its reasonable best efforts to provide accurate and informative Information Services to Subscriber, Focus Point LMI LLC but cannot guarantee the accuracy, relevance and/or completeness of the Information Services, or other information used in connection therewith. Focus Point LMI LLC, its affiliates, shareholders, directors, officers, and employees shall have no liability, contingent or otherwise, for any claims or damages arising in connection with (i) the use by Subscriber of the Information Services and/or (ii) any errors, omissions or inaccuracies in the Information Services. The Information Services are provided for the benefit of the Subscriber. It is not to be used or otherwise relied on by any other person. Some of the data contained in this publication may have been obtained from The Federal Reserve, Bloomberg Barclays Indices; Bloomberg Finance L.P.; CBRE Inc.; IHS Markit; MSCI Inc. Neither MSCI Inc. nor any other party involved in or related to compiling, computing or creating the MSCI Inc. data makes any express or implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of such data. Such party, its affiliates and suppliers (“Content Providers”) do not guarantee the accuracy, adequacy, completeness, timeliness or availability of any Content and are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, or for the results obtained from the use of such Content. In no event shall Content Providers be liable for any damages, costs, expenses, legal fees, or losses (including lost income or lost profit and opportunity costs) in connection with any use of the Content. A reference to a particular investment or security, a rating or any observation concerning an investment that is part of the Content is not a recommendation to buy, sell or hold such investment or security, does not address the suitability of an investment or security and should not be relied on as investment advice.

This communication reflects our analysts’ current opinions and may be updated as views or information change. Past results do not guarantee future performance. Business and market conditions, laws, regulations, and other factors affecting performance all change over time, which could change the status of the information in this publication. Using any graph, chart, formula, model, or other device to assist in making investment decisions presents many difficulties and their effectiveness has significant limitations, including that prior patterns may not repeat themselves and market participants using such devices can impact the market in a way that changes their effectiveness. Focus Point LMI LLC believes no individual graph, chart, formula, model, or other device should be used as the sole basis for any investment decision. Focus Point LMI LLC or its affiliated companies or their respective shareholders, directors, officers and/or employees, may have long or short positions in the securities discussed herein and may purchase or sell such securities without notice. Neither Focus Point LMI LLC nor the author is rendering investment, tax, or legal advice, nor offering individualized advice tailored to any specific portfolio or to any individual’s particular suitability or needs. Investors should seek professional investment, tax, legal, and accounting advice prior to making investment decisions. Focus Point LMI LLC’s publications do not constitute an offer to sell any security, nor a solicitation of an offer to buy any security. They are designed to provide information, data and analysis believed to be accurate, but they are not guaranteed and are provided “as is” without warranty of any kind, either express or implied.

FOCUS POINT LMI LLC DISCLAIMS ANY AND ALL EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY, SUITABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE.

Focus Point LMI LLC, its affiliates, officers, or employees, and any third-party data provider shall not have any liability for any loss sustained by anyone who has relied on the information contained in any Focus Point LMI LLC publication, and they shall not be liable to any party for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including, without limitation, lost income or lost profits and opportunity costs) in connection with any use of the information or opinions contained Focus Point LMI LLC publications even if advised of the possibility of such damages.