“… after the laws of physics, everything else is opinion.“

— Neil deGrasse Tyson, Astrophysics for People in a Hurry

The View From 30,000 Feet

Last week was a continuation of the major themes that have marked the fourth quarter: A softening of the labor markets, a downshifting in the trajectory of growth, a slowdown in inflationary pressures and a Federal Reserve that is coming around to the view that they have crested the top in rates and may be looking towards beginning normalization in the new year.

These themes have opened the door for risk assets to appreciate in anticipation that the coming slowdown will resemble a gradual decline towards the mean (soft-landing), versus the more typical non-linear decent through the mean that has more typically been associated with interest rate hiking cycles (hard-landing).

This week we provide our outlook for 2024, which doesn’t focus one case as the primary possibility, but rather outlines what we see as the possible outcomes and probabilities for each. We believe it will be very difficult to forecast the exact route, because the outcomes will ultimately depend on variables that interact with each other based on the strength of feedback loops that are created. As the economy progresses through the new year, we anticipate the exact glide path will become clearer, and as that happens the probabilities will begin to shift towards one of the potential scenarios.

- Inflation, employment, growth and Fed rhetoric all feeding the soft-landing story

- Focus Point Leading Market Indicator signals Neutral Conditions

- 2024 Outlook – Scenarios and Probability Estimates

- What to watch in 2024 for hints of which scenario is unfolding

Inflation, Employment, Growth, Fed Rhetoric Feeding Soft-Landing Story

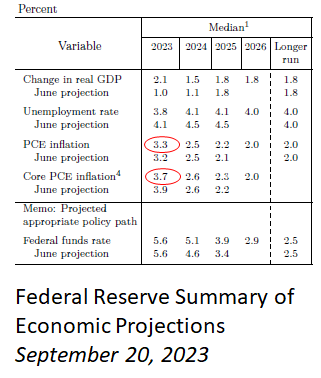

- PCE, the Fed’s preferred measure for inflation, surprised to the downside with the headline number measuring flat month-over-month, and the year-over-year now below the Fed’s most recent Summary of Economic

- Headline CPE YoY 0%

- Core CPE 5%

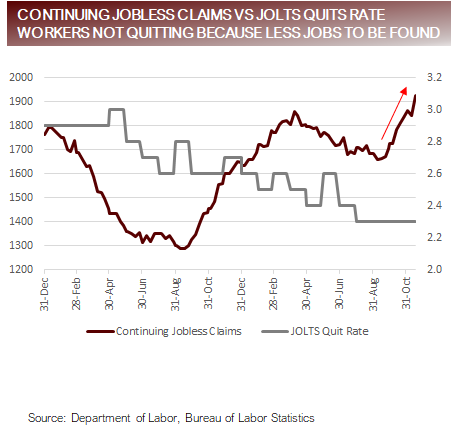

- Continuing Jobless Claims hit 1927k, extending to the highest level since the interrupting the downward trend, and up 200k over the last 6 weeks, the second highest 6 week rise since the pandemic.

- ISM Purchasing Manager Survey Employment component surprised to the downside hitting the second lowest level since the post-pandemic recovery

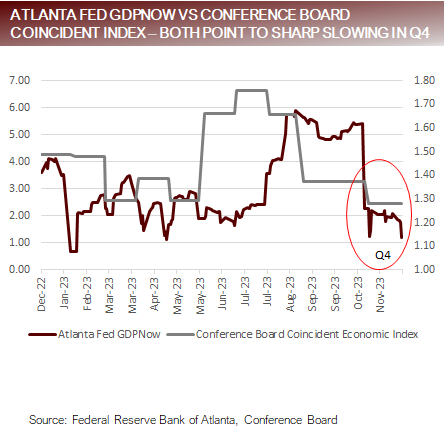

- The Atlanta Fed GDPNow forecast is now projecting 19% GDP growth for the Q4 and Conference Board’s Coincident Index measured 1.28% YoY, touching its lowest level post-pandemic, signaling a sharp cooling of activity in Q4.

- Fed President Waller, who had previously been known to be a hawk, ignited a rally with is speech titled, “Something Appears to be Giving”, which is in stark contrast to his speech in October, titled “Something’s Got to Give.”

Fed’s Getting Its Wish List: Cooling Growth, Tightening Labor Market

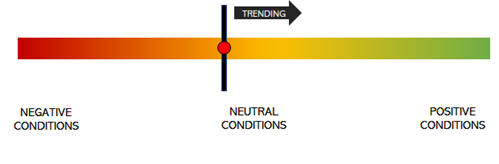

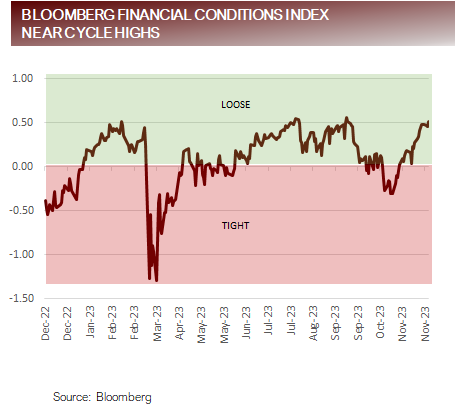

Focus Point Leading Market Indicator Signals Neutral Conditions

QUANTITATIVE VIEW: The Focus Point Leading Market Indicator (LMI), signaled Neutral Conditions for December, as looser financial conditions, tighter credits spreads and resilient earnings – versus expectations – combined with strengthening technicals to nudge the model forward.

QUALITATIVE VIEW: With rates restrictive, growth and employment both deteriorating, and market expectations for the Fed to embark on an aggressive rate cutting campaign in 2024, financial markets are primed for disappointment if the growth slowdown trickles into earnings, or the Fed doesn’t deliver on expectations.

High Frequency Data Signaling Risk Environment Strong, Despite Deteriorating Fundamental Data

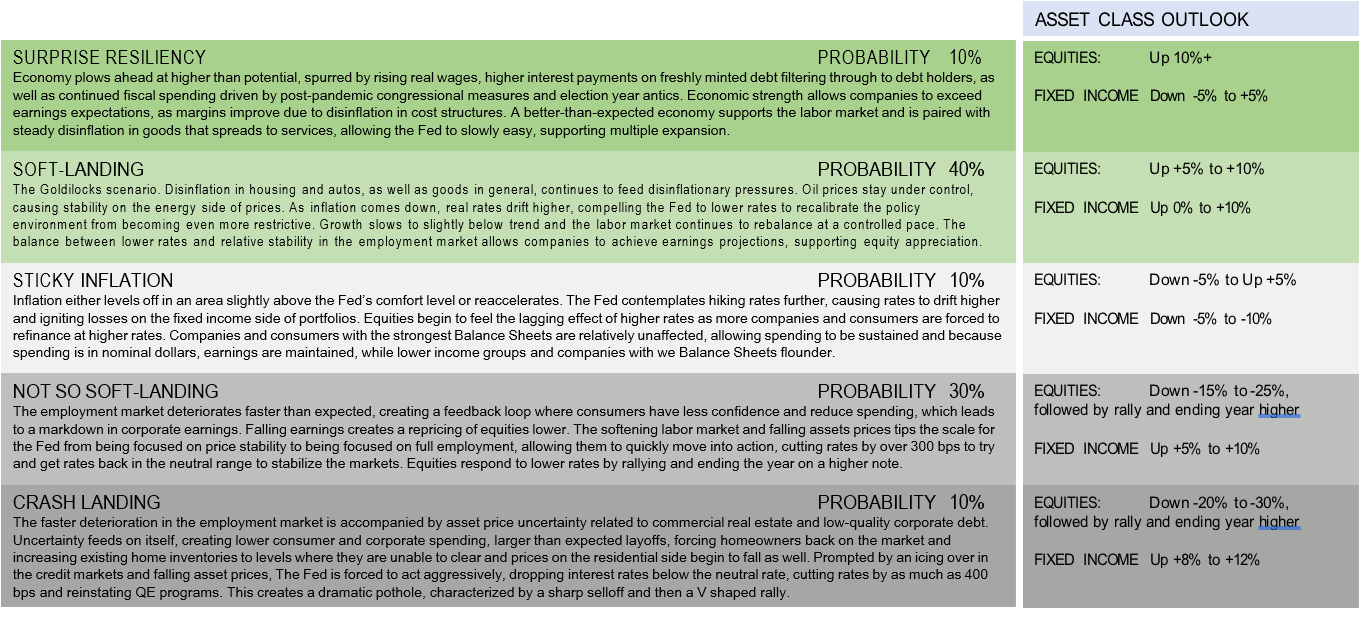

2024 Outlook – Scenarios and Probability Estimates

Takeaways From 2024 Outlook

- Although the probabilities are roughly evenly split between financial markets that trend higher, on a relatively smooth course versus bumper outcomes with more variability, volatility and drawdowns, the upside/downside return disparity is tipped towards more pain to the downside in the negative Said another way, we expect the drawdowns from the negatively weighted outcomes in the lower half to exceed the upside from outcomes in those that are positively weighted. However, we do anticipate that in the event of most negative outcome scenarios related to slowdowns, the policy response should ultimately drive higher returns for risk assets.

- There are three main things to keep in mind that should make investors wary of the path of potential outcomes for 2024:

-

- Rates are restrictive

- The majority of data from historical analogs indicate that soft-landings when rates are restrictive are hard to come by

- The Fed would rather risk a recession than risk a recurrence of inflation (what does Powell want his legacy to be?)

- The investment implications include maintaining risk asset exposure but hedging or remaining nimble and aware of which way the data is As data rolls in, the probabilities will migrate between scenarios and potential outcomes for asset values.

What to Watch in 2024 for Hints of Which Scenario Is Unfolding

- The Fed has a dual mandate: Fully Employment (growth) and Price Stability (inflation), with a tacit third, and overarching, mandate of Financial Things to watch out for in the coming year are those things that drive the Fed’s mandates.

-

- Labor Markets

- Credit Conditions and Use of Credit

- Consumer Spending

- Depletion of Excess Savings

- Housing

- Commercial Real Estate

- Corporate Credit Health

- Oil Prices

- Goods and Services Supply and Demand

- Supply Chain Pressures

- Other data and events that are likely to influence the markets in 2024

-

- Demand for Government Bonds

- Geopolitical Events

- U.S. Election

- Investment Themes

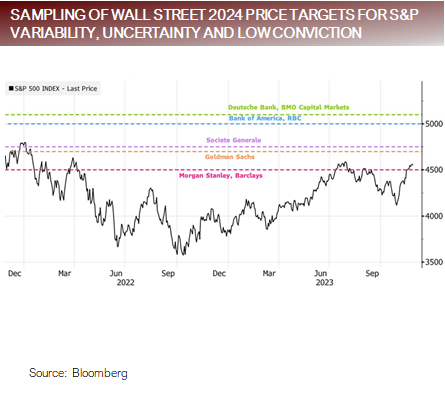

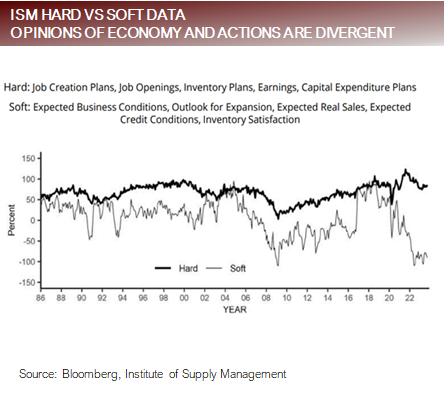

Wall Street Expectations Across the Spectrum, Driven Partially by Survey vs Hard Data Divergence

Putting It All Together

- The risk asset rally of 2023 has been driven by a host of factors but there were two that stood out:

- Excess consumer and corporate savings

- The Artificial Intelligence investment theme and the Magnificent 7 effect

- Going into 2024 the two main drivers of 2023 are unlikely to repeat.

- Pandemic savings on consumer Balance Sheets peaked between $2.0t and $2.5t, and now probably stand at somewhere between $500b and $800b. Saving are being drawn down by $50b to $60b per month, with the lower income cohorts likely already exhausted.

- Although AI will to be a continuing theme in 2024. The average return of the Magnificent 7 for 2023 currently stands at 101% though the close on Friday. It is very unlikely that there will be a repeat of this performance in 2024.

- Although there are potential scenarios that provide for positive outcomes in 2024, it bears reiterating that restrictive rate environments have historically caused recessions, with very few instances where this was not the case. Although it has become fashionable to forecast a soft-landing, investors should be aware a soft-landing is betting against the odds based on how things have typically played out in the past.

- The soft-landing narrative is predicated on the notion that the data that is currently falling towards the mean will level off near the mean with a little help from the Fed. Although this is always plausible, it is also plausible that the data falls through the mean, as it has done in the majority of past analogs. This is why we see Wall Street strategist falling on either side of the argument.

DISCLOSURES AND IMPORTANT RISK INFORMATION

Performance data quoted represents past performance, which is not a guarantee of future results. No representation is made that a client will, or is likely to, achieve positive returns, avoid losses, or experience returns similar to those shown or experienced in the past.

Focus Point LMI LLC

For more information, please visit www.focuspointlmi.com or contact us at [email protected] Copyright 2023, Focus Point LMI LLC. All rights reserved.

The text, images and other materials contained or displayed on any Focus Point LMI LLC Inc. product, service, report, e-mail or web site are proprietary to Focus Point LMI LLC Inc. and constitute valuable intellectual property and copyright. No material from any part of any Focus Point LMI LLC Inc. website may be downloaded, transmitted, broadcast, transferred, assigned, reproduced or in any other way used or otherwise disseminated in any form to any person or entity, without the explicit written consent of Focus Point LMI LLC Inc. All unauthorized reproduction or other use of material from Focus Point LMI LLC Inc. shall be deemed willful infringement(s) of Focus Point LMI LLC Inc. copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Focus Point LMI LLC Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Focus Point LMI LLC Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.

All unauthorized use of material shall be deemed willful infringement of Focus Point LMI LLC Inc. copyright and other proprietary and intellectual property rights. While Focus Point LMI LLC will use its reasonable best efforts to provide accurate and informative Information Services to Subscriber, Focus Point LMI LLC but cannot guarantee the accuracy, relevance and/or completeness of the Information Services, or other information used in connection therewith. Focus Point LMI LLC, its affiliates, shareholders, directors, officers, and employees shall have no liability, contingent or otherwise, for any claims or damages arising in connection with (i) the use by Subscriber of the Information Services and/or (ii) any errors, omissions or inaccuracies in the Information Services. The Information Services are provided for the benefit of the Subscriber. It is not to be used or otherwise relied on by any other person. Some of the data contained in this publication may have been obtained from The Federal Reserve, Bloomberg Barclays Indices; Bloomberg Finance L.P.; CBRE Inc.; IHS Markit; MSCI Inc. Neither MSCI Inc. nor any other party involved in or related to compiling, computing or creating the MSCI Inc. data makes any express or implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of such data. Such party, its affiliates and suppliers (“Content Providers”) do not guarantee the accuracy, adequacy, completeness, timeliness or availability of any Content and are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, or for the results obtained from the use of such Content. In no event shall Content Providers be liable for any damages, costs, expenses, legal fees, or losses (including lost income or lost profit and opportunity costs) in connection with any use of the Content. A reference to a particular investment or security, a rating or any observation concerning an investment that is part of the Content is not a recommendation to buy, sell or hold such investment or security, does not address the suitability of an investment or security and should not be relied on as investment advice.

This communication reflects our analysts’ current opinions and may be updated as views or information change. Past results do not guarantee future performance. Business and market conditions, laws, regulations, and other factors affecting performance all change over time, which could change the status of the information in this publication. Using any graph, chart, formula, model, or other device to assist in making investment decisions presents many difficulties and their effectiveness has significant limitations, including that prior patterns may not repeat themselves and market participants using such devices can impact the market in a way that changes their effectiveness. Focus Point LMI LLC believes no individual graph, chart, formula, model, or other device should be used as the sole basis for any investment decision. Focus Point LMI LLC or its affiliated companies or their respective shareholders, directors, officers and/or employees, may have long or short positions in the securities discussed herein and may purchase or sell such securities without notice. Neither Focus Point LMI LLC nor the author is rendering investment, tax, or legal advice, nor offering individualized advice tailored to any specific portfolio or to any individual’s particular suitability or needs. Investors should seek professional investment, tax, legal, and accounting advice prior to making investment decisions. Focus Point LMI LLC’s publications do not constitute an offer to sell any security, nor a solicitation of an offer to buy any security. They are designed to provide information, data and analysis believed to be accurate, but they are not guaranteed and are provided “as is” without warranty of any kind, either express or implied.

FOCUS POINT LMI LLC DISCLAIMS ANY AND ALL EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY, SUITABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE.

Focus Point LMI LLC, its affiliates, officers, or employees, and any third-party data provider shall not have any liability for any loss sustained by anyone who has relied on the information contained in any Focus Point LMI LLC publication, and they shall not be liable to any party for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including, without limitation, lost income or lost profits and opportunity costs) in connection with any use of the information or opinions contained Focus Point LMI LLC publications even if advised of the possibility of such damages.