By: BCM Investment Team

Supply chain issues are pushing up producer prices and driving inflationary pressures; though CPI came in below expectations, the median month-over-month gain hit a multi-year high. But how useful are headline figures in these still-very-much-unprecedented times? Consumer sentiment has appeared to sour somewhat as the Delta variant hit pause on a return toward normalcy, but consumer credit growth indicates some lingering optimism. The Nasdaq 100 meanwhile notched a new all-time high in a show of strength from large-cap tech—and its profit margins—as smaller companies and the yield curve stick to smaller moves. And finally, what’s going on in China’s housing market and could it lead to more trouble ahead?

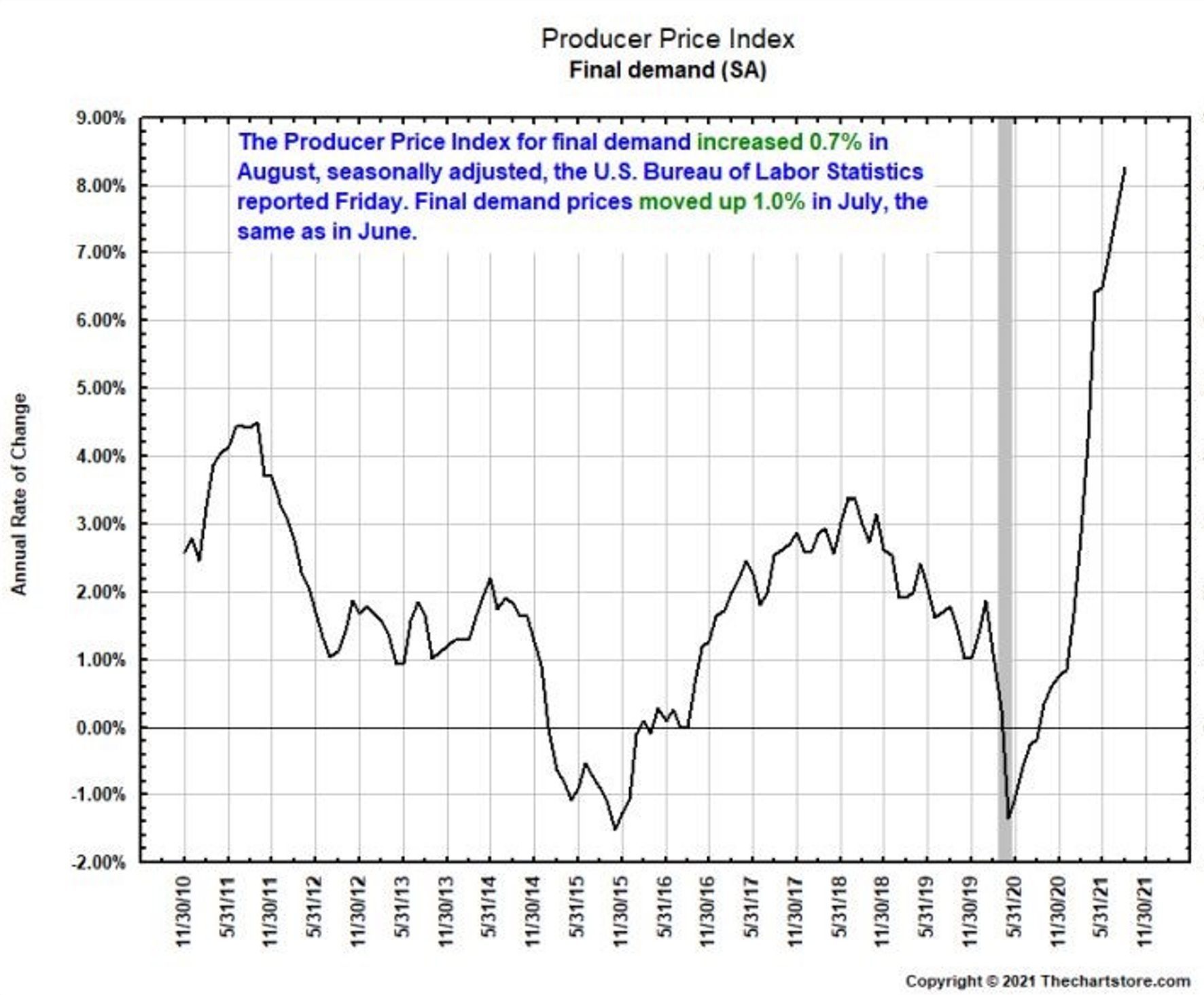

- Inflationary forces are at work in producer prices, hopefully supply chain issues prove to be temporary.

Source: The Chart Store, from 9/152/21

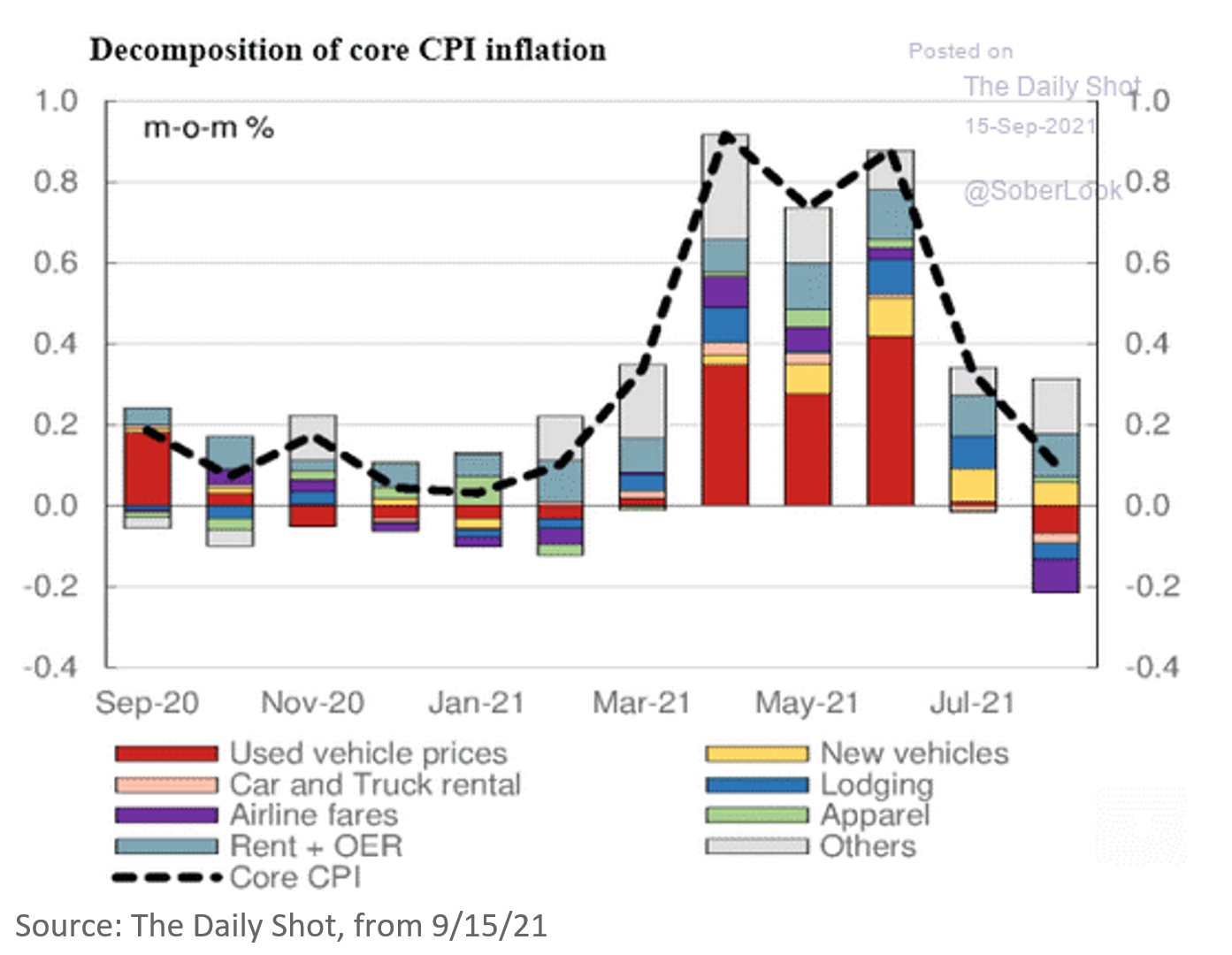

- Headline CPI isn’t a very useful metric due to the aforementioned supply chain issues.

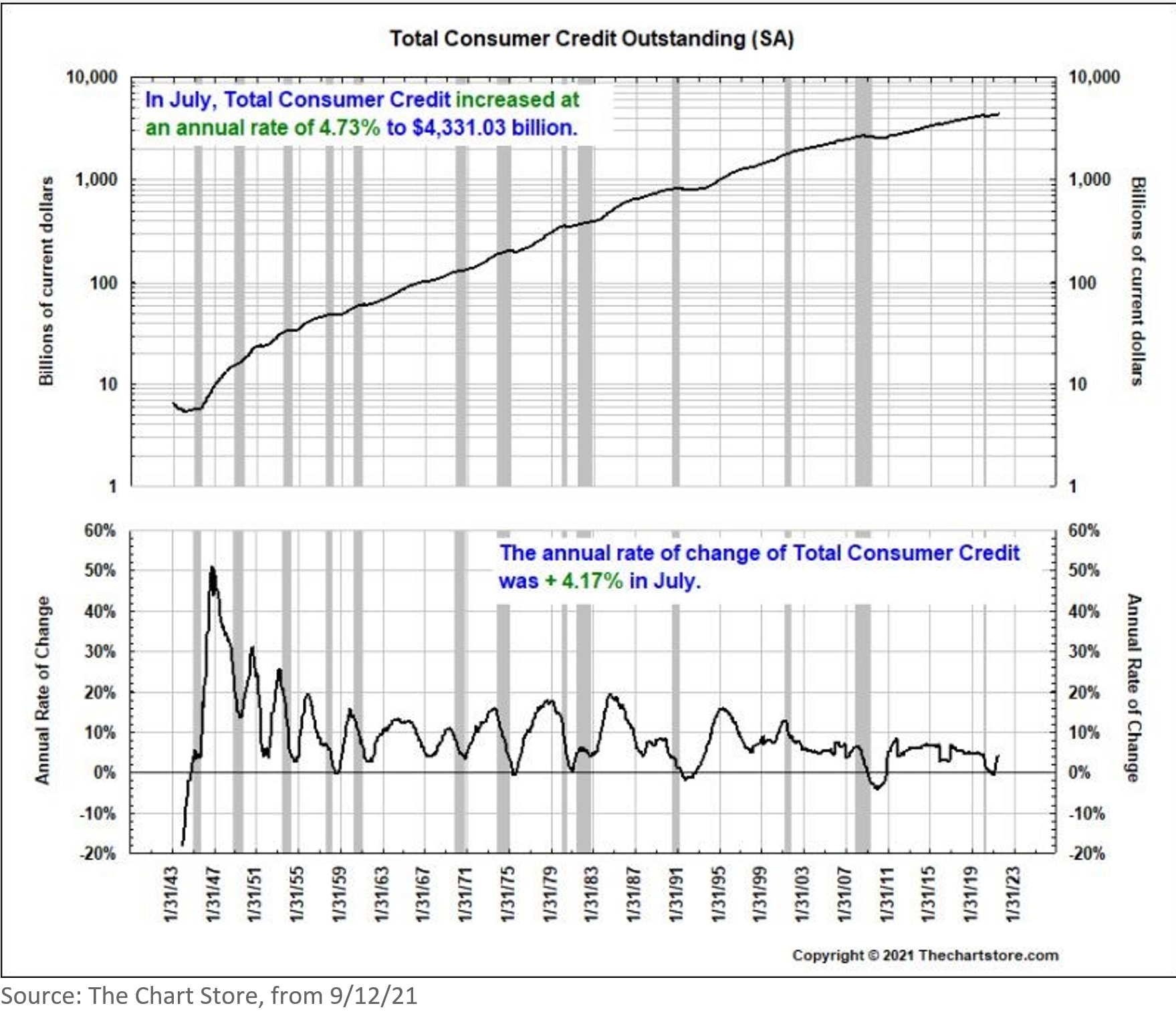

- Consumer credit is beginning to grow again, potentially a sign of confidence in the economy.

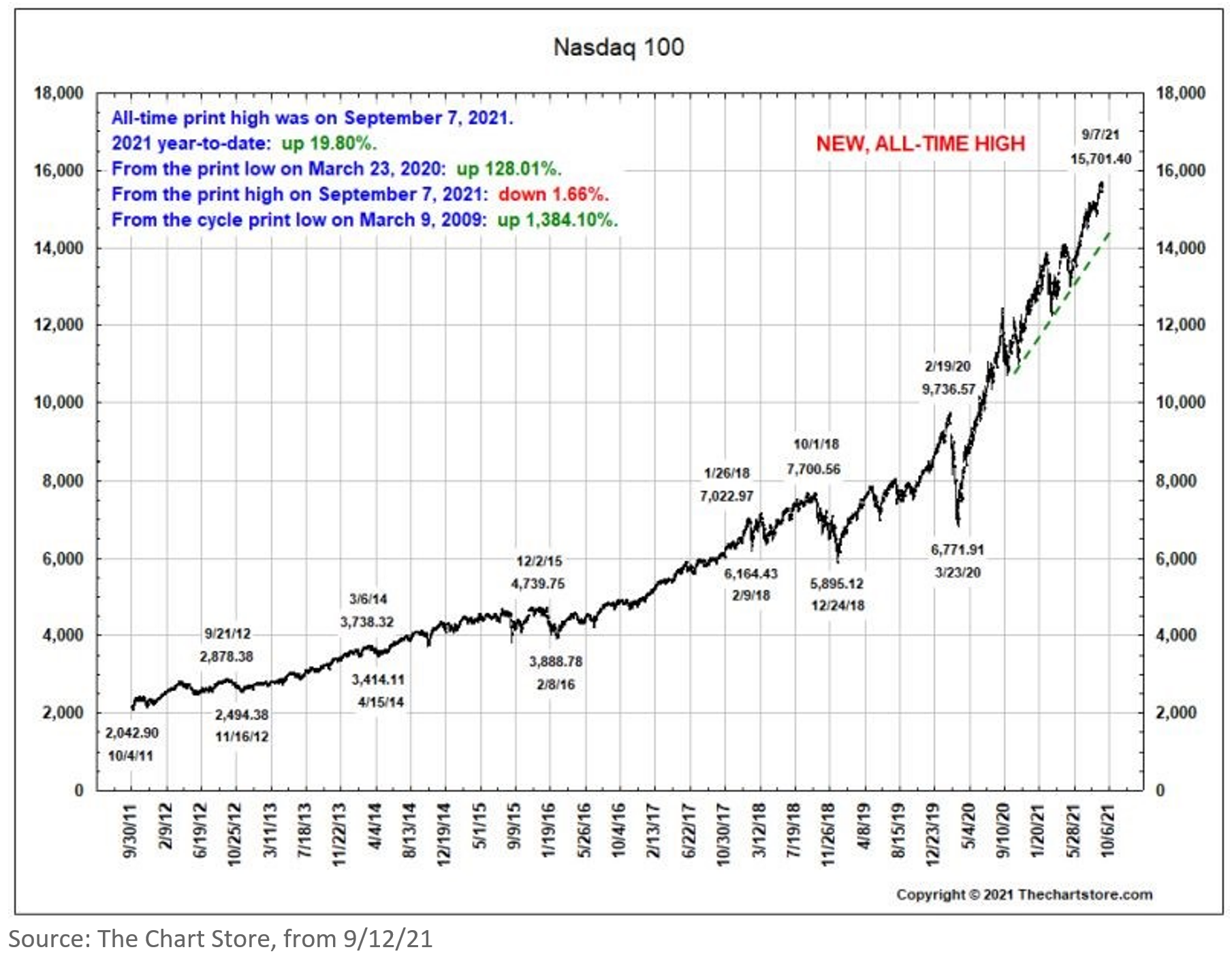

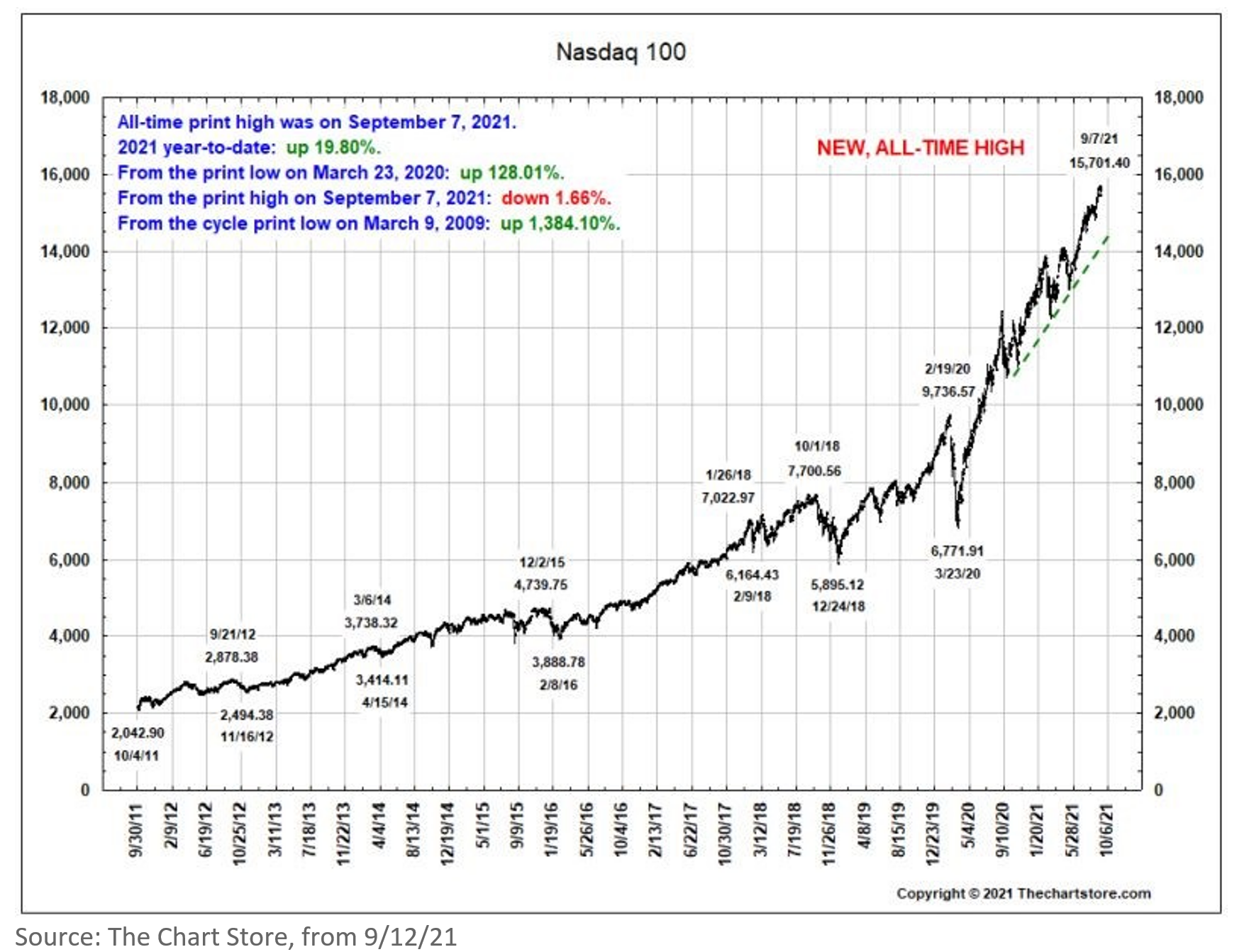

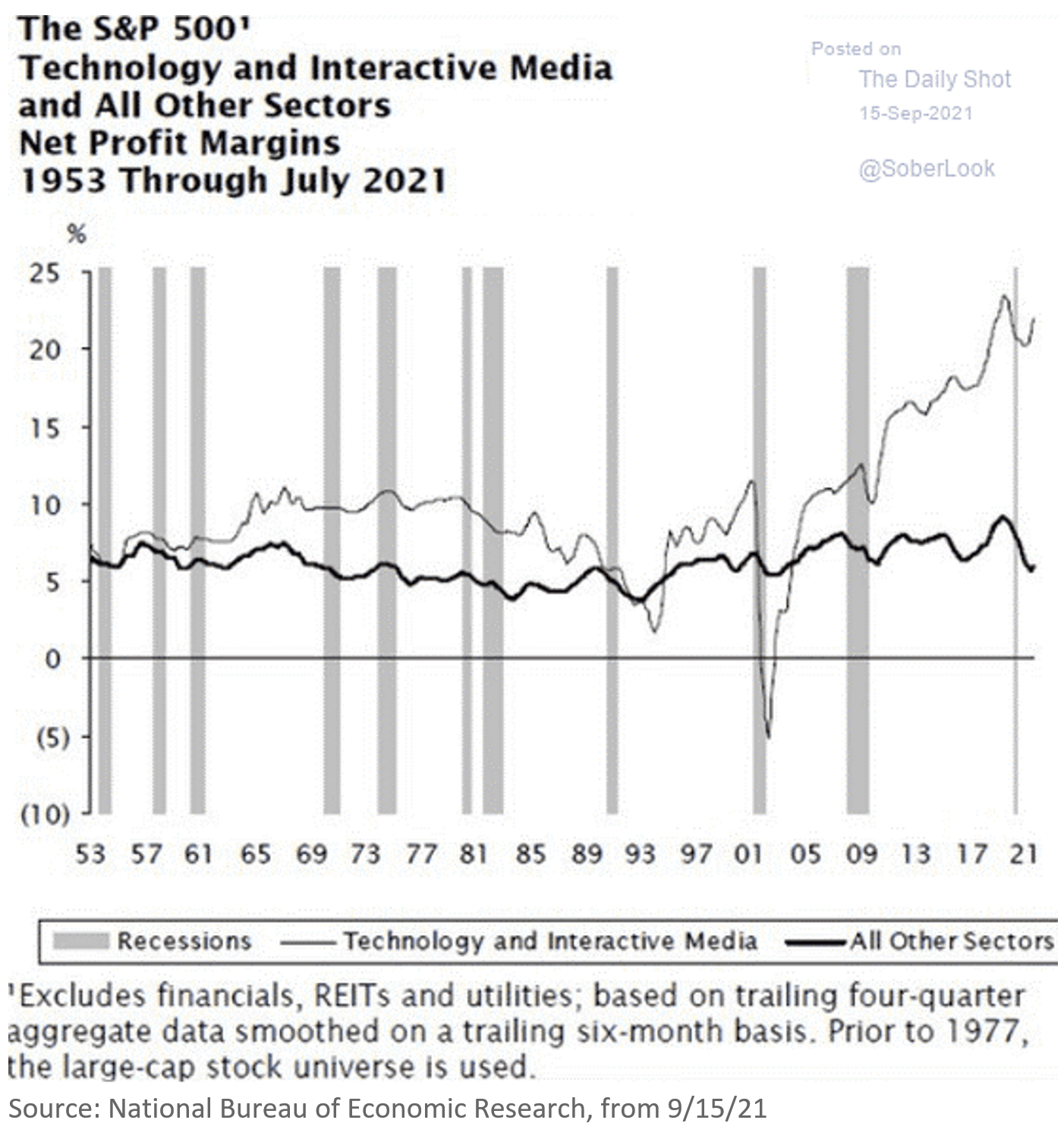

- Large-cap technology continues to make new all-time highs.

- While smaller companies have traded sideways.

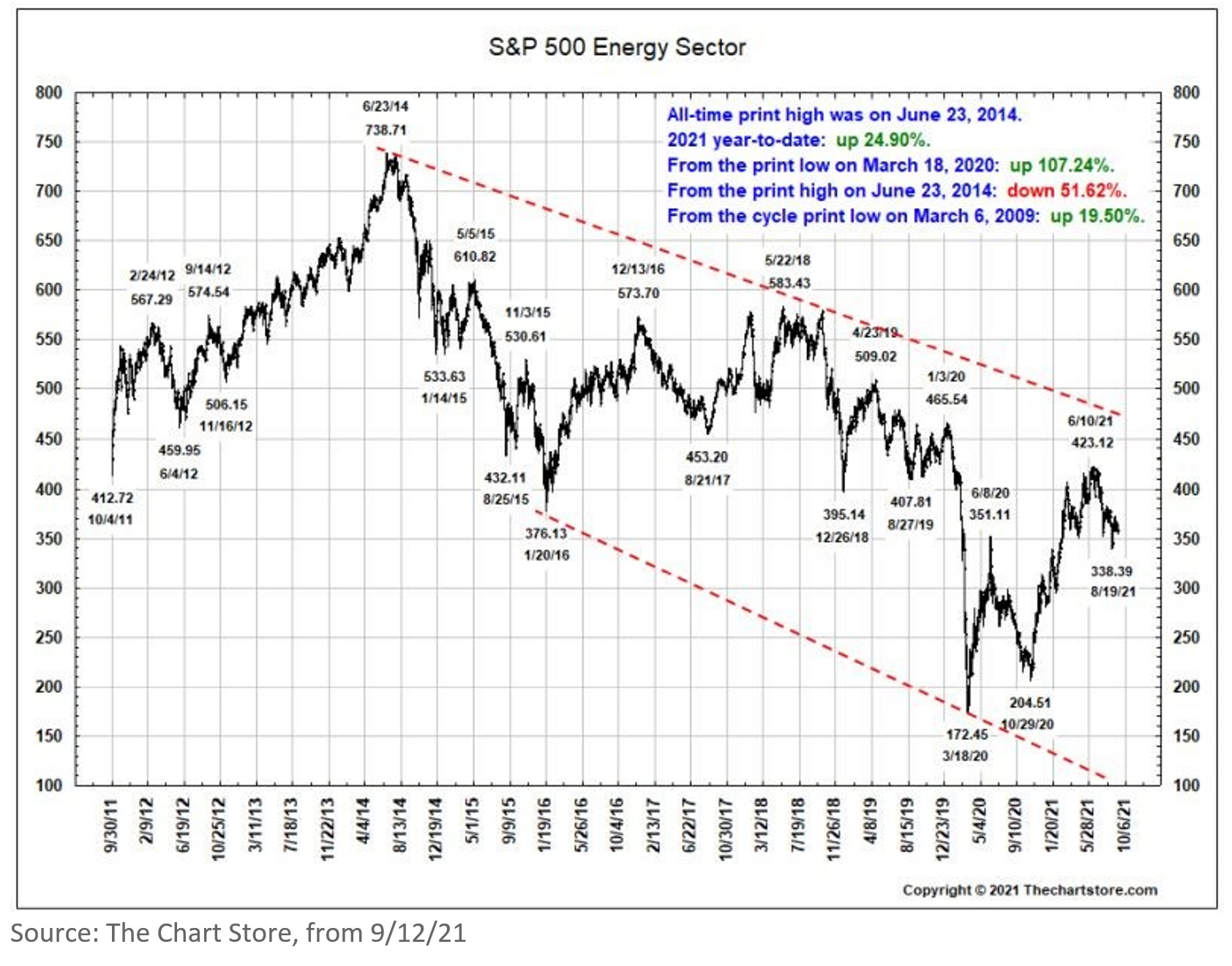

- Despite strong gains since last March, the Energy sector is still 50% off of its peak.

- A good portion of the S&P 500’s high valuation, compared to its history, has been justified.

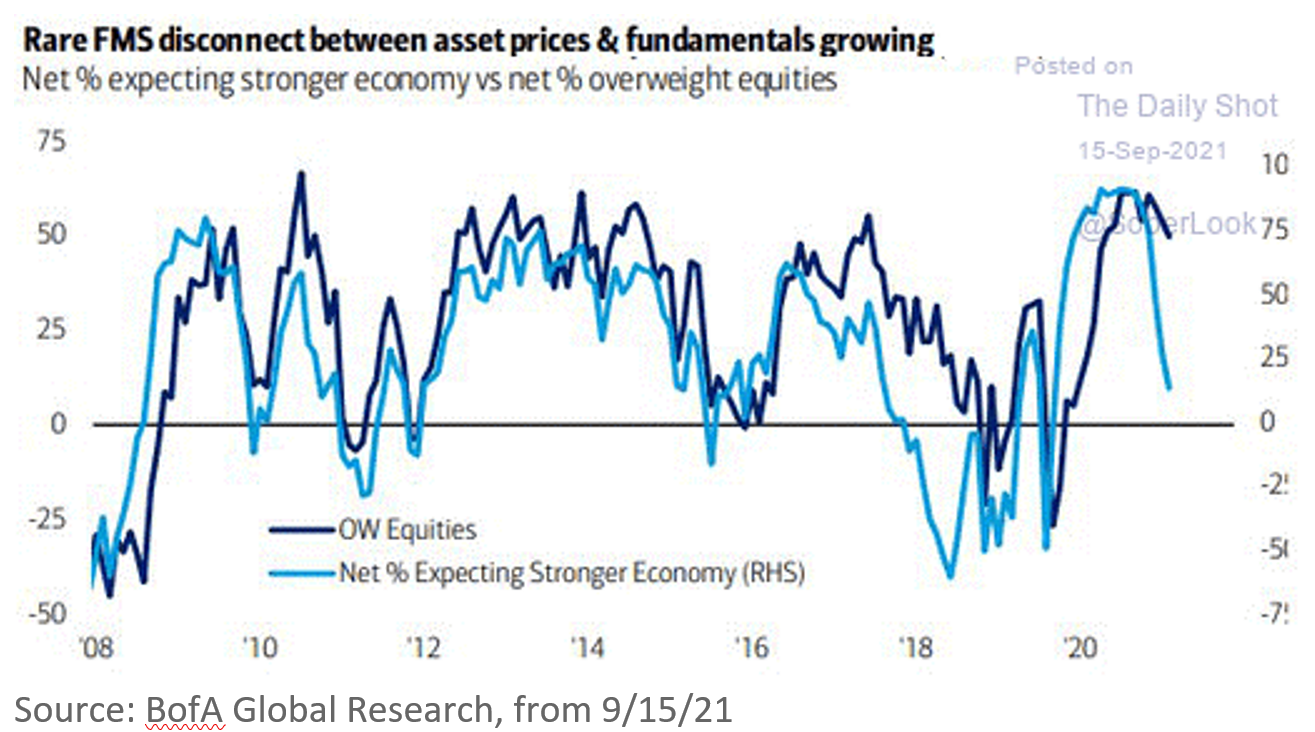

- Despite softening views on the economy, fund managers have no choice but to remain invested.

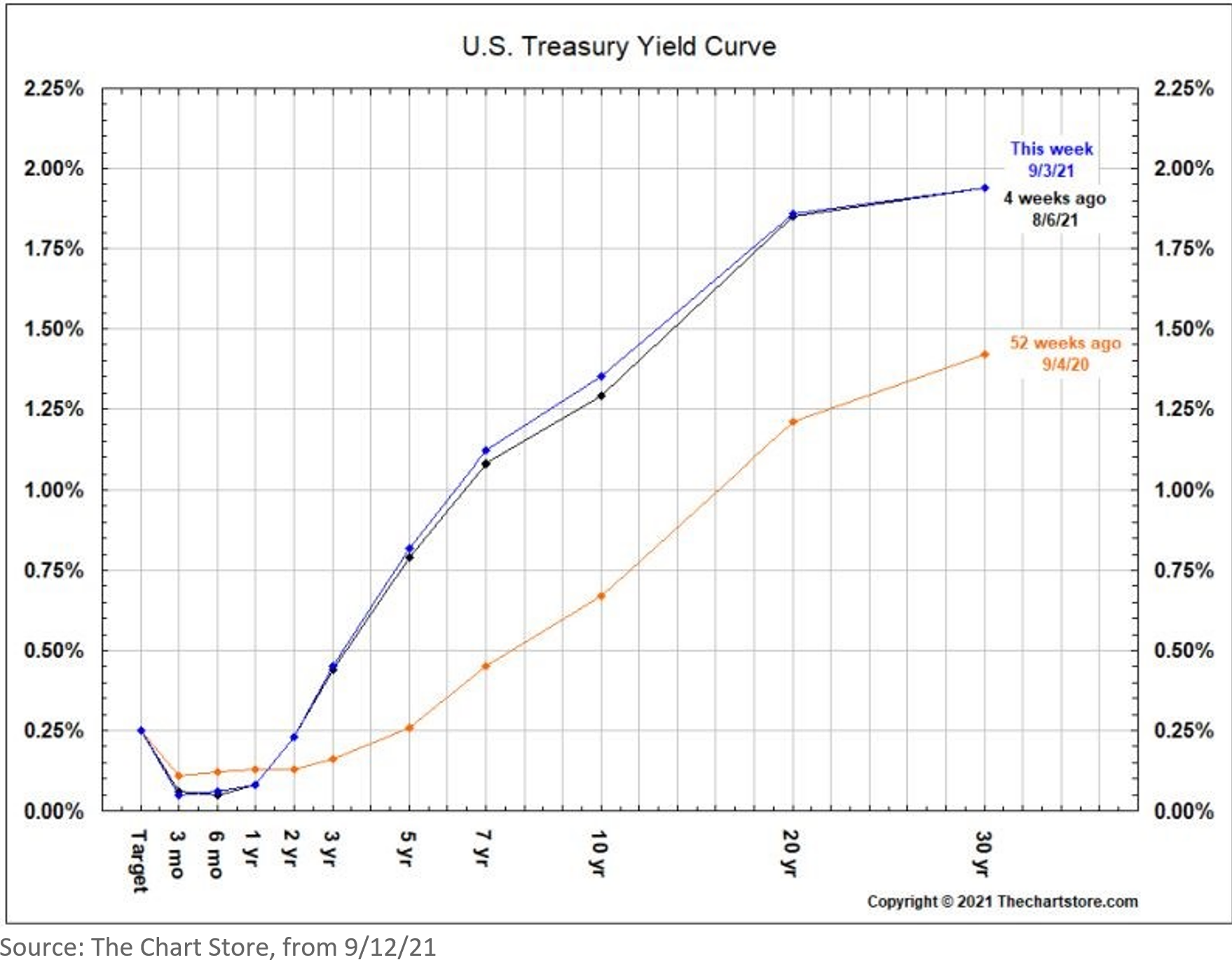

- Very little movement in interest rates over the past month.

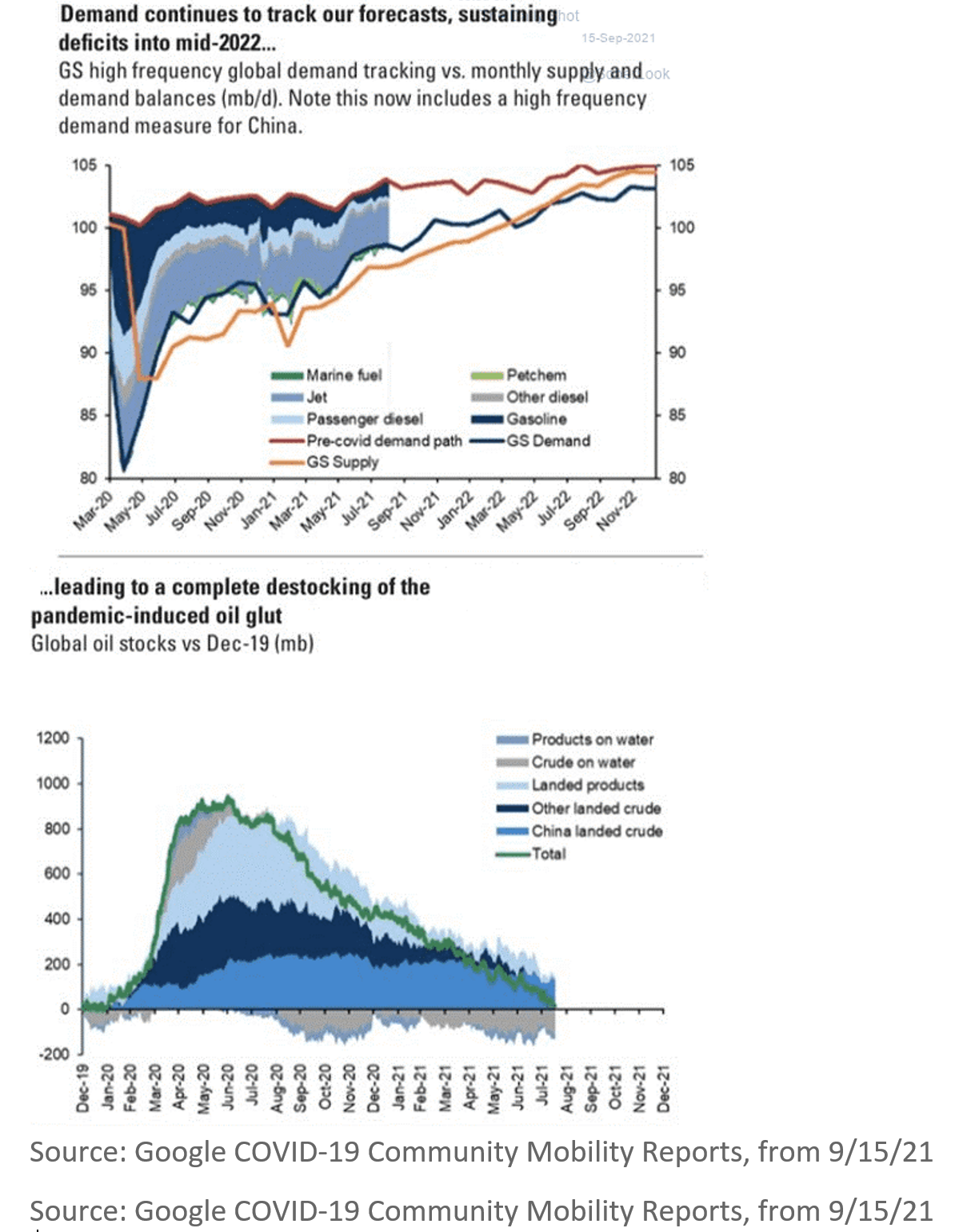

- The pandemic oil supply glut is nearly gone.

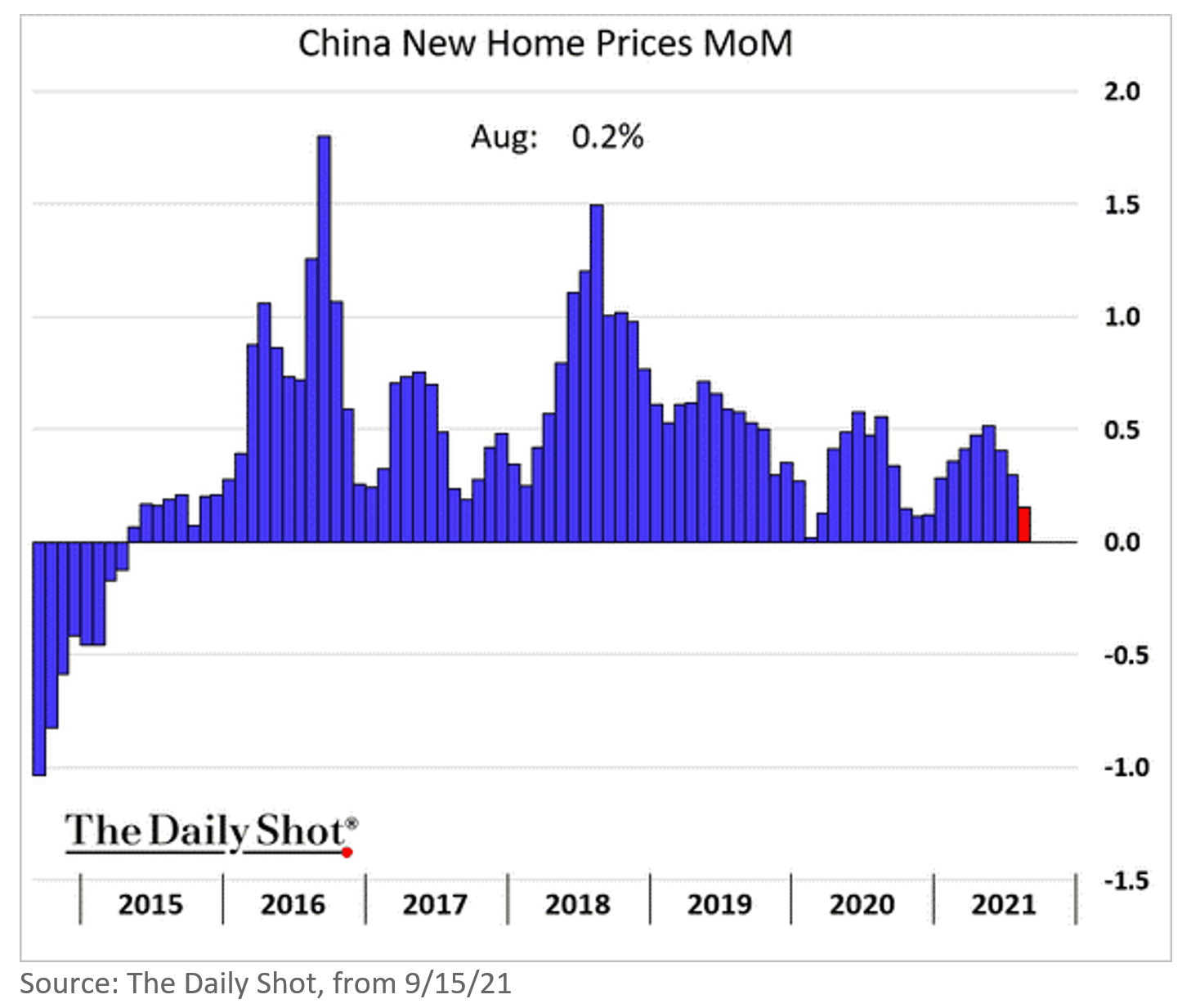

- The Chinese government has taken steps to moderate housing price increases. Unfortunately, this will surely lead to further distortions in China’s housing market.

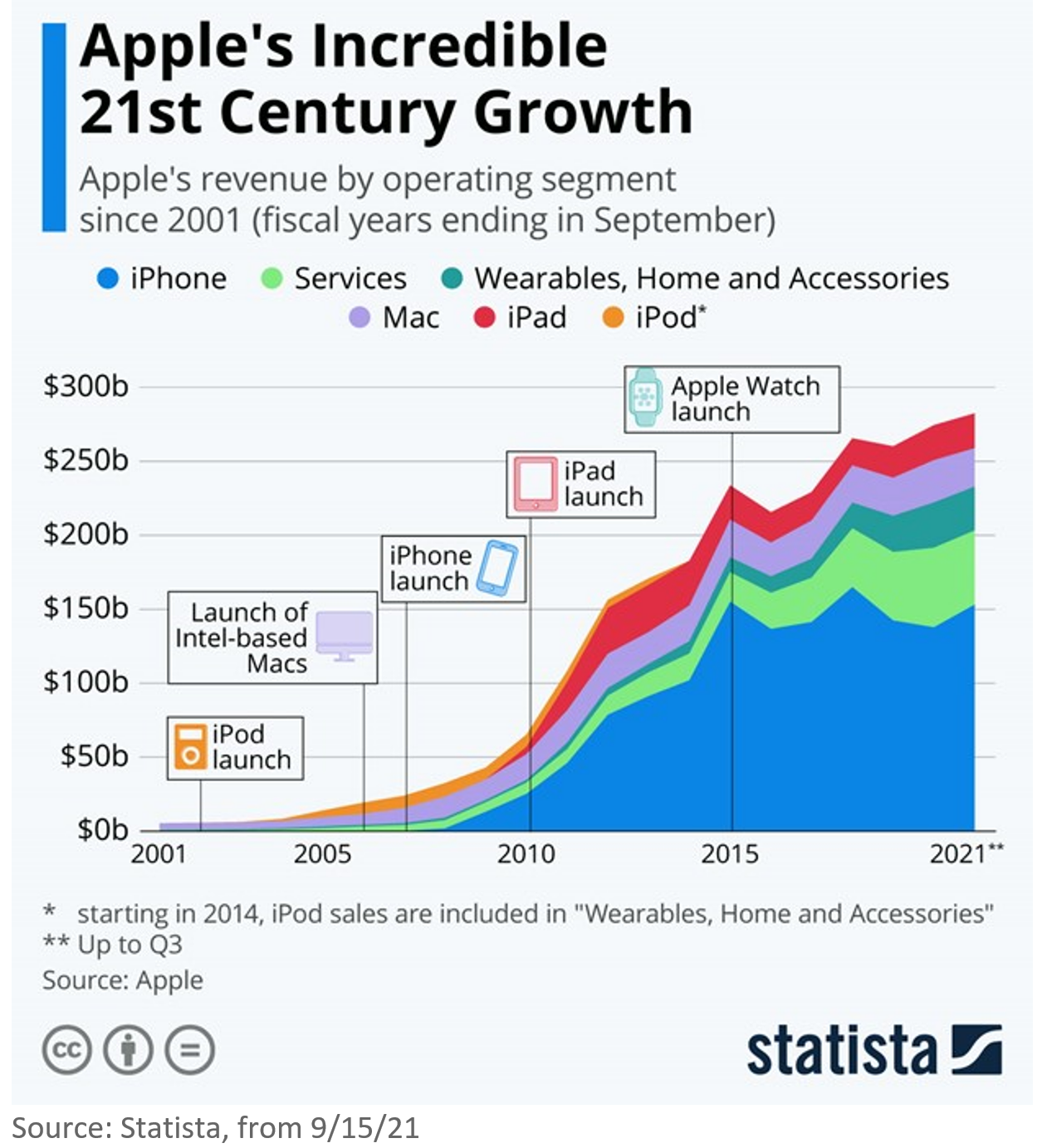

- Apple launched the iPhone 13 yesterday.

This article was contributed by Beaumont Capital Management, a participant in the ETF Strategist Channel.

For more insights like these, visit BCM’s blog at blog.investbcm.com.

Disclosure: The charts and info-graphics contained in this blog are typically based on data obtained from 3rd parties and are believed to be accurate. The commentary included is the opinion of the author and subject to change at any time. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be held in client accounts. Past performance is no guarantee of future results.