Friday’s disappointing jobs report has put a huge damper on economic sentiment for the moment. Goldman Sachs has bumped up the odds of a recession from 10% to 25% over the next 12 months. Global markets have been thrown for a loop. Some, like WisdomTree’s Jeremy Siegel, are even calling for “emergency” rate cuts of 75 basis points or more from the Federal Reserve. Overarching macro concerns over a weakening economy have led to a broad takedown of the markets across the board. Technology in particular has borne the brunt of the pain. But advisors have made much hype about the so-called “Great Rotation” over the past month, and for good reason. Of course, this aggressive reallocation may very well be temporarily interrupted by this week’s sell-off.

Small Cap with Strong Value Tilt

The consumer price index came at a much cooler-than-expected clip in early July. Since then, markets have undergone a decisive, almost violent shift away from the mega-cap growth trade toward small-cap value instead. The iShares Russell 2000 ETF (IWM) enjoyed its best week and month of the year following the tamer CPI print as of August 2. The small-cap benchmark rose 10% in July, while the Invesco QQQ Trust (QQQ) fell 2%. The Consumer Staples Select Sector SPDR Fund (XLP) also put on its third best daily showing versus the QQQs in 15 years.

For the month of July, 30 of the top-performing 50 ETFs were all small-cap ETFs. And 10 out of those 30 were explicitly focused on value. The iShares U.S. Small Cap Value Factor ETF (SVAL) topped the list, rising 15%, followed by the SPDR SSGA U.S. Small Cap Low Volatility Index (SMLV) and ProShares Russell 2000 Dividend Growers ETF (SMDV). Both are trading at a significant discount to the broader small-cap space.

| Top 20 Best-Performing ETFs | July 2024 |

| First Trust NASDAQ ABA Community Bank Index Fund (QABA) | 19.53% |

| iShares U.S. Home Construction ETF (ITB) | 19.33% |

| Invesco KBW Regional Banking ETF (KBWR) | 18.70% |

| SPDR S&P Regional Banking ETF (KRE) | 18.70% |

| SPDR S&P Homebuilders ETF (XHB) | 16.93% |

| SPDR S&P Bank ETF (KBE) | 16.30% |

| iShares U.S. Regional Banks ETF (IAT) | 16.18% |

| SPDR S&P Telecom ETF (XTL) | 15.71% |

| Invesco S&P SmallCap Financials ETF (PSCF) | 15.40% |

| iShares US Small Cap Value Factor ETF (SVAL) | 15.07% |

| Kurv Yield Premium Strategy Tesla (TSLA) ETF (TSLP) | 15.06% |

| SPDR SSGA US Small Cap Low Volatility Index ETF (SMLV) | 15.03% |

| ARK Genomic Revolution ETF (ARKG) | 14.78% |

| iShares MSCI Global Silver Miners ETF (SLVP) | 14.71% |

| VanEck Office and Commercial REIT ETF (DESK) | 14.64% |

| WisdomTree Efficient Gold Plus Gold Miners Strategy Fund (GDMN) | 14.57% |

| Virtus LifeSci Biotech Clinical Trials ETF (BBC) | 14.23% |

| ProShares Russell 2000 Dividend Growers ETF (SMDV) | 14.17% |

| Invesco S&P SmallCap Utilities & Communication Services ETF (PSCU) | 13.81% |

| WisdomTree U.S. SmallCap Fund (EES) | 13.58% |

Beyond just small caps, value-oriented sectors like real estate, financials and utilities have also done well. The iShares U.S. Home Construction ETF (ITB), SPDR S&P Regional Banking ETF (KRE) and even small-cap silver miners like the Amplify Junior Silver Miners ETF (SILJ) topped the list.

Triggering the Turnaround

Several macro catalysts sparked the move – including cooling inflation, signs of a relatively stable economy, and full faith in deeper rate cuts from the Federal Reserve (some to the tune of 50 basis points or more). Right now, the futures market is pricing in the equivalent of four cuts of 25 basis points or more through year-end. The Fed put is back in play, and the committee has plenty of dry powder on hand – 525 basis points, to be exact.

Rising concerns over tech valuations are also playing a pivotal role. Mixed earnings and muted performance from the Magnificent 7 showed the AI hype has transitioned into more of a “show-me” trade lately. Semis and crypto were among the worst performers in the past two weeks. On top of that, this week’s massive unwinding has pushed the Nasdaq deeper into correction territory – down more than 10% from recent highs.

The U.S. presidential election also factors into the equation. The initial notion of a Republican sweep was considered a boon to the domestic manufacturing and reshoring trade. A still uncertain geopolitical landscape also lends itself to bigger bets on small-cap companies, which tend to be more domestic-focused and less susceptible to geopolitical risk. Small caps also benefit more directly from lower borrowing costs and, in some cases, can serve as a hedge against global geopolitical risk and domestic election risk.

While growth strategies have taken a backseat, value-oriented ETFs, which are typically tied to companies with lower multiples, have outperformed. The iShares S&P 500 Value ETF (IVE) rose 5% versus the cap-weighted SPDR S&P 500 ETF Trust (SPY)’s 1% gain. Meanwhile, the iShares S&P 500 Growth ETF (IVW) fell 1.4%. The Vanguard Value Index Fund ETF (VTV) is the cheapest value ETF on the market, charging just 0.04% and rallying 15% in July. The fund brought in more than $600 million last month and $2.8 billion so far in 2024. That places it among the most popular value ETFs of the year, alongside the Avantis U.S. Small Cap Value ETF (AVUV).

Taking Care to Avoid Value Traps

Of course, cheaper does not always mean worthwhile. Smaller companies that are not profitable would benefit neither from a stronger macro backdrop nor rate cuts. To screen out potential trouble spots, some may want to turn to active management. The JPMorgan Active Small Cap Value ETF (JPSV), for instance, takes a bottom-up approach to actively screen for small-cap companies with less cylicality and niche market leadership. That fund rose 11% in July.

Will the Rotation Continue?

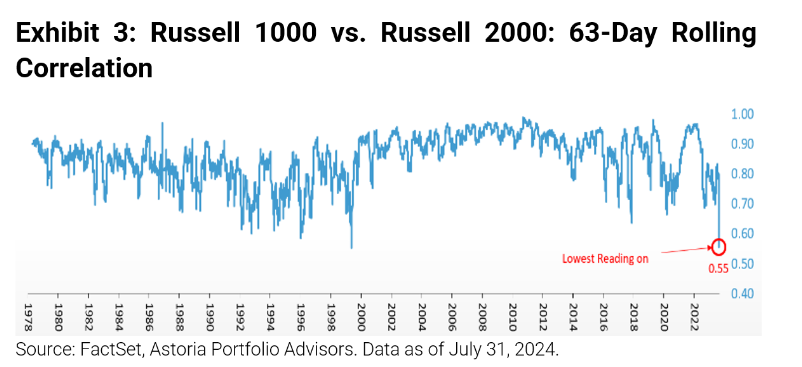

Finally, per data from Astoria Portfolio Advisors, the correlation of large caps (Russell 1000 Index) relative to small caps (Russell 2000 Index) recently reached its second-lowest level in history, on a 63-day rolling basis. That correlation may even be negative by now. Moreover, small caps remain historically cheap, offering at least a 27% discount to large caps.

Once the dust and drama settle in the market, and exempting a major jump in recession odds, the recent great rotation may prove to be the start of a longer-term trend. The driving forces mentioned above are still in place, at least for the moment. This is especially true for investors looking to stay fully invested but seeking to pinpoint exposure to undervalued pockets of opportunity.

For more news, information, and analysis, visit VettaFi | ETF Trends.